TABLE OF CONTENTS

1 INTRODUCTION

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS (Page No. - 39)

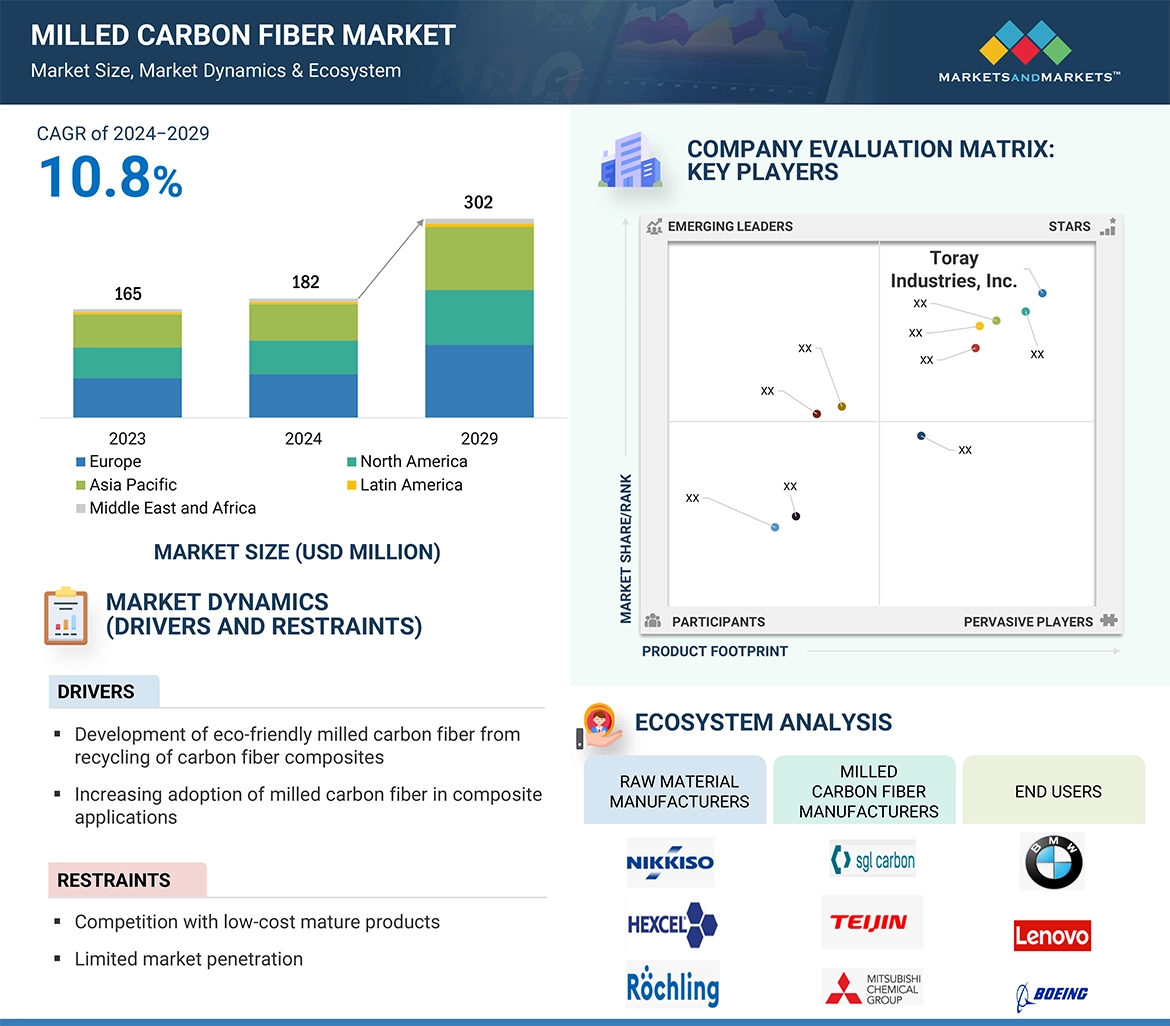

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MILLED CARBON FIBER MARKET

4.2 MILLED CARBON FIBER MARKET, BY APPLICATION AND REGION, 2023

4.3 MILLED CARBON FIBER MARKET, BY FIBER TYPE

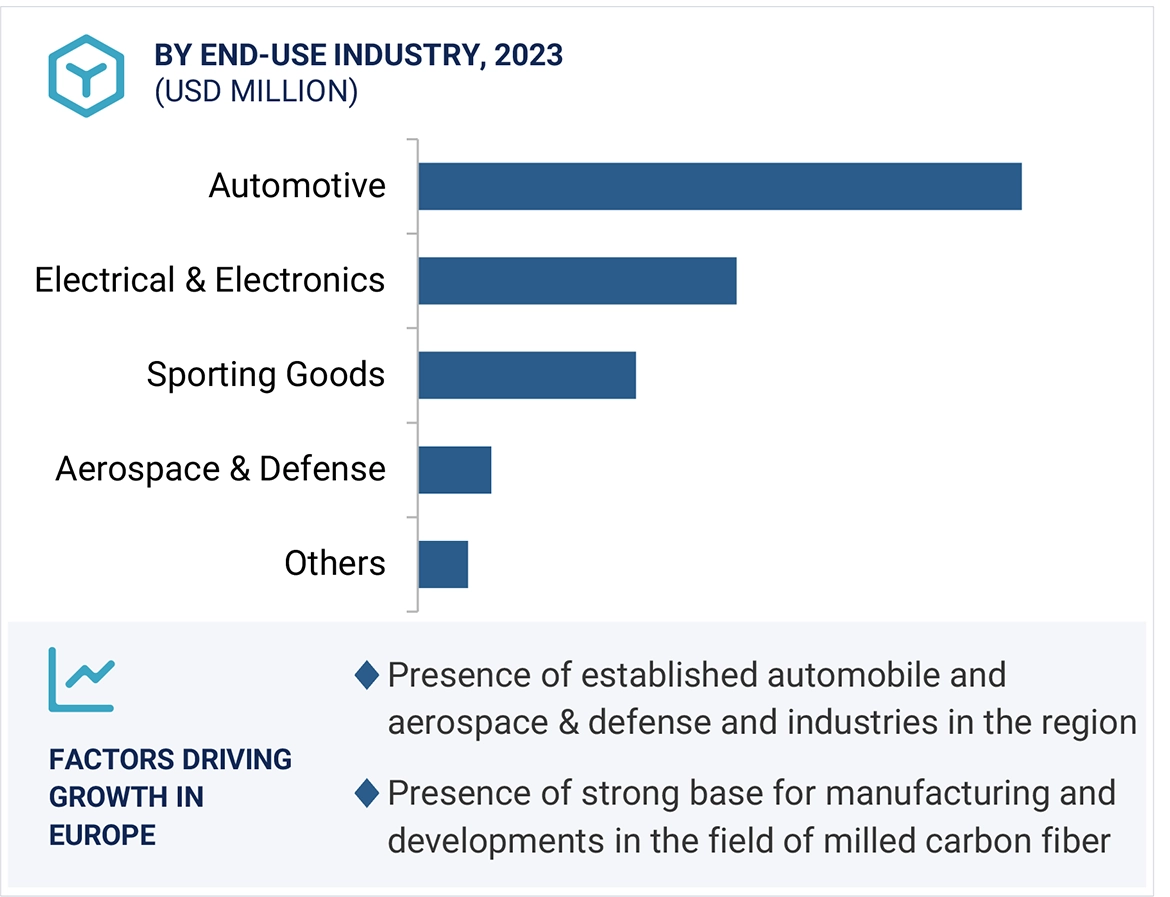

4.4 MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY

4.5 MILLED CARBON FIBER MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW (Page No. - 42)

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Development of eco-friendly milled carbon fiber from recycling of carbon fiber composites

5.2.1.2 Increasing adoption of milled carbon fiber in composite applications

5.2.1.3 Growing adoption of recyclable and lightweight milled carbon fibers in automotive industry

5.2.2 RESTRAINTS

5.2.2.1 Competition with low-cost mature products

5.2.3 OPPORTUNITIES

5.2.3.1 Reduction in cost of carbon fibers

5.2.3.2 Rising demand from emerging markets

5.2.4 CHALLENGES

5.2.4.1 Lack of availability of composite waste and limited recycling facilities

5.2.4.2 High production cost of milled carbon fibers

5.3 PORTER’S FIVE FORCES ANALYSIS

5.3.1 THREAT OF NEW ENTRANTS

