The research study involved four major activities in estimating the size of the education smart display market. Exhaustive secondary research has been done to collect important information about the market and peer markets. The validation of these findings, assumptions, and sizing with the help of primary research with industry experts across the value chain has been the next step. Both top-down and bottom-up approaches have been used to estimate the market size. Post which the market breakdown and data triangulation have been adopted to estimate the market sizes of segments and sub-segments.

Secondary Research

In secondary research, various secondary sources have been referred to for obtaining the information that was needed for the study. Various secondary sources that were used for the research include corporate filings such as annual reports, press releases, investor presentations, and financial statements; trade, business, and professional associations; whitepapers, journals, certified publications, and articles from recognized authors and databases.

In the education smart display report, the top-down as well as bottom-up approaches have been used for the estimation of the global market size, along with several other dependent submarkets. The major players in the market were identified with the help of extensive secondary research and their presence in the market was determined using secondary and primary research. All the percentage shares, splits, and breakdowns have been determined using secondary sources and verified through primary sources.

Primary Research

Extensive primary research has been conducted after understanding the education smart display market scenario through secondary research. Several primary interviews have been conducted with key opinion leaders from both demand- and supply-side vendors across four major regions— North America, Europe, Asia Pacific, and the Rest of the World. Approximately 25% of the primary interviews have been conducted with the demand-side vendors and 75% with the supply-side vendors. Primary data has been collected mainly through telephonic interviews, which consist of 80% of the total primary interviews; questionnaires and emails have also been used to collect the data.

After successful interaction with industry experts, brief sessions were conducted with highly experienced independent consultants to reinforce the findings of our primary research. This, along with the in-house subject matter experts’ opinions, has led us to the findings as described in the report.

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

In the market engineering process, both top-down and bottom-up approaches along with data triangulation methods have been used to estimate and validate the size of the education smart display market and other dependent submarkets. The research methodology used to estimate the market sizes includes the following:

-

Initially, the focus was on top line investments and spending in the ecosystem. Further the segment level splits and major developments in the market have been considered.

-

Identifying different stakeholders in the education smart displays market that influence the entire market, along with participants across the supply chain

