TABLE OF CONTENTS

1 INTRODUCTION (Page No. - 28)

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION

1.3.2 INCLUSIONS AND EXCLUSIONS

1.4 YEARS CONSIDERED

1.5 CURRENCY CONSIDERED

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY (Page No. - 33)

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.2 PRIMARY DATA

2.1.2.1 Breakup of primary profiles

2.1.2.2 Key insights from industry experts

2.2 DATA TRIANGULATION

2.3 MARKET SIZE ESTIMATION

2.4 MARKET FORECAST

2.5 RESEARCH ASSUMPTIONS

2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY (Page No. - 43)

4 PREMIUM INSIGHTS (Page No. - 46)

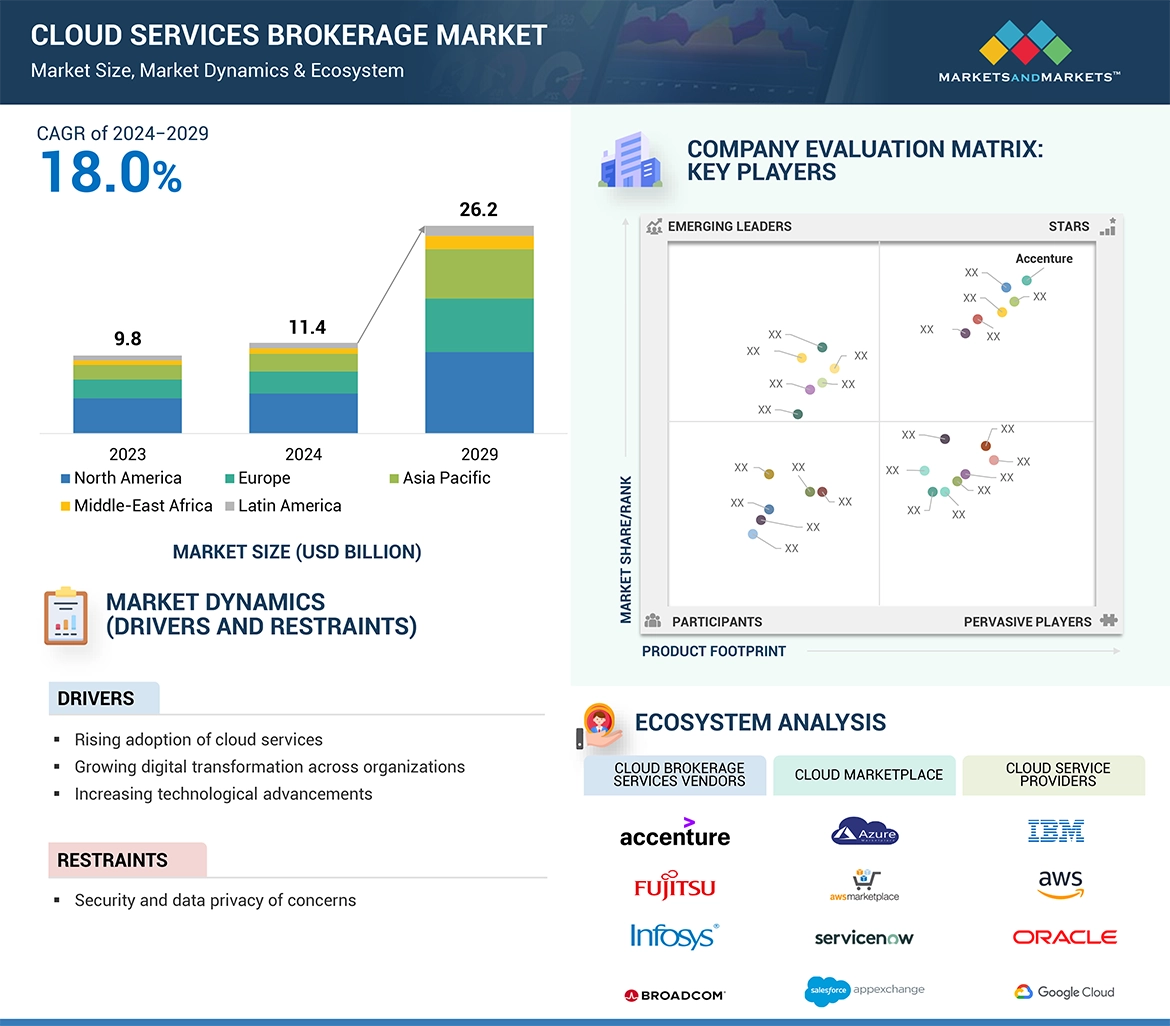

4.1 ATTRACTIVE OPPORTUNITIES FOR KEY PLAYERS IN CLOUD SERVICES BROKERAGE MARKET

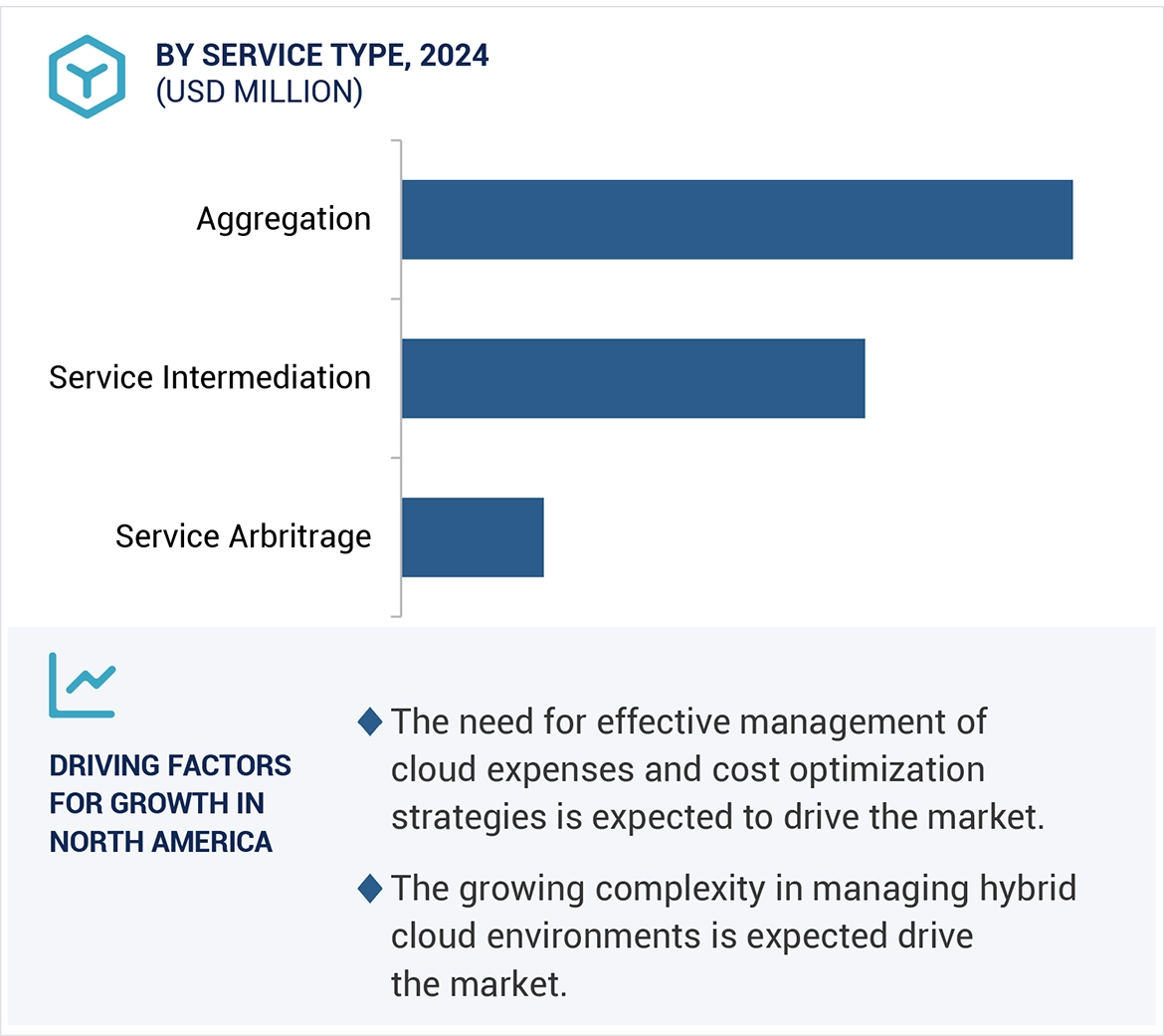

4.2 MARKET, BY SERVICE TYPE, 2024 VS. 2029

4.3 MARKET, BY CLOUD SERVICE MODEL 2024 VS. 2029

4.4 MARKET, BY ORGANIZATION SIZE, 2024 VS. 2029

4.5 MARKET, BY VERTICAL, 2024 VS. 2029

4.6 CLOUD SERVICES BROKERAGE MARKET: REGIONAL SCENARIO, 2024–2029

5 MARKET OVERVIEW AND INDUSTRY TRENDS (Page No. - 49)

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rising adoption of cloud services

5.2.1.2 Growing digital transformation across organizations

5.2.1.3 Increasing technological advancements

5.2.2 RESTRAINTS

5.2.2.1 Security and data privacy concerns

5.2.3 OPPORTUNITIES

5.2.3.1 Need for multi-cloud management

5.2.3.2 Need for optimized cost efficiency

5.2.4 CHALLENGES

5.2.4.1 Lack of skilled professionals

5.2.4.2 Integration of modern cloud solutions with legacy systems

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 PRICING ANALYSIS

5.4.1 AVERAGE SELLING PRICE (ASP) TREND OF KEY PLAYERS, BY SERVICE TYPE

5.5 SUPPLY CHAIN ANALYSIS

5.6 ECOSYSTEM

5.7 TECHNOLOGY ANALYSIS

5.7.1 KEY TECHNOLOGIES

5.7.1.1 Cloud management

5.7.1.2 Cloud cost management & optimization

5.7.1.3 Cloud governance

5.7.2 COMPLEMENTARY TECHNOLOGIES

5.7.2.1 Cloud storage