5.3.2 THREAT OF SUBSTITUTES

5.3.3 BARGAINING POWER OF SUPPLIERS

5.3.4 BARGAINING POWER OF BUYERS

5.3.5 INTENSITY OF COMPETITIVE RIVALRY

5.4 SUPPLY CHAIN ANALYSIS

5.4.1 RAW MATERIAL

5.4.2 MANUFACTURING PROCESS

5.4.3 FINAL PRODUCT

5.5 ECOSYSTEM/MARKET MAP

5.6 PRICING ANALYSIS

5.6.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY END-USE INDUSTRY

5.6.2 AVERAGE SELLING PRICE TREND, BY FIBER TYPE

5.6.3 AVERAGE SELLING PRICE TREND, BY APPLICATION

5.6.4 AVERAGE SELLING PRICE TREND, BY REGION

5.7 VALUE CHAIN ANALYSIS

5.8 TRADE ANALYSIS

5.8.1 IMPORT SCENARIO FOR HS CODE 681511

5.8.2 EXPORT SCENARIO FOR HS CODE 681511

5.9 TECHNOLOGY ANALYSIS

5.9.1 KEY TECHNOLOGY

5.9.1.1 Mechanical process

5.9.2 COMPLEMENTARY TECHNOLOGY

5.9.2.1 Thermal recycling process

5.10 KEY STAKEHOLDERS AND BUYING CRITERIA

5.10.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.10.2 BUYING CRITERIA

5.11 PATENT ANALYSIS

5.11.1 INTRODUCTION

5.11.2 METHODOLOGY

5.11.3 DOCUMENT TYPES

5.11.4 INSIGHTS

5.11.5 LEGAL STATUS

5.11.6 JURISDICTION ANALYSIS

5.11.7 TOP APPLICANTS

5.11.8 TOP 10 PATENT OWNERS (US) IN LAST 13 YEARS

5.12 REGULATORY LANDSCAPE

5.12.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.13 KEY CONFERENCES AND EVENTS IN 2024–2025