-

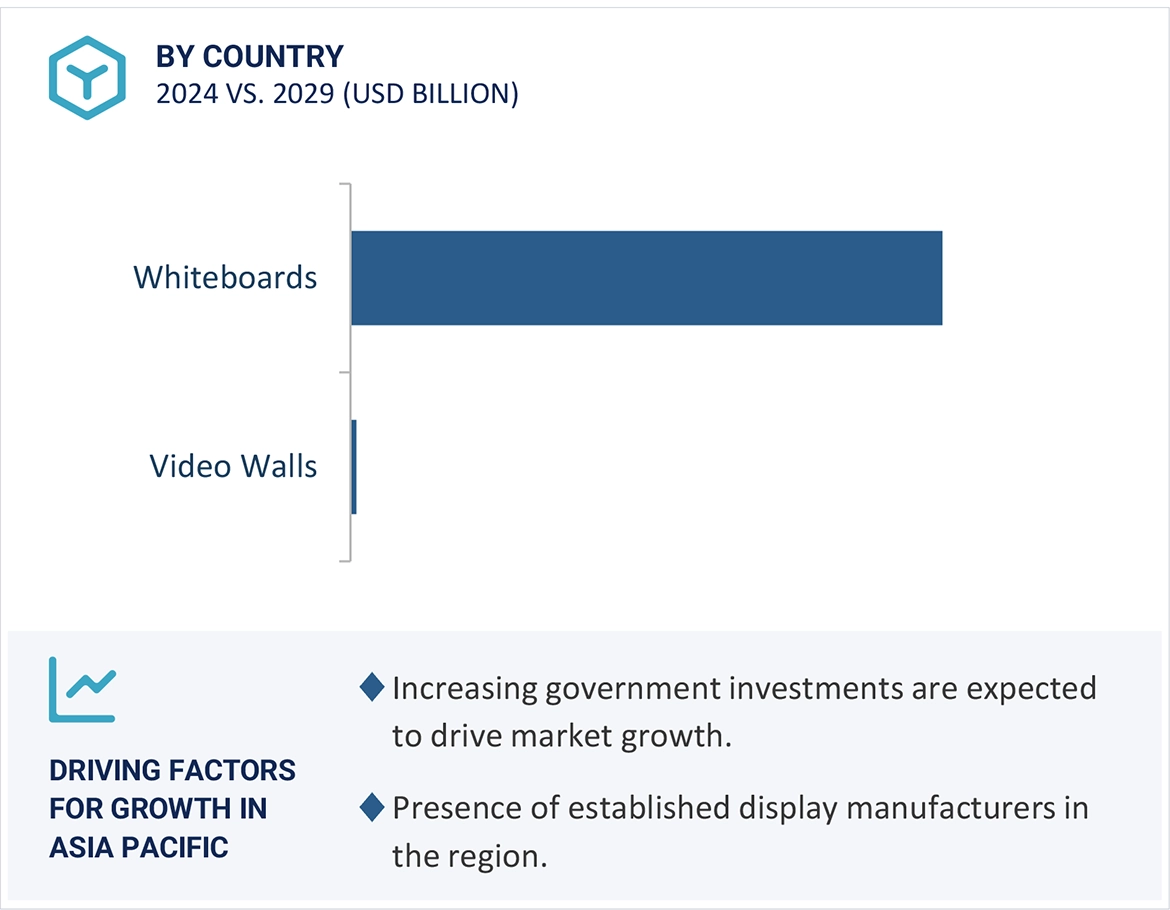

Analyzing major manufacturers of whiteboards and video walls for education as well as studying their product portfolios

-

Analyzing trends related to the adoption of whiteboards and video walls

-

Tracking the recent and upcoming developments in the market that include investments, R&D activities, product launches, collaborations, mergers & acquisitions, and partnerships as well as forecasting the market size based on these developments and other critical parameters

-

Carrying out multiple discussions with key opinion leaders to identify the trends in the adoption of whiteboards and video walls

-

Segmenting the overall market into various other market segments

-

Validating the estimates at each level through discussions with key opinion leaders, such as chief executives (CXOs), directors, and operation managers, and finally with the domain experts at MarketsandMarkets

Market Size Estimation Methodology-Bottom-up Approach

Market Size Estimation Methodology-Top-Down Approach

Data Triangulation

After arriving at the overall market size through the market size estimation process explained in the earlier section, the overall education smart displays market has been divided into several segments and subsegments. To complete the overall market engineering process and arrive at the exact statistics for all segments, the data triangulation and market breakdown procedures have been used, wherever applicable. The data has been triangulated by studying various factors and trends from both, the demand and supply side perspectives. Along with the data triangulation and market breakdown procedures, the market has been validated through the top-down and bottom-up approaches.