5.7.2.2 Cloud automation

5.7.2.3 API management

5.7.3 ADJACENT TECHNOLOGIES

5.7.3.1 Artificial Intelligence (AI)

5.7.3.2 Machine Learning (ML)

5.7.3.3 Data analytics and business intelligence

5.8 PATENT ANALYSIS

5.9 KEY CONFERENCES AND EVENTS IN 2024–2025

5.1 REGULATORY LANDSCAPE

5.10.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.10.2 REGULATIONS, BY REGION

5.11 PORTER’S FIVE FORCES ANALYSIS

5.11.1 THREAT OF NEW ENTRANTS

5.11.2 THREAT OF SUBSTITUTES

5.11.3 BARGAINING POWER OF BUYERS

5.11.4 BARGAINING POWER OF SUPPLIERS

5.11.5 INTENSITY OF COMPETITIVE RIVALRY

5.12 KEY STAKEHOLDERS AND BUYING CRITERIA

5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.12.2 BUYING CRITERIA

5.13 BUSINESS MODEL ANALYSIS

5.13.1 SUBSCRIPTION-BASED MODEL

5.13.2 PAY-AS-YOU-GO MODEL

5.14 INVESTMENT AND FUNDING SCENARIO

5.15 IMPACT OF AI/GEN AI IN CLOUD SERVICES BROKERAGE MARKET

5.15.1 INDUSTRY TRENDS: USE CASES

5.15.1.1 Lufthansa adopted IBM’s AI solutions for global management

5.15.1.2 Cerebriu accelerated AI model training and MRI workflows with Oracle Cloud

5.15.2 TOP CLIENTS ADOPTING AI/GEN AI

5.15.2.1 AWS

5.15.2.2 Accenture

5.16 CASE STUDY ANALYSIS

5.16.1 TELENOR STREAMLINED CLOUD FUNCTIONALITY BY DEPLOYING ARROWSPHERE’S SOLUTIONS

5.16.2 BRENNAN IT CHOSE CLOUDMORE TO OVERCOME BILLING AND CUSTOMER RELATIONSHIP MANAGEMENT

5.16.3 NTT DATA MANAGED CLOUD OPERATIONS FOR STRATEGIC BLUE

5.16.4 INFOSYS HELPED WESTERN DIGITAL STREAMLINE 3 ERPS WITH 1 CLOUD

5.16.5 WIPRO HELPED FOOD PROCESSING COMPANY IN OPERATING TECHNOLOGY GLOBALLY

5.16.6 COGNIZANT’S CCIB HELPED SPEED UP CLOUD OPERATION FOR TRANSPORT AND LOGISTIC FIRM

6 CLOUD SERVICES BROKERAGE MARKET, BY SERVICE TYPE (Page No. - 78)

6.1 INTRODUCTION

6.1.1 SERVICE TYPES: CLOUD SERVICES BROKERAGE MARKET DRIVERS

6.2 AGGREGATION

6.2.1 NEED TO OPTIMIZE CLOUD STRATEGIES, REDUCE VENDOR MANAGEMENT COMPLEXITY, AND LEVERAGE CLOUD TECHNOLOGIES TAILORED TO SPECIFIC NEEDS TO DRIVE MARKET