5.14 CASE STUDY ANALYSIS

5.14.1 CASE STUDY: IMPACT OF MILLED CARBON FIBER ON LENOVO THINKPAD X1 SERIES LAPTOPS

5.15 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6 MILLED CARBON FIBER MARKET, BY FIBER TYPE (Page No. - 68)

6.1 INTRODUCTION

6.2 VIRGIN FIBER

6.2.1 GROWING DEMAND FOR LIGHTWEIGHT AND HIGH-STRENGTH MATERIALS

6.2.2 VIRGIN FIBER: MILLED CARBON FIBER MARKET, BY REGION

6.3 RECYCLED FIBER

6.3.1 SUSTAINABILITY AND COST-EFFECTIVENESS TO DRIVE MARKET

6.3.2 RECYCLED FIBER: MILLED CARBON FIBER MARKET, BY REGION

7 MILLED CARBON FIBER MARKET, BY APPLICATION (Page No. - 72)

7.1 INTRODUCTION

7.2 REINFORCEMENTS

7.3 COATINGS & ADHESIVES

7.4 OTHER APPLICATIONS

8 MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY (Page No. - 75)

8.1 INTRODUCTION

8.2 AUTOMOTIVE

8.2.1 GROWING DEMAND FOR LIGHTWEIGHT AND HIGH-STRENGTH MATERIALS TO DRIVE MARKET

8.2.2 AUTOMOTIVE: MILLED CARBON FIBER MARKET, BY REGION

8.3 ELECTRICAL & ELECTRONICS

8.3.1 IMPROVED ELECTRICAL CONDUCTIVITY OF ELECTRONIC PRODUCTS TO DRIVE MARKET

8.3.2 ELECTRICAL & ELECTRONICS: MILLED CARBON FIBER MARKET, BY REGION

8.4 SPORTING GOODS

8.4.1 HIGH TENSILE STRENGTH-TO-WEIGHT RATIO TO DRIVE MARKET

8.4.2 SPORTING GOODS: MILLED CARBON FIBER MARKET, BY REGION

8.5 AEROSPACE & DEFENSE

8.5.1 COST-SAVING ADVANTAGES TO DRIVE DEMAND

8.5.2 AEROSPACE & DEFENSE: MILLED CARBON FIBER MARKET, BY REGION

8.6 OTHER END-USE INDUSTRIES

8.6.1 OTHER END-USE INDUSTRIES: MILLED CARBON FIBER MARKET, BY REGION

9 MILLED CARBON FIBER MARKET, BY REGION (Page No. - 84)

9.1 INTRODUCTION

9.2 NORTH AMERICA

9.2.1 RECESSION IMPACT

9.2.1.1 US

9.2.1.1.1 Surging demand in automotive sector to drive market

9.2.1.2 Canada

9.2.1.2.1 Diverse industrial applications to drive market

9.3 EUROPE

9.3.1 RECESSION IMPACT

9.3.1.1 Germany

9.3.1.1.1 Innovation and industrial strength to drive market

9.3.1.2 France

9.3.1.2.1 Presence of strong manufacturing base to boost market

9.3.1.3 UK

9.3.1.3.1 Growing demand for sustainable, lightweight, and high-performance materials to drive market

9.3.1.4 Spain

9.3.1.4.1 Increasing demand for lightweight and durable materials in automotive industry to drive market

9.3.1.5 Italy

9.3.1.5.1 Advanced manufacturing and innovation to drive market

9.3.1.6 Rest of Europe

9.4 ASIA PACIFIC

9.4.1 RECESSION IMPACT

9.4.1.1 China

9.4.1.1.1 Established value chain and focus of OEMs on manufacturing cost-efficient and lightweight products to drive market

9.4.1.2 Japan

9.4.1.2.1 High demand from OEMs to drive market

9.4.1.3 Taiwan

9.4.1.3.1 Development of economic zones and government support to drive market

9.4.1.4 South Korea

9.4.1.4.1 Surging demand from automotive and electrical & electronics industries to drive market

9.4.1.5 Rest of Asia Pacific

9.5 LATIN AMERICA

9.5.1 RECESSION IMPACT

9.5.1.1 Brazil

9.5.1.1.1 Growth of automotive industry to drive market

9.5.1.2 Mexico

9.5.1.2.1 Lower manufacturing costs, proximity to OEMs in US, and duty-free access to key automotive markets to drive market

