Aerospace Testing Market Size, Share and Trends

Aerospace Testing Market by Material Testing, Environmental Testing, Structural/Component Testing, Avionics/Flight & Electronics Testing, Propulsion System Testing, In-house, Commercial, Military & Defense, Space Exploration - Global Forecast to 2030

OVERVIEW

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

The aerospace testing market is projected to reach USD 6.91 billion by 2030 from USD 5.50 billion in 2025, at a CAGR of 4.6% from 2025 to 2030. The growth of the aerospace testing market is driven by the rising demand for commercial aircraft in developing economies, and growing use of UAVs in military and commercial applications

KEY TAKEAWAYS

-

By RegionThe North America aerospace testing market dominated with a 39.2% revenue share in 2024.

-

By End UserBy end user, the space exploration segment is expected to register the highest CAGR of 7.4%.

-

By Testing TypeBy testing type, the avionics/flight & electronics testing segment is projected to grow at the fastest rate from 2025 to 2030.

-

By SourcingBy sourcing, the outsourced segment is expected to register the highest CAGR of 5.7%.

-

Competitive LandscapeSGS, Intertek, and Element Materials Technology stand out as Star players in the aerospace testing market thanks to their global lab networks, strong accreditation depth, and end-to-end testing capabilities. Their expertise across materials, NDT, environmental, engine, and avionics testing helps OEMs and Tier-1 suppliers speed up certification and reduce program risk. Continuous investments in advanced test rigs and aerospace-grade quality systems further strengthen their leadership and industry trust.

-

Competitive LandscapeAstroscale and Accion Systems stand out as high-potential startups in the aerospace testing space, driven by cutting-edge satellite servicing and propulsion technologies that require intensive qualification and verification. Their rapid innovation and agile development models position them as emerging disruptors in next-generation space systems testing

The aerospace testing industry is growing steadily as next-gen aircraft, engines, and space systems demand higher reliability and tighter certification standards. With advanced materials, electrified propulsion, and complex avionics becoming mainstream, traditional testing methods fall short, driving strong adoption of advanced structural, environmental, and performance testing solutions.

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The aerospace testing market is rapidly evolving as AI-driven predictive tools, digital twins, and advanced NDT reshape how modern aircraft are validated. Beyond traditional structural and environmental testing, the sector is shifting toward hot areas like structural health monitoring, autonomous systems, and avionics cybersecurity. With rising demand for lightweight materials, fuel efficiency, and stricter safety compliance, customers now expect faster cycles, higher reliability, and lower maintenance costs. This transformation is unlocking new growth opportunities and pushing the industry toward smarter, more sustainable testing practices.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

MARKET DYNAMICS

Level

-

Rising demand for commercial aircraft in developing economies

-

Growing use of UAVs in military and commercial applications

Level

-

Complex and time-consuming testing process due to stringent regulations

Level

-

Development of advanced aircraft technologies creating need for specialized testing

-

Need for new testing methodologies to cater to evolving aerospace technologies

Level

-

Budget constraints necessitating aerospace companies to cut testing costs

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Rising demand for commercial aircraft in developing economies

Rapid urbanization and a growing middle class in developing economies are increasing the demand for air travel. This trend is expected to continue as economic growth in these regions sustains the need for larger commercial fleets and new aircraft models, driving the aerospace testing market to ensure quality and safety standards.

Restraint: Complex and time-consuming testing process due to stringent regulations

The aerospace industry is highly regulated, with stringent safety and quality standards to protect passengers and ensure operational integrity. Meeting these regulatory requirements can be complex, requiring extensive documentation, rigorous testing, and validation processes that significantly increase time and costs. As regulations evolve, staying compliant can become even more challenging, limiting the speed and flexibility of the aerospace testing process.

Opportunity: Development of advanced aircraft technologies creating need for specialized testing

As aerospace companies develop new technologies, such as lightweight materials, hybrid-electric propulsion systems, and autonomous flight capabilities, there is an increasing demand for specialized testing to validate these advancements. Ensuring safety, reliability, and regulatory compliance for these novel technologies requires tailored testing solutions, presenting a significant growth opportunity for the aerospace testing market.

Challenge: Budget constraints necessitating aerospace companies to cut testing costs

Aerospace companies often face budget constraints due to rising operational costs, such as increased prices for raw materials, fuel, and labor, along with ongoing supply chain disruptions that further inflate expenses. These financial pressures can lead companies to prioritize cost-cutting measures, including reductions in testing budgets. Additionally, competitive pressures to release new technologies quickly may drive companies to streamline or limit testing to maintain speed to market.