6.2.1.1 Multi-cloud management

6.2.1.2 Data integration

6.2.1.3 Automation & orchestration

6.3 SERVICE INTERMEDIATION

6.3.1 NEED TO ENHANCE CUSTOMER SUPPORT AND SERVICE CUSTOMIZATION ACROSS MULTIPLE CLOUD PROVIDERS

6.3.1.1 Security management

6.3.1.2 Performance & usage reporting

6.4 SERVICE ARBITRAGE

6.4.1 NEED FOR COST OPTIMIZATION AND AUGMENTING PERFORMANCE NEEDS TO FUEL DEMAND FOR SERVICE ARBITRAGE

6.4.1.1 Service catalog management

6.4.1.2 Marketplace integration

6.4.1.3 Enablement services

7 CLOUD SERVICES BROKERAGE MARKET, BY CLOUD SERVICE MODEL (Page No. - 87)

7.1 INTRODUCTION

7.1.1 CLOUD SERVICE MODELS: CLOUD SERVICES BROKERAGE MARKET DRIVERS

7.2 PLATFORM AS A SERVICE (PAAS)

7.2.1 NEED TO STREAMLINE APPLICATION DEVELOPMENT, REDUCE COMPLEXITY, AND ACCELERATE DEPLOYMENT TO FUEL DEMAND FOR PLATFORM AS A SERVICE (PAAS) MODELS

7.3 INFRASTRUCTURE AS A SERVICE (IAAS)

7.3.1 NEED TO OFFER SCALABLE, FLEXIBLE, AND COST-EFFECTIVE IT INFRASTRUCTURE TO BOOST DEMAND FOR INFRASTRUCTURE AS A SERVICE (IAAS) SOLUTIONS

7.4 SOFTWARE AS A SERVICE (SAAS)

7.4.1 NEED TO DELIVER SOFTWARE APPLICATIONS WITH AUTOMATIC UPDATES & MAINTENANCE AND REDUCING IT MANAGEMENT OVERHEAD & ENHANCING ACCESSIBILITY TO PROPEL MARKET

8 CLOUD SERVICES BROKERAGE MARKET, BY ORGANIZATION SIZE (Page No. - 93)

8.1 INTRODUCTION

8.1.1 ORGANIZATION SIZES: CLOUD SERVICES BROKERAGE MARKET DRIVERS

8.2 LARGE ENTERPRISES

8.2.1 LARGE ENTERPRISES TO STREAMLINE OPERATIONS, ENHANCE PERFORMANCE, AND MEET STRINGENT REGULATORY COMPLIANCE AND SECURITY STANDARDS WITH CLOUD SERVICES

8.3 MEDIUM ENTERPRISES

8.3.1 MEDIUM ENTERPRISES TO UTILIZE CLOUD SOLUTIONS TO BALANCE COST EFFICIENCY AND OPERATIONAL FLEXIBILITY

8.4 SMALL ENTERPRISES

8.4.1 NEED FOR AFFORDABILITY TO ACCESS ADVANCED CLOUD SOLUTIONS WITHOUT SIGNIFICANT UPFRONT COSTS TO EXPAND MARKET GROWTH

9 CLOUD SERVICES BROKERAGE MARKET, BY VERTICAL (Page No. - 99)

9.1 INTRODUCTION

9.1.1 VERTICALS: CLOUD SERVICES BROKERAGE MARKET DRIVERS

9.2 BFSI

9.2.1 NEED TO ENHANCE DATA MANAGEMENT, REGULATORY COMPLIANCE, AND DIGITAL INNOVATION TO BOLSTER DEMAND FOR CLOUD SERVICES

9.2.2 BFSI: APPLICATION AREAS

9.2.2.1 Hybrid & multi-cloud management

9.2.2.2 Cost optimization & management

9.2.2.3 Other BFSI application areas

9.3 TELECOMMUNICATIONS

9.3.1 TELECOMMUNICATIONS COMPANIES TO LEVERAGE CLOUD SERVICES TO OPTIMIZE NETWORK INFRASTRUCTURE, ENHANCE SERVICE DELIVERY, AND SUPPORT GROWING DEMAND FOR HIGH-BANDWIDTH APPLICATIONS

9.3.2 TELECOMMUNICATIONS: APPLICATION AREAS

9.3.2.1 Service aggregation & delivery

9.3.2.2 Network & infrastructure management

9.3.2.3 Other telecommunication application areas

9.4 IT & ITES

9.4.1 IT & ITES COMPANIES TO UTILIZE CLOUD SERVICES TO STREAMLINE OPERATIONS, ENHANCE SERVICE DELIVERY, AND DRIVE INNOVATION

9.4.2 IT & ITES: APPLICATION AREAS

9.4.2.1 IT operations & management

9.4.2.2 Cost management & optimization

9.4.2.3 Other IT & ITeS application areas

9.5 GOVERNMENT & PUBLIC SECTOR

9.5.1 NEED FOR ROBUST TOOLS FOR MANAGING DATA PROTECTION, COMPLIANCE WITH REGULATIONS, AND ENSURING INTEGRITY OF SENSITIVE INFORMATION TO DRIVE MARKET

9.5.2 GOVERNMENT & PUBLIC SECTOR: APPLICATION AREAS

9.5.2.1 Service integration

9.5.2.2 Compliance & security

9.5.2.3 Other government & public sector application areas

9.6 RETAIL & CONSUMER GOODS

9.6.1 NEED TO ANALYZE CONSUMER DATA, UNDERSTAND PURCHASING BEHAVIORS, AND DELIVER PERSONALIZED MARKETING AND PRODUCT RECOMMENDATIONS TO FUEL MARKET GROWTH