9.5.1.3 Rest of Latin America

9.6 MIDDLE EAST & AFRICA

9.6.1 RECESSION IMPACT

9.6.1.1 GCC countries

9.6.1.1.1 UAE

9.6.1.1.2 Saudi Arabia

9.6.1.1.3 Rest of GCC countries

9.6.1.2 South Africa

9.6.1.2.1 Local and international investments to boost market

9.6.1.3 Rest of Middle East & Africa

10 COMPETITIVE LANDSCAPE (Page No. - 123)

10.1 OVERVIEW

10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

10.3 REVENUE ANALYSIS

10.4 MARKET SHARE ANALYSIS

10.4.1 MARKET RANKING ANALYSIS

10.5 BRAND/PRODUCT COMPARATIVE ANALYSIS

10.5.1 BRAND/PRODUCT COMPARATIVE ANALYSIS, BY MILLED CARBON FIBER PRODUCTS

10.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

10.6.1 STARS

10.6.2 EMERGING LEADERS

10.6.3 PERVASIVE PLAYERS

10.6.4 PARTICIPANTS

10.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023

10.6.5.1 Company footprint

10.6.5.2 Fiber type footprint

10.6.5.3 Application footprint

10.6.5.4 End-use industry footprint

10.6.5.5 Region footprint

10.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

10.7.1 PROGRESSIVE COMPANIES

10.7.2 RESPONSIVE COMPANIES

10.7.3 DYNAMIC COMPANIES

10.7.4 STARTING BLOCKS

10.7.5 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

10.8 VALUATION AND FINANCIAL METRICS OF MILLED CARBON FIBER VENDORS

10.9 COMPETITIVE SCENARIO AND TRENDS

10.9.1 PRODUCT LAUNCHES

10.9.2 DEALS

10.9.3 EXPANSIONS

11 COMPANY PROFILES (Page No. - 143)

11.1 KEY COMPANIES

11.1.1 TORAY INDUSTRIES, INC.

11.1.1.1 Business overview

11.1.1.2 Products/Solutions/Services offered

11.1.1.3 Recent developments

11.1.1.3.1 Product launches

11.1.1.3.2 Deals

11.1.1.3.3 Expansions

11.1.1.4 MnM view

11.1.1.4.1 Right to win

11.1.1.4.2 Strategic choices

11.1.1.4.3 Weaknesses and competitive threats

11.1.2 TEIJIN LIMITED

11.1.2.1 Business overview

11.1.2.2 Products/Solutions/Services offered

11.1.2.3 Recent developments

11.1.2.3.1 Deals

11.1.2.4 MnM view

11.1.2.4.1 Right to win

11.1.2.4.2 Strategic choices

11.1.2.4.3 Weaknesses and competitive threats

11.1.3 SGL CARBON

11.1.3.1 Business overview

11.1.3.2 Products/Solutions/Services offered

11.1.3.3 Recent developments

11.1.3.3.1 Expansions

11.1.3.4 MnM view

11.1.3.4.1 Right to win

11.1.3.4.2 Strategic choices

11.1.3.4.3 Weaknesses and competitive threats

11.1.4 MITSUBISHI CHEMICAL GROUP CORPORATION

11.1.4.1 Business overview

11.1.4.2 Products/Solutions/Services offered

11.1.4.3 Recent developments

11.1.4.3.1 Deals

11.1.4.4 MnM view

11.1.4.4.1 Right to win

11.1.4.4.2 Strategic choices

11.1.4.4.3 Weaknesses and competitive threats

11.1.5 DAIGAS GROUP

11.1.5.1 Business overview

11.1.5.2 Products/Solutions/Services offered

11.1.5.3 MnM view

11.1.5.3.1 Right to win

11.1.5.3.2 Strategic choices

11.1.5.3.3 Weaknesses and competitive threats

11.1.6 STANFORD ADVANCED MATERIALS

11.1.6.1 Business overview

11.1.6.2 Products/Solutions/Services offered

11.1.6.3 MnM view

11.1.6.3.1 Right to win

11.1.6.3.2 Strategic choices

11.1.6.3.3 Weaknesses and competitive threats

11.1.7 NIPPON GRAPHITE FIBER CO., LTD.

11.1.7.1 Business overview

11.1.7.2 Products/Solutions/Services offered

11.1.7.3 MnM view

11.1.7.3.1 Right to win

11.1.7.3.2 Strategic choices

11.1.7.3.3 Weaknesses and competitive threats

11.1.8 EASY COMPOSITES LTD

11.1.8.1 Business overview

11.1.8.2 Products/Solutions/Services offered

11.1.8.3 Recent developments

11.1.8.3.1 Expansions

11.1.8.4 MnM view

11.1.8.4.1 Right to win

11.1.8.4.2 Strategic choices

11.1.8.4.3 Weaknesses and competitive threats

11.1.9 HAUFLER COMPOSITES GMBH & CO. KG

11.1.9.1 Business overview

11.1.9.2 Products/Solutions/Services offered

11.1.9.3 MnM view

11.1.9.3.1 Right to win

11.1.9.3.2 Strategic choices

11.1.9.3.3 Weaknesses and competitive threats