AEROSPACE TESTING MARKET SIZE, SHARE AND TRENDS: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Full-scale structural testing, fatigue testing, and vibration analysis for commercial aircraft platforms (737, 787). | Ensures airframe durability, improves safety margins, reduces maintenance risk, and accelerates certification timelines. |

|

Environmental, climatic, and materials testing for composite-rich aircraft such as the A350 and A320neo. | Enhances material reliability, validates performance under extreme conditions, and supports lightweight design adoption. |

|

Aerodynamic, thermal, and propulsion testing for defense aircraft (F-35, F-22) and hypersonic systems. | Boosts mission reliability, validates high-speed performance, and supports advanced propulsion innovations. |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET ECOSYSTEM

The aerospace testing companies ecosystem comprises three key segments: component manufacturers, testing service providers, and end users. Aerospace component manufacturers like GE Aerospace, Collins Aerospace, Airbus, Honeywell, and Safran design and produce essential parts and systems for aircraft and spacecraft, setting the foundation for testing requirements. Aerospace testing service providers such as DEKRA, TÜV SÜD, Eurofins, TÜV Rheinland, and Intertek play a critical role in validating safety, performance, and regulatory compliance, offering specialized testing services across materials, electronics, and structural components. Finally, end users, including major aerospace companies like SpaceX, Boeing, NASA, Northrop Grumman, and Raytheon Technologies, rely on these tested components and systems to innovate and operate in the aerospace sectors, from commercial aviation to defense and space exploration.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

aerospace testing Market, By Testing Type

The avionics/flight & electronics testing segment is projected to register the highest CAGR during the forecast period. This high growth is attributed to the rapid advancements in aircraft electronics, including next-generation flight control systems, communication technologies, navigation systems, and autonomous systems. As aircraft become more reliant on sophisticated electronics to enhance safety, efficiency, and performance, rigorous testing of these systems becomes increasingly critical. The rise of electric aircraft and the growing demand for unmanned aerial vehicles (UAVs) further drive the need for comprehensive avionics testing.

aerospace testing Market, By Sourcing

The in-house sourcing segment is expected to dominate the aerospace testing market due to the highly specialized and stringent requirements involved in aerospace testing. Many aerospace companies prefer to keep testing operations in-house to maintain greater control over the quality, security, and confidentiality of sensitive data and proprietary technologies. Additionally, having in-house capabilities allows for faster turnaround times, customization of testing processes, and seamless integration into the development and production workflow.

aerospace testing Market, By End User

In 2024, the commercial aviation sector dominates the aerospace testing market, primarily due to the continuous demand for new aircraft to accommodate growing global air travel. Factors such as increasing passenger traffic, fleet expansion by airlines, and the need for more fuel-efficient, next-generation aircraft contribute to the dominance of this segment. Additionally, the emphasis on safety, regulatory compliance, and performance optimization in commercial aviation leads to rigorous testing requirements. Aircraft manufacturers and operators prioritize extensive material, structural, environmental, and electronic testing to ensure safety and reliability, which is driving the growth of aerospace testing in the commercial segment.

REGION

Asia Pacific to be fastest-growing region in global aerospace testing market during forecast period

The aerospace testing market is experiencing the fastest growth in the Asia Pacific region. The region's rapid economic growth, particularly in countries like China, India, and Japan, is driving an increase in both commercial and military aircraft production. The rising demand for air travel, fueled by expanding middle-class populations and urbanization, is pushing airlines to invest in new, fuel-efficient aircraft. This, in turn, is driving the demand for comprehensive aerospace testing services. Moreover, governments in Asia Pacific are investing significantly in defense and space programs. All these factors are boosting the need for specialized testing services in Asia Pacific.