9.6.2 RETAIL & CONSUMER GOODS: APPLICATION AREAS

9.6.2.1 Customer experience enhancement

9.6.2.2 Vendor management & integration

9.6.2.3 Other retail & consumer goods application areas

9.7 MANUFACTURING

9.7.1 CLOUD SERVICES TO ANALYZE PRODUCTION DATA, MONITOR EQUIPMENT PERFORMANCE IN REAL-TIME, AND GAIN INSIGHTS INTO OPERATIONAL TRENDS IN MANUFACTURING SECTOR

9.7.2 MANUFACTURING: APPLICATION AREAS

9.7.2.1 Supply chain management

9.7.2.2 Predictive maintenance

9.7.2.3 Other manufacturing application areas

9.8 ENERGY & UTILITIES

9.8.1 NEED TO MODERNIZE OPERATIONS, ENHANCE EFFICIENCY, AND ADDRESS CHALLENGES OF RAPIDLY CHANGING ENERGY LANDSCAPE TO PROPEL MARKET

9.8.2 ENERGY & UTILITIES: APPLICATION AREAS

9.8.2.1 Predictive maintenance

9.8.2.2 Regulatory compliance & reporting

9.8.2.3 Other energy & utilities application areas

9.9 MEDIA & ENTERTAINMENT

9.9.1 SHIFT TOWARD REMOTE AND COLLABORATIVE WORKFLOWS IN CONTENT CREATION TO BOOST MARKET GROWTH

9.9.2 MEDIA & ENTERTAINMENT: APPLICATION AREAS

9.9.2.1 Media asset management

9.9.2.2 Content delivery & streaming

9.9.2.3 Other media & entertainment application areas

9.1 HEALTHCARE & LIFE SCIENCES

9.10.1 NEED FOR EFFICIENT DATA INTEGRATION AND MANAGEMENT TO ENHANCE PATIENT CARE AND ENSURE REGULATORY COMPLIANCE TO BOLSTER MARKET GROWTH

9.10.2 HEALTHCARE & LIFE SCIENCES: APPLICATION AREAS

9.10.2.1 Data integration & management

9.10.2.2 Cost management & optimization

9.10.2.3 Other healthcare & life sciences application areas

9.11 OTHER VERTICALS

10 CLOUD SERVICES BROKERAGE MARKET, BY REGION (Page No. - 121)

10.1 INTRODUCTION

10.2 NORTH AMERICA

10.2.1 NORTH AMERICA: MARKET DRIVERS

10.2.2 NORTH AMERICA: MACROECONOMIC OUTLOOK

10.2.3 US

10.2.3.1 Increased adoption of multi-cloud strategies for enhanced efficiency and presence of major players to drive market

10.2.4 CANADA

10.2.4.1 Investments from major tech companies and government initiatives to maintain regulatory frameworks and data protection standards to propel market

10.3 EUROPE

10.3.1 EUROPE: CLOUD SERVICES BROKERAGE MARKET DRIVERS

10.3.2 EUROPE: MACROECONOMIC OUTLOOK

10.3.3 UK

10.3.3.1 Widespread use of cloud technology and need for effective management to fuel market growth

10.3.4 GERMANY

10.3.4.1 Rising adoption of multi-cloud setups to boost efficiency and scalability investments to accelerate market growth

10.3.5 FRANCE

10.3.5.1 Digital transformation, regulatory needs, and need for cost-saving measures to foster market growth

10.3.6 ITALY

10.3.6.1 Need for cloud solutions that meet high-security standards and comply with strict regulations to boost market growth

10.3.7 REST OF EUROPE

10.4 ASIA PACIFIC

10.4.1 ASIA PACIFIC: CLOUD SERVICES BROKERAGE MARKET DRIVERS

10.4.2 ASIA PACIFIC: MACROECONOMIC OUTLOOK

10.4.3 CHINA

10.4.3.1 Supportive government policies, increasing cloud adoption across various sectors, and use of advanced technologies to bolster market growth

10.4.4 JAPAN

10.4.4.1 Technological innovations and deeper collaboration between service providers and brokerage firms from global vendors to drive market

10.4.5 INDIA

10.4.5.1 Shift from traditional services to cloud-based services and presence of major players to augment market growth

10.4.6 REST OF ASIA PACIFIC

10.5 MIDDLE EAST & AFRICA

10.5.1 MIDDLE EAST & AFRICA: CLOUD SERVICES BROKERAGE MARKET DRIVERS

10.5.2 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

10.5.3 GULF COOPERATION COUNCIL (GCC) COUNTRIES

10.5.3.1 UAE

10.5.3.1.1 Shift from oil-based economy to tech giant and rising focus on regulatory compliance to boost market growth

10.5.3.2 Saudi Arabia

10.5.3.2.1 Growing foreign investments and Vision 2030’s focus on digital transformation and economic diversification to accelerate market growth

10.5.3.3 Rest of GCC countries

10.5.4 SOUTH AFRICA

10.5.4.1 Rapid digital transformation and increasing cloud adoption to bolster demand for security testing

10.5.5 REST OF MIDDLE EAST & AFRICA

10.6 LATIN AMERICA

10.6.1 LATIN AMERICA: CLOUD SERVICES BROKERAGE MARKET DRIVERS

10.6.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

10.6.3 BRAZIL

10.6.3.1 Increasing demand for cloud services and digitalization in distinct industries by domestic and foreign companies and start-ups to propel market