11.1.10 PROCOTEX

11.1.10.1 Business overview

11.1.10.2 Products/Solutions/Services offered

11.1.10.3 Recent developments

11.1.10.3.1 Deals

11.1.10.3.2 Expansions

11.1.10.4 MnM view

11.1.10.4.1 Right to win

11.1.10.4.2 Strategic choices

11.1.10.4.3 Weaknesses and competitive threats

11.2 OTHER PLAYERS

11.2.1 CLM-PRO

11.2.2 R&G FASERVERBUNDWERKSTOFFE GMBH

11.2.3 NIPPON POLYMER SANGYO CO., LTD.

11.2.4 TASUNS COMPOSITE TECHNOLOGY CO., LTD.

11.2.5 NANTONG YONGTONG ENVIRONMENTAL TECHNOLOGY CO., LTD.

11.2.6 HEBEI YAYANG SPODUMENE CO., LTD.

11.2.7 K. SAKAI & CO., LTD.

11.2.8 ELLEY NEW MATERIAL CO., LTD.

11.2.9 TIANJIN YUFENG CARBON CO., LTD.

11.2.10 CARBONFIBER.CZ

11.2.11 SHENZHEN XIANGU HIGH-TECH. CO., LTD.

11.2.12 HANGZHOU IMPACT NEW MATERIALS CO., LTD.

11.2.13 CHINA BEIHAI FIBERGLASS CO., LTD.

11.2.14 SHANGHAI SHENGHE TEXTILE TECHNOLOGY CO., LTD.

11.2.15 ARITECH CHEMAZONE PVT LTD.

12 APPENDIX (Page No. - 180)

12.1 DISCUSSION GUIDE

12.2 KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

12.3 CUSTOMIZATION OPTIONS

12.4 RELATED REPORTS

12.5 AUTHOR DETAILS

LIST OF TABLES (162 TABLES)

TABLE 1 MILLED CARBON FIBER MARKET: ROLE OF COMPANIES IN ECOSYSTEM

TABLE 2 AVERAGE SELLING PRICE TREND, BY REGION

TABLE 3 LEADING IMPORTING COUNTRIES FOR HS CODE 681511

TABLE 4 LEADING EXPORTING COUNTRIES FOR HS CODE 681511

TABLE 5 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END-USE INDUSTRIES IN MILLED CARBON FIBER MARKET

TABLE 6 KEY BUYING CRITERIA FOR TOP THREE END-USE INDUSTRIES IN MILLED CARBON FIBER MARKET

TABLE 7 MILLED CARBON FIBER MARKET: TOTAL NUMBER OF PATENTS

TABLE 8 LIST OF PATENTS BY DALIAN UNIVERSITY OF TECHNOLOGY

TABLE 9 LIST OF PATENTS BY CENTRAL SOUTH UNIVERSITY

TABLE 10 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 11 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 12 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 13 MILLED CARBON FIBER MARKET: KEY CONFERENCES AND EVENTS, 2024–2025

TABLE 14 MILLED CARBON FIBER MARKET, BY FIBER TYPE, 2022–2029 (USD MILLION)

TABLE 15 MILLED CARBON FIBER MARKET, BY FIBER TYPE, 2022–2029 (TON)

TABLE 16 MILLED VIRGIN CARBON FIBER MARKET, BY REGION, 2022–2029 (USD MILLION)

TABLE 17 MILLED VIRGIN CARBON FIBER MARKET, BY REGION, 2022–2029 (TON)

TABLE 18 MILLED RECYCLED CARBON FIBER MARKET, BY REGION, 2022–2029 (USD MILLION)

TABLE 19 MILLED RECYCLED CARBON FIBER MARKET, BY REGION, 2022–2029 (TON)

TABLE 20 MILLED CARBON FIBER MARKET, BY APPLICATION, 2022–2029 (USD MILLION)

TABLE 21 MILLED CARBON FIBER MARKET, BY APPLICATION, 2022–2029 (TON)

TABLE 22 MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 23 MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 24 MILLED CARBON FIBER MARKET IN AUTOMOTIVE INDUSTRY, BY REGION, 2022–2029 (USD MILLION)

TABLE 25 MILLED CARBON FIBER MARKET IN AUTOMOTIVE INDUSTRY, BY REGION, 2022–2029 (TON)

TABLE 26 MILLED CARBON FIBER MARKET IN ELECTRICAL & ELECTRONICS INDUSTRY, BY REGION, 2022–2029 (USD MILLION)

TABLE 27 MILLED CARBON FIBER MARKET IN ELECTRICAL & ELECTRONICS INDUSTRY, BY REGION, 2022–2029 (TON)

TABLE 28 MILLED CARBON FIBER MARKET IN SPORTING GOODS INDUSTRY, BY REGION, 2022–2029 (USD MILLION)

TABLE 29 MILLED CARBON FIBER MARKET IN SPORTING GOODS INDUSTRY, BY REGION, 2022–2029 (TON)

TABLE 30 MILLED CARBON FIBER MARKET IN AEROSPACE & DEFENSE INDUSTRY, BY REGION, 2022–2029 (USD MILLION)

TABLE 31 MILLED CARBON FIBER MARKET IN AEROSPACE & DEFENSE INDUSTRY, BY REGION, 2022–2029 (TON)

TABLE 32 MILLED CARBON FIBER MARKET IN OTHER END-USE INDUSTRIES, BY REGION, 2022–2029 (USD MILLION)

TABLE 33 MILLED CARBON FIBER MARKET IN OTHER END-USE INDUSTRIES, BY REGION, 2022–2029 (TON)

TABLE 34 MILLED CARBON FIBER MARKET, BY REGION, 2022–2029 (USD MILLION)