Market Definition

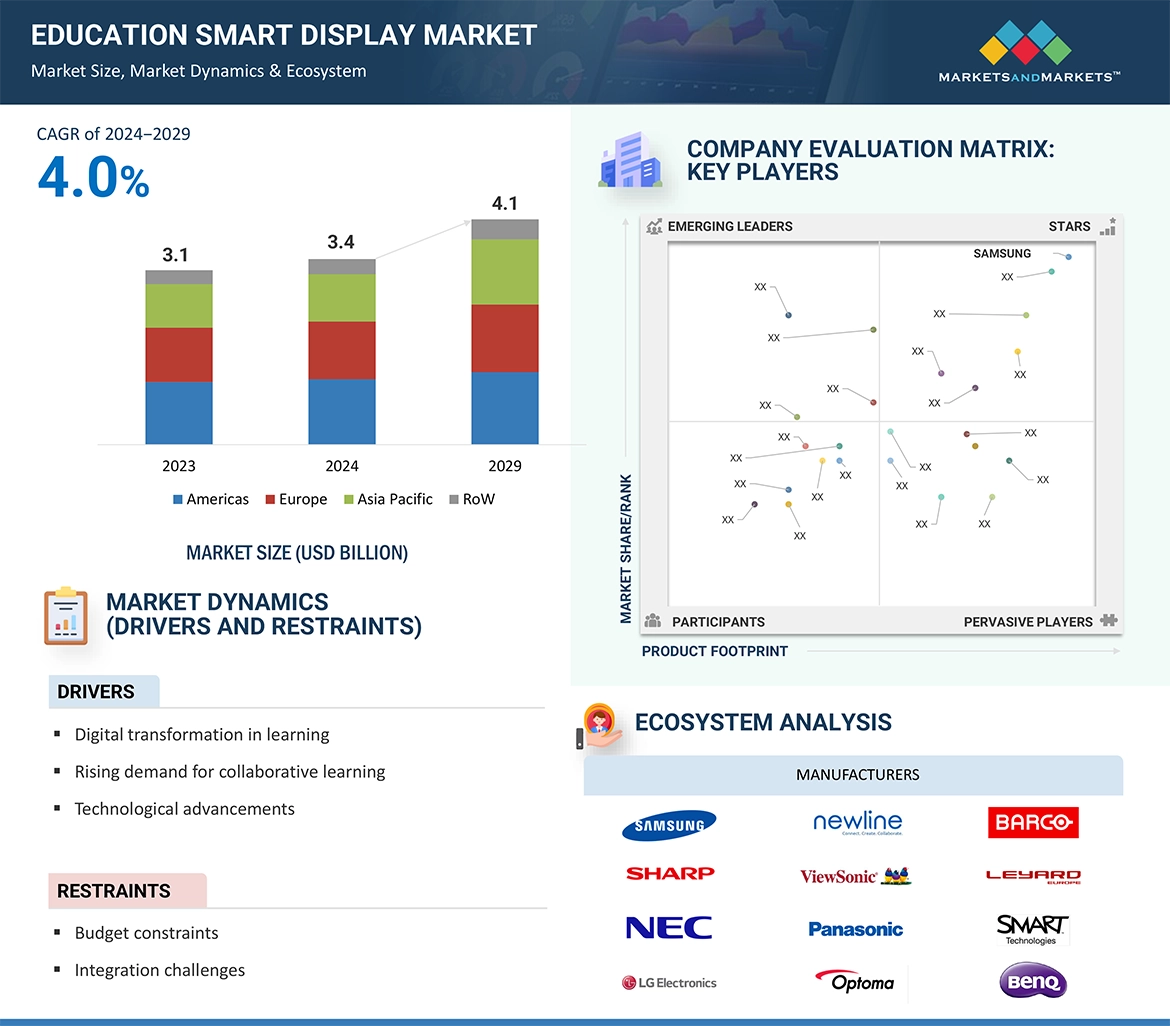

The education smart displays market refers to the industry segment that involves the production, distribution, and adoption of interactive display solutions designed specifically for educational environments. These displays are equipped with advanced technologies such as touchscreens, high resolutions, and interactive functionalities to enhance the learning experience in classrooms and other educational settings.

Education smart displays are tailored to support modern teaching methodologies, foster collaborative learning, and provide interactive content delivery. The market encompasses a range of display sizes, formats, and features that cater to the diverse needs of educational institutions, from primary schools to universities. The primary goal is to leverage technology to create dynamic, engaging, and interactive learning environments, contributing to the digital transformation of education.

Key Stakeholders

-

Raw Material Supplier

-

Manufacturers

-

Technology Providers

-

Government and Regulatory Bodies

-

IT Support and Service Providers

-

Educational Institutions

-

Investors and Financial Institutions

-

Industry Associations

-

Content Developers

The main objectives of this study are as follows:

-

To define, analyze, and forecast the education smart display market size, based on product type, display technology, display size and region in terms of value

-

To define, analyze, and forecast the market size, based on product type, and display size in terms of volume

-

To forecast the market size for various segments with respect to four main regions, namely, North America, Europe, Asia Pacific, and Rest of the World

-

To provide detailed information regarding the major drivers, restraints, opportunities, and challenges influencing the growth of the market

-

To study the complete value chain and related industry segments for the market

-

To strategically analyze the micromarkets1 with respect to individual growth trends, prospects, and contributions to the total market

-

To analyze trends and disruptions; pricing trends; patents and innovations; trade data (export and import data); regulatory environment; Porter's five forces analysis; case studies; key stakeholders & buying criteria; technology trends; the market ecosystem; and key conferences and events related to the education smart displays market

-

To analyze opportunities in the market for various stakeholders by identifying the high-growth segments of the market

-

To strategically profile the key players and comprehensively analyze their market positions in terms of ranking and core competencies2, along with the detailed the competitive landscape for the market leaders

-

To analyze competitive developments such as product launches/developments, expansions, acquisitions, partnerships, collaborations, agreements, and research & development (R&D) activities carried out by players in the market, strategically profile the key players and comprehensively analyze their market position in terms of ranking and core competencies2, along with detailing the competitive landscape for the market leaders

-

To analyze competitive developments such as product launches/developments, expansions, acquisitions, partnerships, collaborations, agreements, and research and development (R&D) activities carried out by players in the education smart display market

Available Customizations:

With the given market data, MarketsandMarkets offers customizations according to the specific requirements of companies. The following customization options are available for the report:

Country-wise Information:

-

Country-wise breakdown for Americas, Europe, Asia Pacific, and Rest of the World

Company Information:

-

Detailed analysis and profiling of additional market players (up to five)

Growth opportunities and latent adjacency in Education Smart Display Market