10.6.4 MEXICO

10.6.4.1 Emergence of local players and need to save costs and boost digital transformation to foster market growth

10.6.5 REST OF LATIN AMERICA

11 COMPETITIVE LANDSCAPE (Page No. - 169)

11.1 OVERVIEW

11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

11.3 REVENUE ANALYSIS

11.4 MARKET SHARE ANALYSIS

11.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

11.5.1 STARS

11.5.2 EMERGING LEADERS

11.5.3 PERVASIVE PLAYERS

11.5.4 PARTICIPANTS

11.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023

11.5.5.1 Company footprint

11.5.5.2 Service type footprint

11.5.5.3 Organization size footprint

11.5.5.4 Vertical footprint

11.5.5.5 Regional footprint

11.6 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2023

11.6.1 PROGRESSIVE COMPANIES

11.6.2 RESPONSIVE COMPANIES

11.6.3 DYNAMIC COMPANIES

11.6.4 STARTING BLOCKS

11.6.5 COMPETITIVE BENCHMARKING: START-UPS/SMES, 2023

11.6.5.1 Key start-ups/SMEs

11.6.5.2 Competitive benchmarking of key start-ups/SMEs

11.7 COMPANY VALUATION AND FINANCIAL METRICS

11.8 BRAND/PRODUCT COMPARISON

11.8.1 ACCENTURE MYNAV

11.8.2 IBM Z/OS CLOUD BROKER

11.8.3 VMWARE TANZU CLOUD SERVICE BROKER

11.8.4 FUJITSU CLOUD SERVICE MANAGEMENT

11.9 COMPETITIVE SCENARIO AND TRENDS

11.9.1 PRODUCT LAUNCHES AND ENHANCEMENTS

11.9.2 DEALS

12 COMPANY PROFILES (Page No. - 187)

12.1 INTRODUCTION

12.2 MAJOR PLAYERS

12.2.1 ACCENTURE

12.2.1.1 Business overview

12.2.1.2 Products/Solutions/Services offered

12.2.1.3 Recent developments

12.2.1.3.1 Product launches

12.2.1.3.2 Deals

12.2.1.4 MnM view

12.2.1.4.1 Strategic choices

12.2.1.4.2 Weaknesses and competitive threats

12.2.2 IBM

12.2.2.1 Business overview

12.2.2.2 Products/Solutions/Services offered

12.2.2.3 Recent developments

12.2.2.3.1 Product enhancements

12.2.2.3.2 Deals

12.2.2.4 MnM view

12.2.2.4.1 Right to win

12.2.2.4.2 Strategic choices

12.2.2.4.3 Weaknesses and competitive threats

12.2.3 BROADCOM

12.2.3.1 Business overview

12.2.3.2 Products/Solutions/Services offered.

12.2.3.3 Recent developments

12.2.3.3.1 Product launches

12.2.3.3.2 Deals

12.2.3.4 MnM view

12.2.3.4.1 Right to win

12.2.3.4.2 Strategic choices

12.2.3.4.3 Weaknesses and competitive threats

12.2.4 ARROW ELECTRONICS

12.2.4.1 Business overview

12.2.4.2 Products/Solutions/Services offered

12.2.4.3 Recent developments

12.2.4.3.1 Product launches and enhancements

12.2.4.3.2 Deals

12.2.4.4 MnM view

12.2.4.4.1 Right to win

12.2.4.4.2 Strategic choices

12.2.4.4.3 Weaknesses and competitive threats

12.2.5 FUJITSU

12.2.5.1 Business overview

12.2.5.2 Products/Solutions/Services offered

12.2.5.3 Recent developments

12.2.5.3.1 Product launches

12.2.5.3.2 Deals

12.2.6 DXC TECHNOLOGY

12.2.6.1 Business overview

12.2.6.2 Products/Solutions/Services offered

12.2.6.3 Recent developments

12.2.6.3.1 Product launches

12.2.6.3.2 Deals

12.2.7 WIPRO

12.2.7.1 Business overview

12.2.7.2 Products/Solutions/Services offered

12.2.7.3 Recent developments

12.2.7.3.1 Deals

12.2.8 EVIDEN

12.2.8.1 Business overview

12.2.8.2 Products/Solutions/Services offered

12.2.8.3 Recent developments

12.2.8.3.1 Product launches

12.2.8.3.2 Deals

12.2.9 AWS

12.2.9.1 Business overview

12.2.9.2 Products/Solutions/Services offered

12.2.10 INFOSYS

12.2.10.1 Business overview

12.2.10.2 Products/Solutions/Services offered

12.2.10.3 Recent developments

12.2.10.3.1 Deals

12.2.11 NTT DATA

12.2.12 TCS

12.2.13 TECH MAHINDRA

12.2.14 BMC SOFTWARE

12.2.15 FLEXERA

12.2.16 JAMCRACKER

12.2.17 CLOUDMORE

12.2.18 ESHGRO

12.2.19 OPENTEXT

12.2.20 INCONTINUUM

12.2.21 COMPUNNEL

12.2.22 SHIVAAMI

12.2.23 BITTITAN

12.2.24 CAPGEMINI

12.2.25 ORACLE

12.2.26 CIGNEX

12.3 OTHER PLAYERS

12.3.1 ACTIVEPLATFORM

12.3.2 CLOUDFX

12.3.3 CLOUDBOLT

12.3.4 CLOUDSME

12.3.5 APPDIRECT

12.3.6 MORPHEUS DATA

12.3.7 INTERWORKS.CLOUD

12.3.8 RACKNAP

12.3.9 SPOT

12.3.10 CLOUDBROKER

13 ADJACENT AND RELATED MARKETS (Page No. - 244)

13.1 INTRODUCTION

13.1.1 RELATED MARKETS

13.2 CLOUD COMPUTING MARKET

13.3 MULTI-CLOUD MANAGEMENT MARKET

14 APPENDIX (Page No. - 251)

14.1 DISCUSSION GUIDE

14.2 KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

14.3 CUSTOMIZATION OPTIONS

14.4 RELATED REPORTS

14.5 AUTHOR DETAILS

LIST OF TABLES (244 TABLES)

TABLE 1 USD EXCHANGE RATES, 2018–2023

TABLE 2 FACTOR ANALYSIS

TABLE 3 AVERAGE SELLING PRICE OF KEY VENDORS FOR TOP THREE SERVICE TYPES

TABLE 4 INDICATIVE PRICING LEVELS OF CLOUD SERVICES BROKERAGE VENDORS

TABLE 5 CLOUD SERVICES BROKERAGE MARKET: ECOSYSTEM

TABLE 6 LIST OF MAJOR PATENTS FOR MARKET

TABLE 7 MARKET: LIST OF KEY CONFERENCES AND EVENTS, 2024–2025

TABLE 8 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 9 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 10 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 11 REST OF THE WORLD: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 12 PORTER’S FIVE FORCES’ IMPACT ON CLOUD SERVICES BROKERAGE MARKET

TABLE 13 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE VERTICALS

TABLE 14 KEY BUYING CRITERIA FOR TOP THREE VERTICALS

TABLE 15 MARKET, BY SERVICE TYPE, 2019–2023 (USD MILLION)

TABLE 16 MARKET, BY SERVICE TYPE, 2024–2029 (USD MILLION)