TABLE 35 MILLED CARBON FIBER MARKET, BY REGION, 2022–2029 (TON)

TABLE 36 NORTH AMERICA: MILLED CARBON FIBER MARKET, BY FIBER TYPE, 2022–2029 (USD MILLION)

TABLE 37 NORTH AMERICA: MILLED CARBON FIBER MARKET, BY FIBER TYPE, 2022–2029 (TON)

TABLE 38 NORTH AMERICA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 39 NORTH AMERICA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 40 NORTH AMERICA: MILLED CARBON FIBER MARKET, BY COUNTRY, 2022–2029 (USD MILLION)

TABLE 41 NORTH AMERICA: MILLED CARBON FIBER MARKET, BY COUNTRY, 2022–2029 (TON)

TABLE 42 US: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 43 US: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 44 CANADA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 45 CANADA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 46 EUROPE: MILLED CARBON FIBER MARKET, BY FIBER TYPE, 2022–2029 (USD MILLION)

TABLE 47 EUROPE: MILLED CARBON FIBER MARKET, BY FIBER TYPE, 2022–2029 (TON)

TABLE 48 EUROPE: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 49 EUROPE: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 50 EUROPE: MILLED CARBON FIBER MARKET, BY COUNTRY, 2022–2029 (USD MILLION)

TABLE 51 EUROPE: MILLED CARBON FIBER MARKET, BY COUNTRY, 2022–2029 (TON)

TABLE 52 GERMANY: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 53 GERMANY: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 54 FRANCE: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 55 FRANCE: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 56 UK: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 57 UK: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 58 SPAIN: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 59 SPAIN: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 60 ITALY: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 61 ITALY: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 62 REST OF EUROPE: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 63 REST OF EUROPE: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 64 ASIA PACIFIC: MILLED CARBON FIBER MARKET, BY FIBER TYPE, 2022–2029 (USD MILLION)

TABLE 65 ASIA PACIFIC: MILLED CARBON FIBER MARKET, BY FIBER TYPE, 2022–2029 (TON)

TABLE 66 ASIA PACIFIC: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 67 ASIA PACIFIC: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 68 ASIA PACIFIC: MILLED CARBON FIBER MARKET, BY COUNTRY, 2022–2029 (USD MILLION)

TABLE 69 ASIA PACIFIC: MILLED CARBON FIBER MARKET, BY COUNTRY, 2022–2029 (TON)

TABLE 70 CHINA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 71 CHINA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 72 JAPAN: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 73 JAPAN: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 74 TAIWAN: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 75 TAIWAN: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 76 SOUTH KOREA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 77 SOUTH KOREA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 78 REST OF ASIA PACIFIC: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 79 REST OF ASIA PACIFIC: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 80 LATIN AMERICA: MILLED CARBON FIBER MARKET, BY FIBER TYPE, 2022–2029 (USD MILLION)

TABLE 81 LATIN AMERICA: MILLED CARBON FIBER MARKET, BY FIBER TYPE, 2022–2029 (TON)

TABLE 82 LATIN AMERICA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 83 LATIN AMERICA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 84 LATIN AMERICA: MILLED CARBON FIBER MARKET, BY COUNTRY, 2022–2029 (USD MILLION)

TABLE 85 LATIN AMERICA: MILLED CARBON FIBER MARKET, BY COUNTRY, 2022–2029 (TON)

TABLE 86 BRAZIL: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 87 BRAZIL: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 88 MEXICO: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 89 MEXICO: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TONS)

TABLE 90 REST OF LATIN AMERICA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 91 REST OF LATIN AMERICA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 92 MIDDLE EAST & AFRICA: MILLED CARBON FIBER MARKET, BY FIBER TYPE, 2022–2029 (USD MILLION)

TABLE 93 MIDDLE EAST & AFRICA: MILLED CARBON FIBER MARKET, BY FIBER TYPE, 2022–2029 (TON)

TABLE 94 MIDDLE EAST & AFRICA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 95 MIDDLE EAST AND AFRICA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 96 MIDDLE EAST & AFRICA: MILLED CARBON FIBER MARKET, BY COUNTRY, 2022–2029 (USD MILLION)

TABLE 97 MIDDLE EAST & AFRICA: MILLED CARBON FIBER MARKET, BY COUNTRY, 2022–2029 (TON)

TABLE 98 UAE: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 99 UAE: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 100 SAUDI ARABIA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 101 SAUDI ARABIA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 102 REST OF GCC COUNTRIES: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 103 REST OF GCC COUNTRIES: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 104 SOUTH AFRICA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 105 SOUTH AFRICA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 106 REST OF MIDDLE EAST & AFRICA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (USD MILLION)

TABLE 107 REST OF MIDDLE EAST & AFRICA: MILLED CARBON FIBER MARKET, BY END-USE INDUSTRY, 2022–2029 (TON)

TABLE 108 STRATEGIES ADOPTED BY MILLED CARBON FIBER MANUFACTURERS

TABLE 109 DEGREE OF COMPETITION: MILLED CARBON FIBER MARKET

TABLE 110 MILLED CARBON FIBER MARKET: FIBER TYPE FOOTPRINT (10 COMPANIES)