AEROSPACE TESTING MARKET SIZE, SHARE AND TRENDS: COMPANY EVALUATION MATRIX

In the aerospace testing market matrix, SGS stands firmly in the Leaders' Quadrant for third-party Inspection, Testing, and Certification (TIC), with a dominant global network and comprehensive service offerings for the entire aerospace value chain (including NDT, materials, and certification). Airbus, positioned as a emerging leader, is strengthening its footprint through its massive, in-house OEM testing capabilities for new aircraft development, cutting-edge R&D, and proprietary test facility operation.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

KEY MARKET PLAYERS

- Element Materials Technology (UK)

- SGS SA (Switzerland)

- Intertek Group plc (UK)

- Applus+ (Spain)

- TÜV SÜD (Germany)

- TÜV RHEINLAND (Germany)

- TÜV NORD Group (Germany)

- Rohde & Schwarz (Germany)

- Eurofins Scientific (Luxembourg)

- The Boeing Company (US)

- Airbus (Netherlands)

- MISTRAS Group (US)

- Lockheed Martin Corporation (US)

- Bureau Veritas (France)

- DEKRA (Germany)

MARKET SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size in 2025 (Value) | USD 5.50 Billion |

| Market Forecast in 2030 (Value) | USD 6.91 Billion |

| Growth Rate | CAGR of 4.6% from 2025-2030 |

| Years Considered | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments Covered |

|

| Regions Covered | North America, Asia Pacific, Europe, Rest of the World |

WHAT IS IN IT FOR YOU: AEROSPACE TESTING MARKET SIZE, SHARE AND TRENDS REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Leading Indian Aerospace OEM |

|

|

| Global Tier-1 Aerospace Test System Supplier |

|

|

| International Propulsion Test Equipment Manufacturer |

|

|

RECENT DEVELOPMENTS

- October 2024 : TÜV Rheinland acquired Safetec Nordic AS, a Norwegian consulting firm specializing in risk management and safety solutions. This acquisition strengthens TÜV Rheinland’s services in safety engineering, particularly in sectors such as oil & gas, transportation, and other high-risk industries. The addition of Safetec enhances TÜV Rheinland’s capabilities in managing risks related to safety, environmental impact, and technical integrity, aligning with their mission to provide comprehensive safety services worldwide.

- September 2024 : TÜV Rheinland acquired ICARO, an Italian engineering and consulting firm specializing in health, safety, environment, and process safety (HSE). The acquisition aligns with TÜV Rheinland’s strategy to strengthen its service offerings in the energy and environmental sectors, expanding its capabilities in Italy.

- August 2024 : Boeing partnered with AI Engineering Services Limited (AIESL) to enhance maintenance, repair, and overhaul (MRO) services for the Indian Navy’s P-8I fleet. The partnership will focus on in-country component repairs and landing gear overhauls, supporting the long-term sustainment of the P-8I aircraft. This partnership strengthens Boeing’s commitment to local capabilities, advancing India’s defense industry self-reliance.

- April 2024 : Bureau Veritas partnered with ST Engineering to support the development of AirX’s Wing Ground Technology, which aims to enhance operational efficiency in aviation. This collaboration focuses on optimizing aircraft maintenance and reducing downtime through innovative inspection and testing techniques. The partnership will leverage Bureau Veritas’ expertise in testing and certification to ensure compliance with safety standards, helping to improve the reliability of aircraft maintenance procedures while integrating advanced technologies into the aviation sector.

- April 2024 : Bureau Veritas collaborated with French airline Amelia (Regourd Aviation) to achieve the highest operational safety and regulatory compliance standards. This collaboration aimed to enhance Amelia’s safety measures and certification processes, which aligned with stringent aviation regulations.

- COLUMN 'A' SHOULD BE IN TEXT FORMAT AND NOT DATE FORMAT :

Table of Contents

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Methodology

The research study involved four major steps in estimating the size of the aerospace testing market. Exhaustive secondary research has been done to collect important information about the market and peer markets. The next step has been to validate these findings and assumptions and size them with the help of primary research with industry experts across the value chain. Both top-down and bottom-up approaches have been used to estimate the market size. After this, the market breakdown and data triangulation approaches have been adopted to estimate the market sizes of segments and subsegments.

Secondary Research

In the secondary research process, various secondary sources were referred to to identify and collect information required for this study. The secondary sources include annual reports, press releases, investor presentations of companies, white papers, and articles from recognized authors. Secondary research has been mainly done to obtain key information about the market’s value chain, the pool of key market players, market segmentation according to industry trends, regional outlook, and developments from market and technology perspectives.

In the aerospace testing market report, the global market size has been estimated using the top-down and bottom-up approaches, along with several other dependent submarkets. The major players in the market were identified using extensive secondary research, and their presence in the market was determined using secondary and primary research. All the percentage splits and breakdowns have been determined using secondary sources and verified through primary sources.