TABLE 17 AGGREGATION: MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 18 AGGREGATION: MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 19 SERVICE INTERMEDIATION: MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 20 SERVICE INTERMEDIATION: MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 21 SERVICE ARBITRAGE: MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 22 SERVICE ARBITRAGE: MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 23 CLOUD SERVICES BROKERAGE MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 24 MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 25 PLATFORM AS A SERVICE (PAAS): MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 26 PLATFORM AS A SERVICE (PAAS): MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 27 INFRASTRUCTURE AS A SERVICE (IAAS): MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 28 INFRASTRUCTURE AS A SERVICE (IAAS): MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 29 SOFTWARE AS A SERVICE (SAAS): MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 30 SOFTWARE AS A SERVICE (SAAS): MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 31 CLOUD SERVICES BROKERAGE MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 32 MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 33 LARGE ENTERPRISES: MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 34 LARGE ENTERPRISES: MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 35 MEDIUM ENTERPRISES: MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 36 MEDIUM ENTERPRISES: MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 37 SMALL ENTERPRISES: MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 38 SMALL ENTERPRISES: MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 39 CLOUD SERVICES BROKERAGE MARKET, BY VERTICAL, 2019–2023 (USD MILLION)

TABLE 40 MARKET, BY VERTICAL, 2024–2029 (USD MILLION)

TABLE 41 BFSI: MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 42 BFSI: MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 43 TELECOMMUNICATIONS: MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 44 TELECOMMUNICATIONS: MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 45 IT & ITES: MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 46 IT & ITES: MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 47 GOVERNMENT & PUBLIC SECTOR: MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 48 GOVERNMENT & PUBLIC SECTOR: MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 49 RETAIL & CONSUMER GOODS: CLOUD SERVICES BROKERAGE MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 50 RETAIL & CONSUMER GOODS: MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 51 MANUFACTURING: MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 52 MANUFACTURING: MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 53 ENERGY & UTILITIES: MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 54 ENERGY & UTILITIES: MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 55 MEDIA & ENTERTAINMENT: MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 56 MEDIA & ENTERTAINMENT: MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 57 HEALTHCARE & LIFE SCIENCES: MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 58 HEALTHCARE & LIFE SCIENCES: MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 59 OTHER VERTICALS: MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 60 OTHER VERTICALS: MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 61 MARKET, BY REGION, 2019–2023 (USD MILLION)

TABLE 62 CLOUD SERVICES BROKERAGE MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 63 NORTH AMERICA: MARKET, BY SERVICE TYPE, 2019–2023 (USD MILLION)

TABLE 64 NORTH AMERICA: MARKET, BY SERVICE TYPE, 2024–2029 (USD MILLION)

TABLE 65 NORTH AMERICA: MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 66 NORTH AMERICA: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 67 NORTH AMERICA: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 68 NORTH AMERICA: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 69 NORTH AMERICA: MARKET, BY VERTICAL, 2019–2023 (USD MILLION)

TABLE 70 NORTH AMERICA: MARKET, BY VERTICAL, 2024–2029 (USD MILLION)

TABLE 71 NORTH AMERICA: MARKET, BY COUNTRY, 2019–2023 (USD MILLION)

TABLE 72 NORTH AMERICA: MARKET, BY COUNTRY, 2024–2029 (USD MILLION)

TABLE 73 US: CLOUD SERVICES BROKERAGE MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 74 US: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 75 US: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 76 US: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 77 CANADA: MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 78 CANADA: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 79 CANADA: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 80 CANADA: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 81 EUROPE: CLOUD SERVICES BROKERAGE MARKET, BY SERVICE TYPE, 2019–2023 (USD MILLION)

TABLE 82 EUROPE: MARKET, BY SERVICE TYPE, 2024–2029 (USD MILLION)

TABLE 83 EUROPE: MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 84 EUROPE: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 85 EUROPE: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 86 EUROPE: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 87 EUROPE: MARKET, BY VERTICAL, 2019–2023 (USD MILLION)

TABLE 88 EUROPE: MARKET, BY VERTICAL, 2024–2029 (USD MILLION)

TABLE 89 EUROPE: MARKET, BY COUNTRY, 2019–2023 (USD MILLION)

TABLE 90 EUROPE: MARKET, BY COUNTRY, 2024–2029 (USD MILLION)

TABLE 91 UK: CLOUD SERVICES BROKERAGE MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 92 UK: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 93 UK: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 94 UK: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 95 GERMANY: MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 96 GERMANY: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 97 GERMANY: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 98 GERMANY: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 99 FRANCE: CLOUD SERVICES BROKERAGE MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 100 FRANCE: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 101 FRANCE: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 102 FRANCE: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 103 ITALY: MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 104 ITALY: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 105 ITALY: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 106 ITALY: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 107 REST OF EUROPE: MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 108 REST OF EUROPE: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 109 REST OF EUROPE: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 110 REST OF EUROPE: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 111 ASIA PACIFIC: CLOUD SERVICES BROKERAGE MARKET, BY SERVICE TYPE, 2019–2023 (USD MILLION)

TABLE 112 ASIA PACIFIC: MARKET, BY SERVICE TYPE, 2024–2029 (USD MILLION)

TABLE 113 ASIA PACIFIC: MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 114 ASIA PACIFIC: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 115 ASIA PACIFIC: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 116 ASIA PACIFIC: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 117 ASIA PACIFIC: MARKET, BY VERTICAL, 2019–2023 (USD MILLION)

TABLE 118 ASIA PACIFIC: MARKET, BY VERTICAL, 2024–2029 (USD MILLION)

TABLE 119 ASIA PACIFIC: MARKET, BY COUNTRY, 2019–2023 (USD MILLION)

TABLE 120 ASIA PACIFIC: MARKET, BY COUNTRY, 2024–2029 (USD MILLION)

TABLE 121 CHINA: CLOUD SERVICES BROKERAGE MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 122 CHINA: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 123 CHINA: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 124 CHINA: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 125 JAPAN: MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 126 JAPAN: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 127 JAPAN: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 128 JAPAN: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 129 INDIA: CLOUD SERVICES BROKERAGE MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 130 INDIA: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 131 INDIA: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 132 INDIA: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 133 REST OF ASIA PACIFIC: MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 134 REST OF ASIA PACIFIC: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 135 REST OF ASIA PACIFIC: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 136 REST OF ASIA PACIFIC: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 137 MIDDLE EAST & AFRICA: MARKET, BY SERVICE TYPE, 2019–2023 (USD MILLION)