TABLE 111 MILLED CARBON FIBER MARKET: APPLICATION FOOTPRINT (10 COMPANIES)

TABLE 112 MILLED CARBON FIBER MARKET: END-USE INDUSTRY FOOTPRINT (10 COMPANIES)

TABLE 113 MILLED CARBON FIBER MARKET: REGION FOOTPRINT (10 COMPANIES)

TABLE 114 MILLED CARBON FIBER MARKET: KEY STARTUPS/SMES

TABLE 115 MILLED CARBON FIBER MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

TABLE 116 MILLED CARBON FIBER MARKET: PRODUCT LAUNCHES, JANUARY 2018–APRIL 2024

TABLE 117 MILLED CARBON FIBER MARKET: DEALS, JANUARY 2018–APRIL 2024

TABLE 118 MILLED CARBON FIBER MARKET: EXPANSIONS, JANUARY 2018–APRIL 2024

TABLE 119 TORAY INDUSTRIES, INC.: COMPANY OVERVIEW

TABLE 120 TORAY INDUSTRIES, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 121 TORAY INDUSTRIES, INC.: PRODUCT LAUNCHES

TABLE 122 TORAY INDUSTRIES, INC.: DEALS

TABLE 123 TORAY INDUSTRIES, INC.: EXPANSIONS

TABLE 124 TEIJIN LIMITED: COMPANY OVERVIEW

TABLE 125 TEIJIN LIMITED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 126 TEIJIN LIMITED: DEALS

TABLE 127 SGL CARBON: COMPANY OVERVIEW

TABLE 128 SGL CARBON: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 129 SGL CARBON: EXPANSIONS

TABLE 130 MITSUBISHI CHEMICAL GROUP CORPORATION: COMPANY OVERVIEW

TABLE 131 MITSUBISHI CHEMICAL GROUP CORPORATION: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

TABLE 132 MITSUBISHI CHEMICAL GROUP CORPORATION: DEALS

TABLE 133 DAIGAS GROUP: COMPANY OVERVIEW

TABLE 134 DAIGAS GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 135 STANFORD ADVANCED MATERIALS: COMPANY OVERVIEW

TABLE 136 STANFORD ADVANCED MATERIALS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 137 NIPPON GRAPHITE FIBER CO., LTD.: COMPANY OVERVIEW

TABLE 138 NIPPON GRAPHITE FIBER CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 139 EASY COMPOSITES LTD: COMPANY OVERVIEW

TABLE 140 EASY COMPOSITES LTD: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 141 EASY COMPOSITES LTD: EXPANSIONS

TABLE 142 HAUFLER COMPOSITES GMBH & CO. KG: COMPANY OVERVIEW

TABLE 143 HAUFLER COMPOSITES GMBH & CO. KG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 144 PROCOTEX: COMPANY OVERVIEW

TABLE 145 PROCOTEX: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 146 PROCOTEX: DEALS

TABLE 147 PROCOTEX: EXPANSIONS

TABLE 148 CLM-PRO: COMPANY OVERVIEW

TABLE 149 R&G FASERVERBUNDWERKSTOFFE GMBH: COMPANY OVERVIEW

TABLE 150 NIPPON POLYMER SANGYO CO., LTD.: COMPANY OVERVIEW

TABLE 151 TASUNS COMPOSITE TECHNOLOGY CO., LTD.: COMPANY OVERVIEW

TABLE 152 NANTONG YONGTONG ENVIRONMENTAL TECHNOLOGY CO., LTD.: COMPANY OVERVIEW

TABLE 153 HEBEI YAYANG SPODUMENE CO., LTD.: COMPANY OVERVIEW

TABLE 154 K. SAKAI & CO., LTD.: COMPANY OVERVIEW

TABLE 155 ELLEY NEW MATERIAL CO., LTD.: COMPANY OVERVIEW

TABLE 156 TIANJIN YUFENG CARBON CO., LTD.: COMPANY OVERVIEW

TABLE 157 CARBONFIBER.CZ: COMPANY OVERVIEW

TABLE 158 SHENZHEN XIANGU HIGH-TECH. CO., LTD.: COMPANY OVERVIEW

TABLE 159 HANGZHOU IMPACT NEW MATERIALS CO., LTD.: COMPANY OVERVIEW

TABLE 160 CHINA BEIHAI FIBERGLASS CO., LTD.: COMPANY OVERVIEW

TABLE 161 SHANGHAI SHENGHE TEXTILE TECHNOLOGY CO., LTD.: COMPANY OVERVIEW

TABLE 162 ARITECH CHEMAZONE PVT LTD.: COMPANY OVERVIEW

LIST OF FIGURES (55 FIGURES)

