The study involved major activities in estimating the current size of the motor monitoring market. Exhaustive secondary research was done to collect information on the peer and parent markets. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the complete market size. Thereafter, market breakdown and data triangulation were used to estimate the market size of the segments and subsegments.

Secondary Research

This research study on the Motor monitoring market involved the use of extensive secondary sources, directories, and databases, such as The Energy Policy and Conservation Act of 1975 (EPCA), Electrical Appliances and Materials Safety Act, CE marking, The Electrical Equipment (Safety) Regulations 2016, UL 508, Energy Policy Act of 1992 (effective from 1997), International Organization for Standardization (ISO), ASTM International, National Electrical Manufacturers Association (NEMA) and International Electrotechnical Commission (IEC) to identify and collect information useful for a technical, market-oriented, and commercial study of the global Motor monitoring market. The other secondary sources included annual reports, press releases & investor presentations of companies, white papers, certified publications, articles by recognized authors, manufacturer associations, trade directories, and databases.

Primary Research

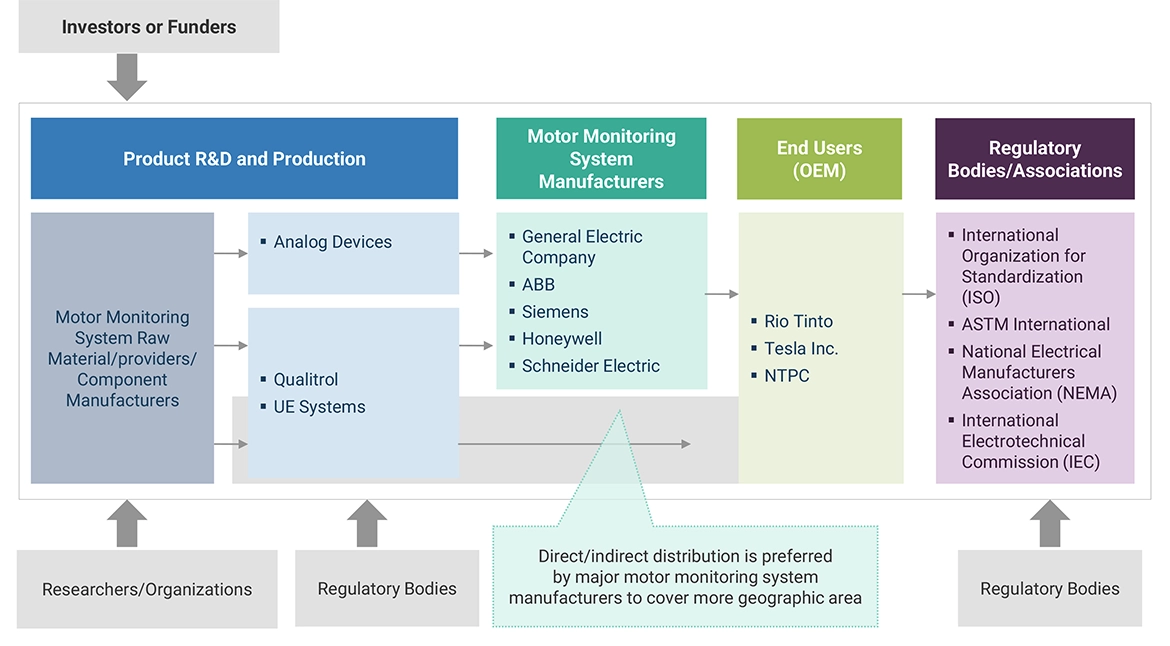

The motor monitoring market comprises several stakeholders such as motor monitoring manufacturers, manufacturers of subcomponents of motor monitoring, manufacturing technology providers, and technology support providers in the supply chain. The value chain of the motor monitoring market comprises research, design, and development centers, monitoring solution developers, system integrators, suppliers and distributors, end users, and post-sales service providers. The value chain model helps portray the service flow for motor monitoring development from the lab to various end users. It notionally estimates the value gained or lost by various stakeholders. The value chain model provides situational awareness of the drivers that influence the demand for motor monitoring.

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

Both top-down and bottom-up approaches were used to estimate and validate the total size of the Motor monitoring market. These methods were also used extensively to estimate the size of various subsegments in the market. The research methodology used to estimate the market size includes the following:

-

The key players in the industry and market have been identified through extensive secondary research, and their market share in the respective regions has been determined through both primary and secondary research.

-

The industry’s value chain and market size, in terms of value, have been determined through primary and secondary research processes.

-

All percentage shares, splits, and breakdowns have been determined using secondary sources and verified through primary sources.

Global Motor Monitoring Market Size: Top-down Approach

To know about the assumptions considered for the study, Request for Free Sample Report

Global Motor Monitoring Market Size: Bottom-Up Approach

Data Triangulation

After arriving at the overall market size from the estimation process explained above, the total market has been split into several segments and subsegments. To complete the overall market engineering process and arrive at the exact statistics for all the segments and subsegments, the data triangulation and market breakdown processes have been employed, wherever applicable. The data has been triangulated by studying various factors and trends from both the demand- and supply sides. Along with this, the market has been validated using both the top-down and bottom-up approaches.

Market Definition

Motor monitoring is the process of tracking the performance of motors to minimize downtime needed for repairs. It is one of the aspects of predictive maintenance. The failing machinery is predicted by monitoring the vibration or temperature of the motor case or the bearings; it can also be detected by monitoring and analyzing the current in the motor. Routine monitoring is the most effective strategy for detecting potential problems, and it can prompt invaluable follow-up inspections. Predictive maintenance has become a worldwide accepted practice and is being implemented and finely tuned by nearly every industry. Locating, defining, and acting on potential problems before they become catastrophic is the main objective of a predictive maintenance program.

Key Stakeholders

-

Technicians and repair personnel

-

Government and research organizations

-

Investment banks

-

End-user industries

-

Motor monitoring solution providers

-

Consulting companies

-

Associations, organizations, forums, and alliances related to motor monitoring solutions

-

Venture capitalists, private equity firms, and start-ups

-

Organizations, forums, alliances, and associations

-

State and national regulatory authorities

-

Venture capital firms

Objectives of the Study

-

To define, describe, segment, and forecast the motor monitoring market, in terms of value and volume, offering, deployment, end user, monitoring process and region

-

To forecast the market size for five key regions: North America, South America, Europe, Asia Pacific, and Middle East & Africa, along with their key countries

-

To provide detailed information about the key drivers, restraints, opportunities, and challenges influencing the growth of the market

-

To strategically analyze the subsegments with respect to individual growth trends, prospects, and contributions of each segment to the overall market size

-

To analyze market opportunities for stakeholders and the competitive landscape of the market

-

To strategically profile the key players and comprehensively analyze their market shares and core competencies

-

To analyze competitive developments, such as deals and agreements in the market

Available Customizations:

With the given market data, MarketsandMarkets offers customizations as per the client’s specific needs. The following customization options are available for this report:

Geographic Analysis

-

Further breakdown of region or country-specific analysis

Company Information

-

Detailed analyses and profiling of additional market players (up to 5)

Growth opportunities and latent adjacency in Motor Monitoring Market