TABLE 138 MIDDLE EAST & AFRICA: MARKET, BY SERVICE TYPE, 2024–2029 (USD MILLION)

TABLE 139 MIDDLE EAST & AFRICA: MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 140 MIDDLE EAST & AFRICA: CLOUD SERVICES BROKERAGE MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 141 MIDDLE EAST & AFRICA: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 142 MIDDLE EAST & AFRICA: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 143 MIDDLE EAST & AFRICA: MARKET, BY VERTICAL, 2019–2023 (USD MILLION)

TABLE 144 MIDDLE EAST & AFRICA: MARKET, BY VERTICAL, 2024–2029 (USD MILLION)

TABLE 145 MIDDLE EAST & AFRICA: MARKET, BY COUNTRY/SUBREGION, 2019–2023 (USD MILLION)

TABLE 146 MIDDLE EAST & AFRICA: MARKET, BY COUNTRY/SUBREGION, 2024–2029 (USD MILLION)

TABLE 147 GULF CORPORATION COUNCIL COUNTRIES: CLOUD SERVICES BROKERAGE MARKET, BY COUNTRY, 2019–2023 (USD MILLION)

TABLE 148 GULF CORPORATION COUNCIL COUNTRIES: MARKET, BY COUNTRY, 2024–2029 (USD MILLION)

TABLE 149 GULF COOPERATION COUNCIL COUNTRIES: MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 150 GULF COOPERATION COUNCIL COUNTRIES: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 151 GULF COOPERATION COUNCIL COUNTRIES: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 152 GULF COOPERATION COUNCIL COUNTRIES: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 153 SOUTH AFRICA: CLOUD SERVICES BROKERAGE MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 154 SOUTH AFRICA: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 155 SOUTH AFRICA: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 156 SOUTH AFRICA: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 157 REST OF MIDDLE EAST & AFRICA: MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 158 REST OF MIDDLE EAST & AFRICA: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 159 REST OF MIDDLE EAST & AFRICA: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 160 REST OF MIDDLE EAST & AFRICA: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 161 LATIN AMERICA: MARKET, BY SERVICE TYPE, 2019–2023 (USD MILLION)

TABLE 162 LATIN AMERICA: MARKET, BY SERVICE TYPE, 2024–2029 (USD MILLION)

TABLE 163 LATIN AMERICA: MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 164 LATIN AMERICA: CLOUD SERVICES BROKERAGE MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 165 LATIN AMERICA: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 166 LATIN AMERICA: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 167 LATIN AMERICA: MARKET, BY VERTICAL, 2019–2023 (USD MILLION)

TABLE 168 LATIN AMERICA: MARKET, BY VERTICAL, 2024–2029 (USD MILLION)

TABLE 169 LATIN AMERICA: MARKET, BY COUNTRY, 2019–2023 (USD MILLION)

TABLE 170 LATIN AMERICA: MARKET, BY COUNTRY, 2024–2029 (USD MILLION)

TABLE 171 BRAZIL: MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 172 BRAZIL: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 173 BRAZIL: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 174 BRAZIL: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 175 MEXICO: MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 176 MEXICO: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 177 MEXICO: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 178 MEXICO: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 179 REST OF LATIN AMERICA: CLOUD SERVICES BROKERAGE MARKET, BY CLOUD SERVICE MODEL, 2019–2023 (USD MILLION)

TABLE 180 REST OF LATIN AMERICA: MARKET, BY CLOUD SERVICE MODEL, 2024–2029 (USD MILLION)

TABLE 181 REST OF LATIN AMERICA: MARKET, BY ORGANIZATION SIZE, 2019–2023 (USD MILLION)

TABLE 182 REST OF LATIN AMERICA: MARKET, BY ORGANIZATION SIZE, 2024–2029 (USD MILLION)

TABLE 183 OVERVIEW OF STRATEGIES BY KEY CLOUD SERVICES BROKERAGE VENDORS

TABLE 184 MARKET: DEGREE OF COMPETITION

TABLE 185 SERVICE TYPE FOOTPRINT

TABLE 186 ORGANIZATION SIZE FOOTPRINT

TABLE 187 VERTICAL FOOTPRINT

TABLE 188 REGIONAL FOOTPRINT

TABLE 189 MARKET: KEY START-UPS/SMES

TABLE 190 CLOUD SERVICES BROKERAGE MARKET: COMPETITIVE BENCHMARKING OF KEY START-UPS/SMES

TABLE 191 MARKET: PRODUCT LAUNCHES AND ENHANCEMENTS, NOVEMBER 2022 – APRIL 2024

TABLE 192 MARKET: DEALS, OCTOBER 2022–SEPTEMBER 2024

TABLE 193 ACCENTURE: COMPANY OVERVIEW

TABLE 194 ACCENTURE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 195 ACCENTURE: PRODUCT LAUNCHES

TABLE 196 ACCENTURE: DEALS

TABLE 197 IBM: COMPANY OVERVIEW

TABLE 198 IBM: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 199 IBM: PRODUCT ENHANCEMENTS

TABLE 200 IBM: DEALS

TABLE 201 BROADCOM: COMPANY OVERVIEW

TABLE 202 BROADCOM: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 203 BROADCOM: PRODUCT LAUNCHES

TABLE 204 BROADCOM: DEALS

TABLE 205 ARROW ELECTRONICS: COMPANY OVERVIEW

TABLE 206 ARROW ELECTRONICS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 207 ARROW ELECTRONICS: PRODUCT LAUNCHES AND ENHANCEMENTS

TABLE 208 ARROW ELECTRONICS: DEALS

TABLE 209 FUJITSU: COMPANY OVERVIEW

TABLE 210 FUJITSU: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 211 FUJITSU: PRODUCT LAUNCHES

TABLE 212 FUJITSU: DEALS

TABLE 213 DXC TECHNOLOGY: COMPANY OVERVIEW

TABLE 214 DXC TECHNOLOGY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 215 DXC TECHNOLOGY: PRODUCT LAUNCHES

TABLE 216 DXC TECHNOLOGY: DEALS

TABLE 217 WIPRO: COMPANY OVERVIEW

TABLE 218 WIPRO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 219 WIPRO: DEALS

TABLE 220 EVIDEN: COMPANY OVERVIEW

TABLE 221 EVIDEN: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 222 EVIDEN: PRODUCT LAUNCHES