FIGURE 1 MILLED CARBON FIBER: MARKET SEGMENTATION

FIGURE 2 MILLED CARBON FIBER MARKET: RESEARCH DESIGN

FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

FIGURE 5 MILLED CARBON FIBER MARKET: DATA TRIANGULATION

FIGURE 6 RECYCLED FIBER TO DOMINATE MILLED CARBON FIBER MARKET IN 2023

FIGURE 7 REINFORCEMENTS APPLICATION RECORDED LARGER MARKET SHARE IN 2023

FIGURE 8 AUTOMOTIVE ACCOUNTED FOR LARGEST MARKET SHARE IN 2023

FIGURE 9 EUROPE ACCOUNTED FOR LARGEST MARKET SHARE IN 2023

FIGURE 10 HIGH DEMAND FOR LIGHTWEIGHT MATERIALS TO DRIVE MARKET

FIGURE 11 REINFORCEMENTS APPLICATION AND EUROPE ACCOUNTED FOR LARGEST SHARES IN 2023

FIGURE 12 RECYCLED FIBER SEGMENT HELD LARGEST SHARE IN 2023

FIGURE 13 AUTOMOTIVE SEGMENT HELD LARGEST SHARE IN 2023

FIGURE 14 US TO DOMINATE MARKET DURING FORECAST PERIOD

FIGURE 15 MILLED CARBON FIBER MARKET: MARKET DYNAMICS

FIGURE 16 MILLED CARBON FIBER MARKET: PORTER’S FIVE FORCES ANALYSIS

FIGURE 17 MILLED CARBON FIBER MARKET: KEY STAKEHOLDERS IN ECOSYSTEM

FIGURE 18 MILLED CARBON FIBER MARKET: ECOSYSTEM

FIGURE 19 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY END-USE INDUSTRY

FIGURE 20 AVERAGE SELLING PRICE OF MILLED CARBON FIBER, BY FIBER TYPE (USD/KG)

FIGURE 21 AVERAGE SELLING PRICE OF MILLED CARBON FIBER, BY APPLICATION (USD/KG)

FIGURE 22 MILLED CARBON FIBER MARKET: VALUE CHAIN ANALYSIS

FIGURE 23 IMPORT FOR HS CODE 681511, BY KEY COUNTRY, 2022–2023 (USD THOUSAND)

FIGURE 24 EXPORT FOR HS CODE 681511, BY KEY COUNTRY, 2022–2023 (USD THOUSAND)

FIGURE 25 TECHNOLOGY ANALYSIS

FIGURE 26 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END-USE INDUSTRIES

FIGURE 27 KEY BUYING CRITERIA FOR TOP THREE END-USE INDUSTRIES

FIGURE 28 PATENT ANALYSIS, BY DOCUMENT TYPE

FIGURE 29 PATENT PUBLICATION TREND, 2014−2024

FIGURE 30 MILLED CARBON FIBER MARKET: LEGAL STATUS OF PATENTS

FIGURE 31 CHINESE JURISDICTION REGISTERED HIGHEST NUMBER OF PATENTS

FIGURE 32 DALIAN UNIVERSITY OF TECHNOLOGY REGISTERED HIGHEST NUMBER OF PATENTS

FIGURE 33 REVENUE SHIFT AND NEW REVENUE POCKETS IN MILLED CARBON FIBER MARKET

FIGURE 34 RECYCLED CARBON FIBER TO REGISTER HIGHER CAGR DURING FORECAST PERIOD

FIGURE 35 REINFORCEMENTS TO REGISTER HIGHER CAGR DURING FORECAST PERIOD

FIGURE 36 AUTOMOTIVE INDUSTRY TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 37 CHINA TO BE FASTEST-GROWING MILLED CARBON FIBER MARKET DURING FORECAST PERIOD

FIGURE 38 NORTH AMERICA: MILLED CARBON FIBER MARKET SNAPSHOT

FIGURE 39 EUROPE: MILLED CARBON FIBER MARKET SNAPSHOT

FIGURE 40 ASIA PACIFIC: MILLED CARBON FIBER MARKET SNAPSHOT

FIGURE 41 MILLED CARBON FIBER MARKET: REVENUE ANALYSIS OF TOP 5 MARKET PLAYERS

FIGURE 42 SHARES OF KEY PLAYERS IN MILLED CARBON FIBER MARKET

FIGURE 43 RANKING OF TOP FIVE PLAYERS IN MILLED CARBON FIBER MARKET

FIGURE 44 MILLED CARBON FIBER MARKET: TOP TRENDING BRANDS/PRODUCTS

FIGURE 45 BRAND/PRODUCT COMPARATIVE ANALYSIS, BY MILLED CARBON FIBER PRODUCTS

FIGURE 46 MILLED CARBON FIBER MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

FIGURE 47 MILLED CARBON FIBER MARKET: COMPANY FOOTPRINT (10 COMPANIES)

FIGURE 48 MILLED CARBON FIBER MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2023

FIGURE 49 MILLED CARBON FIBER MARKET: EV/EBITDA OF KEY VENDORS

FIGURE 50 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY VENDORS

FIGURE 51 TORAY INDUSTRIES, INC.: COMPANY SNAPSHOT

FIGURE 52 TEIJIN LIMITED: COMPANY SNAPSHOT

FIGURE 53 SGL CARBON: COMPANY SNAPSHOT

FIGURE 54 MITSUBISHI CHEMICAL GROUP CORPORATION: COMPANY SNAPSHOT

FIGURE 55 DAIGAS GROUP: COMPANY SNAPSHOT

Growth opportunities and latent adjacency in Milled Carbon Fiber Market