Primary Research

Extensive primary research has been conducted after understanding the aerospace testing market scenario through secondary research. Several primary interviews have been conducted with key opinion leaders from demand- and supply-side vendors across four major regions—North America, Europe, Asia Pacific, and RoW. Approximately 25% of the primary interviews have been conducted with the demand-side vendors and 75% with the supply-side vendors. Primary data has been collected mainly through telephonic interviews, which consist of 80% of the total primary interviews; questionnaires and emails have also been used to collect the data.

After successful interaction with industry experts, brief sessions were conducted with highly experienced independent consultants to reinforce the findings of our primary research. This, along with the in-house subject matter experts’ opinions, has led us to the findings as described in the report. The breakdown of primary respondents is as follows:

Note: “Others” includes sales, marketing, and product managers

About the assumptions considered for the study, To know download the pdf brochure

Market Size Estimation

In the complete market engineering process, top-down and bottom-up approaches and several data triangulation methods have been used to estimate and forecast the market size for the overall market segments and subsegments listed in this report. Extensive qualitative and quantitative analyses have been performed on the complete market engineering process to list the key information/insights throughout the report. The following table explains the process flow of the market size estimation.

The key players in the aerospace testing market were identified through secondary research, and their rankings in the respective regions were determined through primary and secondary research. This entire procedure involved the study of the annual and financial reports of top players, and interviews with industry experts, such as chief executive officers, vice presidents, directors, and marketing executives, for quantitative and qualitative key insights. All percentage shares, splits, and breakdowns were determined using secondary sources and verified through primary sources. All parameters that affect the markets covered in this research study were accounted for, viewed in extensive detail, verified through primary research, and analyzed to obtain the final quantitative and qualitative data. This data was consolidated, supplemented with detailed inputs and analysis from MarketsandMarkets, and presented in this report.

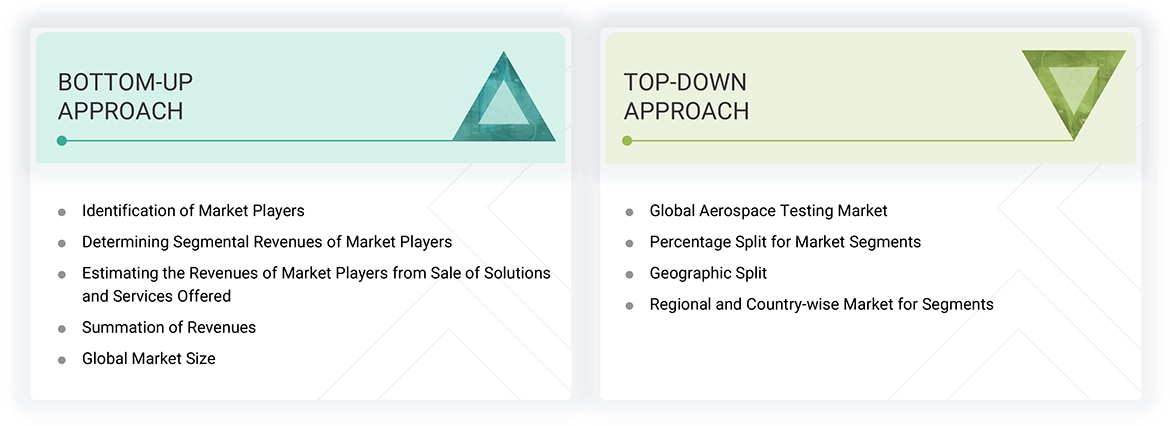

Bottom-Up Approach

- Major companies that provide aerospace testing services were identified. This included analyzing company portfolios, service offerings, and presence across various regions.

- The segment-specific revenues of the companies, particularly those related to aerospace testing, were determined.

- These individual revenue figures were compiled to determine the total revenue generated across the identified companies within the sector.

- Using this consolidated data, the global market size for aerospace testing was obtained.

Top-Down Approach

- Estimated the overall aerospace testing market size, then segmented the global market by allocating shares to in-house and outsourced sources to determine the aerospace testing market by sourcing type

- Estimated the aerospace testing market size by end users by assigning end user penetration splits to the global aerospace testing market based on their respective proportions of testing demand

- Applied market share splits to the global aerospace testing market to derive the market segmentation, by testing type

- Distributed the testing types across regions and countries by aligning regional aerospace activity with economic indicators, aerospace manufacturing presence, and national development initiatives

Aerospace Testing Market : Top-Down and Bottom-Up Approach

Data Triangulation

After arriving at the overall market size-using the market size estimation processes as explained above—the market has been split into several segments and subsegments. Data triangulation and market breakdown procedures have been employed to complete the entire market engineering process and arrive at the exact statistics of each market segment and subsegment. The data has been triangulated by studying various factors and trends from the demand and supply sides in the aerospace testing market.

