5.2 MARKET DYNAMICS

DRIVERS

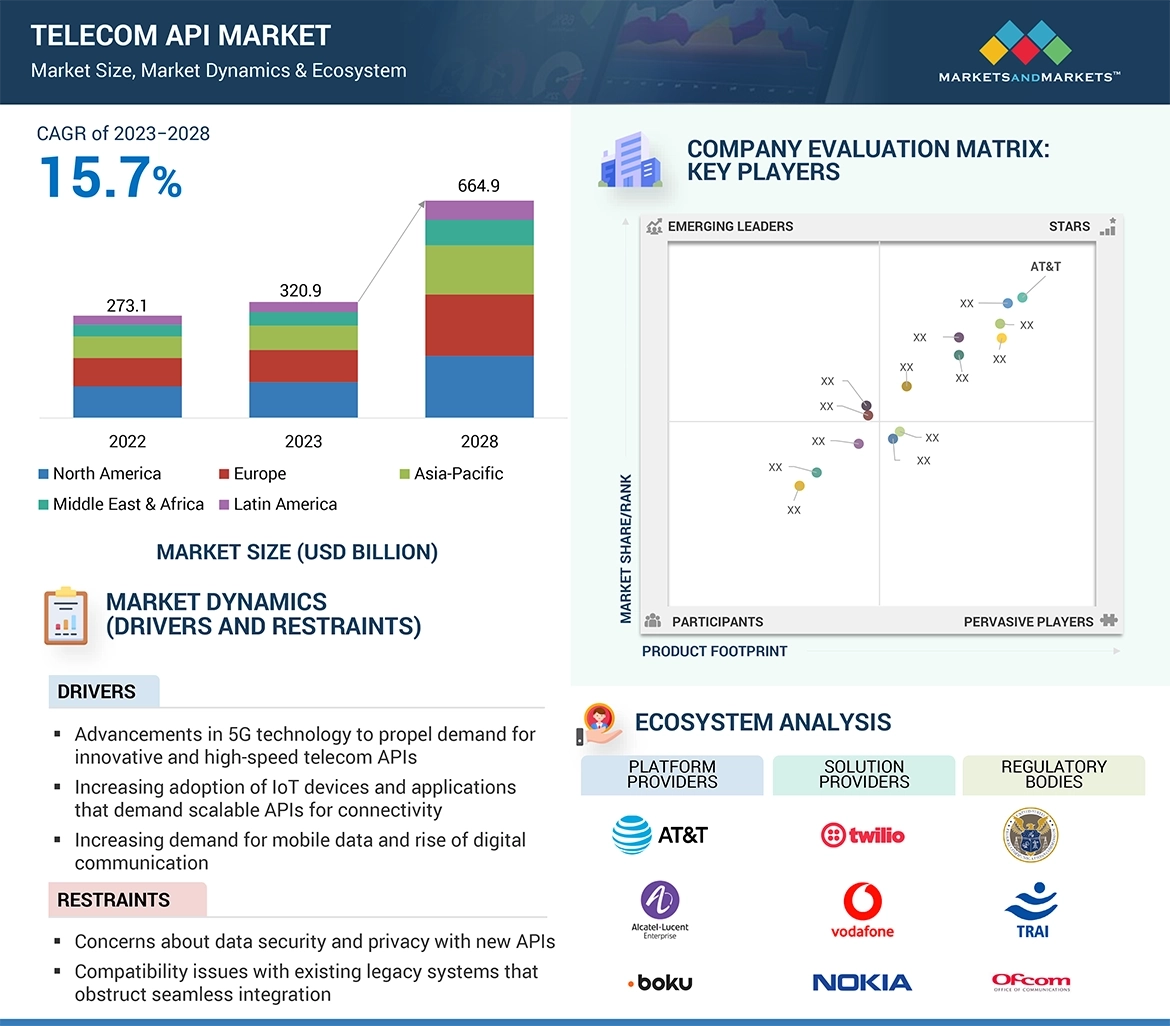

- Advancements in 5G technology to propel demand for innovative and high-speed telecom APIs

- Increasing adoption of IoT devices and applications that demand scalable APIs for connectivity

- Increasing demand for mobile data and rise of digital communication

- Increasing popularity of open APIs

RESTRAINTS

- Concerns about data security and privacy with new APIs

- Compatibility issues with existing legacy systems that obstruct seamless integration

OPPORTUNITIES

- Development of marketplaces for buying and selling APIs

- Valuable insights through API data analytics and creation of new revenue channels

CHALLENGES

- Technical complexity in management of various protocols and frameworks across different APIs

- Interoperability among diverse APIs and platforms hindered by absence of standardized protocols

5.3 INDUSTRY TRENDS

BRIEF HISTORY OF TELECOM API

- 1980s–1990s

- 1990s–2000s

- 2000–2010

- 2010–2020

- 2020–present

ECOSYSTEM: TELECOM API MARKET

CASE STUDY ANALYSIS

- Case Study 1: Twilio improves University of Warwick's student engagement and communication and security of student accounts

- Case Study 2: SmarterKey overcomes challenge of letting guests into rental properties with Twilio's two-way SMS capabilities

- Case Study 3: Wrizto Healthcare implements EnableX’s Live Video Calling API

- Case study 4: AT&T saves 2 million work hours annually with implementation of MuleSoft adopting API-led connectivity

- Case study 5: Apigee NeosAlpha helps Vodafone Network as a Platform to boost its API proxies performance

VALUE CHAIN ANALYSIS

REGULATORY LANDSCAPE

- Regulatory bodies, government agencies, and other organizations

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

PRICING ANALYSIS

- Average selling price trend of key players, by type of API

- Indicative pricing analysis, by type of API

TECHNOLOGY ANALYSIS

- Key technologies

- Complementary technologies

- Adjacent technologies

PATENT ANALYSIS

- Methodology

- List of major patents

KEY STAKEHOLDERS & BUYING CRITERIA

- Key stakeholders in buying criteria

- Buying criteria

KEY CONFERENCES & EVENTS, 2023–2024

PORTER’S FIVE FORCES ANALYSIS

- Threat of new entrants

- Threat of substitutes

- Bargaining power of buyers

- Bargaining power of suppliers

- Intensity of competitive rivalry

TRENDS AND DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

BEST PRACTICES IN TELECOM API MARKET

- Authentication and Authorization

- Use of Standard Protocols and Data Formats

- Placement of API beyond Gateway

- Optimized Requests and Responses

- Comprehensive Documentation

- Unit and Integration Testing

CURRENT AND EMERGING BUSINESS MODELS

- Direct Monetization Model

- Indirect Monetization Model

- API-as-a-service (AaaS)Model

- API Marketplaces Model

TELECOM API TOOLS, FRAMEWORKS, AND TECHNIQUES

FUTURE LANDSCAPE OF TELECOM API MARKET

- Telecom API Technology Roadmap till 2030

Growth opportunities and latent adjacency in Telecom API Market