Market Definition

The aerospace sector encompasses designing, developing, producing, and maintaining aircraft (airplanes, helicopters, gliders, and balloons) and spacecraft (satellites, space probes, orbital stations, and shuttles) and their component parts and accessories for civilian and military purposes. In this broader industry, the aerospace testing market is committed to inspecting and verifying these components to determine that they can meet rigorous standards of safety, performance, and regulation. The aerospace testing industry encompasses a wide range of specialist test services, such as material testing to evaluate the strength, durability, and compatibility of materials used; environmental testing to simulate harsh operating conditions, such as temperature, pressure, humidity, and vibration; structural/component testing to validate the integrity and performance of assembled structures and critical components; avionics, flight, and electronics testing to validate reliability and accuracy of onboard systems, sensors, and software; and propulsion system testing to validate engine efficiency, thrust, and operating safety. These testing procedures ensure the early detection of weaknesses or faults, enhancing the overall safety, functionality, and reliability of aerospace systems.

Key Stakeholders

- Raw Material Suppliers

- Aerospace Component Manufacturers

- Testing and Certification Agencies

- Testing Service Providers

- Suppliers and Component Manufacturers

- Research and Development Institutions

- Regulatory Bodies

- Consulting Firms

- Testing Laboratories

- Military and Defense Agencies

- Airlines and Operators

- Industry Associations

- Investors and Financial Institutions

Report Objectives

- To define, describe, segment, and forecast the aerospace testing market, testing type, sourcing type, and end user, in terms of value

- To describe and forecast the market for various segments, with respect to four main regions: North America, Europe, Asia Pacific, and RoW, in terms of value

- To provide detailed information regarding drivers, restraints, opportunities, and challenges influencing the growth of the aerospace testing market

- To provide a detailed overview of the aerospace testing market’s supply chain, along with the ecosystem, technology trends, use cases, regulatory environment, and Porter’s five forces analysis for the market

- To analyze industry trends, patents and innovations, and trade data (export and import data) related to aerospace testing

- To strategically analyze the micromarkets with respect to individual growth trends, prospects, and contributions to the total market

- To strategically profile the key players and comprehensively analyze their market share and core competencies

- To analyze opportunities for stakeholders and provide a detailed competitive landscape of the market

- To analyze competitive developments, such as solution/service launches/developments, collaborations, agreements, partnerships, acquisitions, and research & development (R&D), carried out by players in the aerospace testing market

- To profile key players in the aerospace testing market and comprehensively analyze their market ranking based on their revenue, market share, and core competencies

Available Customizations

With the given market data, MarketsandMarkets offers customizations according to the specific requirements of companies. The following customization options are available for the report:

- Detailed analysis and profiling of additional market players based on various blocks of the supply chain

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This ReportPersonalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the Aerospace Testing Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

Tetsuya Ohhira

Business Development Manager-Technology Business

Nikon Corporation,

Leading Japanese MNC specializing in optics and imaging productswww.nikon.com

MarketsandMarkets™ response

is quick. Their attitude is flexible and positive. Analyst Insights are globally considered and

significant. Client Services quickly respond to our inquiry and demand. Their wide range of global

surveys help us make our strategic plan.

We hope Knowledge Store will be easier to search

for a report.

VP - Marketing & Business Development

Leading Provider of Process Control Solutions

We engaged with MarketsandMarkets on a study to perform an analysis and recommend a Go-To-Market strategy for metrology and process control in the semiconductor market. The study was tailored to our targets and needs with well-defined milestones. Our overall experience with the MarketsandMarkets team was very good throughout the project in all aspects including the analysis methodologies used, the quality and depth of primary and secondary data sets, the professionalism and flexibility of the team and the ability to meet the target schedule and milestones. We want to thank MarketsandMarkets team for a job well done.

Growth opportunities and latent adjacency in Aerospace Testing Market

Harold

Apr, 2026

Will adoption of AI/GenAI in aerospace testing reduce total addressable revenue (through efficiency gains) or expand it (through higher testing complexity and iteration speed)?.

Bryan

Apr, 2026

Which testing category (material, fuel, structural, environmental) offers the highest long-term margin stability, and which is most vulnerable to commoditization?.