TABLE 223 EVIDEN: DEALS

TABLE 224 AWS: COMPANY OVERVIEW

TABLE 225 AWS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 226 INFOSYS: COMPANY OVERVIEW

TABLE 227 INFOSYS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 228 INFOSYS: DEALS

TABLE 229 CLOUD COMPUTING MARKET, BY SERVICE MODEL, 2018–2022 (USD BILLION)

TABLE 230 CLOUD COMPUTING MARKET, BY SERVICE MODEL, 2023–2028 (USD BILLION)

TABLE 231 CLOUD COMPUTING MARKET, BY DEPLOYMENT MODEL, 2018–2022 (USD BILLION)

TABLE 232 CLOUD COMPUTING MARKET, BY DEPLOYMENT MODEL, 2023–2028 (USD BILLION)

TABLE 233 CLOUD COMPUTING MARKET, BY ORGANIZATION SIZE, 2018–2022 (USD BILLION)

TABLE 234 CLOUD COMPUTING MARKET, BY ORGANIZATION SIZE, 2023–2028 (USD BILLION)

TABLE 235 CLOUD COMPUTING MARKET, BY VERTICAL, 2018–2022 (USD BILLION)

TABLE 236 CLOUD COMPUTING MARKET, BY VERTICAL, 2023–2028 (USD BILLION)

TABLE 237 CLOUD COMPUTING MARKET, BY REGION, 2018–2022 (USD BILLION)

TABLE 238 CLOUD COMPUTING MARKET, BY REGION, 2023–2028 (USD BILLION)

TABLE 239 MULTI-CLOUD MANAGEMENT MARKET, BY PLATFORM, 2015–2022 (USD MILLION)

TABLE 240 MULTI-CLOUD MANAGEMENT MARKET, BY APPLICATION, 2015–2022 (USD MILLION)

TABLE 241 MULTI-CLOUD MANAGEMENT MARKET, BY SERVICE TYPE, 2015–2022 (USD MILLION)

TABLE 242 MULTI-CLOUD MANAGEMENT MARKET, BY DEPLOYMENT MODEL, 2015–2022 (USD MILLION)

TABLE 243 MULTI-CLOUD MANAGEMENT MARKET, BY VERTICAL, 2015–2022 (USD MILLION)

TABLE 244 MULTI-CLOUD MANAGEMENT MARKET, BY REGION, 2015–2022 (USD MILLION)

LIST OF FIGURES (51 FIGURES)

FIGURE 1 MARKET: RESEARCH DESIGN

FIGURE 2 BREAKUP OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

FIGURE 3 DATA TRIANGULATION

FIGURE 4 CLOUD SERVICES BROKERAGE MARKET: TOP-DOWN AND BOTTOM-UP APPROACHES

FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: SUPPLY-SIDE ANALYSIS

FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY - BOTTOM-UP APPROACH (SUPPLY SIDE): COLLECTIVE REVENUE OF CLOUD SERVICES BROKERAGE VENDORS

FIGURE 7 DEMAND-SIDE APPROACH: MARKET

FIGURE 8 NORTH AMERICA TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

FIGURE 9 FASTEST-GROWING SEGMENTS OF MARKET

FIGURE 10 SHIFT TOWARD CLOUD-BASED SERVICES AND GROWING DEMAND FOR MULTI-CLOUD MANAGEMENT TO DRIVE MARKET

FIGURE 11 AGGREGATION SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

FIGURE 12 SOFTWARE AS A SERVICE SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

FIGURE 13 LARGE ENTERPRISES SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

FIGURE 14 BFSI SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

FIGURE 15 ASIA PACIFIC TO EMERGE AS BEST MARKET FOR INVESTMENT IN NEXT FIVE YEARS

FIGURE 16 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES: CLOUD SERVICES BROKERAGE MARKET

FIGURE 17 CLOUD SERVICES BROKERAGE MARKET: TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

FIGURE 18 AVERAGE SELLING PRICES OF KEY PLAYERS FOR TOP THREE SERVICE TYPES

FIGURE 19 CLOUD SERVICES BROKERAGE MARKET: SUPPLY CHAIN ANALYSIS

FIGURE 20 KEY PLAYERS IN MARKET ECOSYSTEM

FIGURE 21 LIST OF MAJOR PATENTS FOR MARKET

FIGURE 22 CLOUD SERVICES BROKERAGE MARKET: PORTER’S FIVE FORCES ANALYSIS

FIGURE 23 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE VERTICALS

FIGURE 24 KEY BUYING CRITERIA FOR TOP THREE VERTICALS

FIGURE 25 INVESTMENT AND FUNDING SCENARIO OF MAJOR CLOUD SERVICES BROKERAGE COMPANIES

FIGURE 26 IMPACT OF AI/GEN AI IN CLOUD SERVICES BROKERAGE MARKET

FIGURE 27 AGGREGATION SEGMENT TO HOLD LARGEST MARKET DURING FORECAST PERIOD

FIGURE 28 SOFTWARE AS A SERVICE SEGMENT TO HOLD LARGEST MARKET DURING FORECAST PERIOD

FIGURE 29 LARGE ENTERPRISES SEGMENT TO HOLD LARGEST MARKET DURING FORECAST PERIOD

FIGURE 30 BANKING, FINANCIAL SERVICES, AND INSURANCE VERTICAL TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 31 NORTH AMERICA TO HOLD LARGEST MARKET DURING FORECAST

FIGURE 32 NORTH AMERICA: MARKET SNAPSHOT

FIGURE 33 ASIA PACIFIC: MARKET SNAPSHOT

FIGURE 34 REVENUE ANALYSIS OF KEY CLOUD SERVICES BROKERAGE COMPANIES

FIGURE 35 MARKET SHARE ANALYSIS, 2023

FIGURE 36 CLOUD SERVICES BROKERAGE MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

FIGURE 37 COMPANY FOOTPRINT

FIGURE 38 CLOUD SERVICES BROKERAGE MARKET: COMPANY EVALUATION MATRIX (START-UPS/SMES), 2023

FIGURE 39 COMPANY VALUATION OF KEY PLAYERS

FIGURE 40 FINANCIAL METRICS

FIGURE 41 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY VENDORS

FIGURE 42 BRAND/PRODUCT COMPARISON

FIGURE 43 ACCENTURE: COMPANY SNAPSHOT

FIGURE 44 IBM: COMPANY SNAPSHOT

FIGURE 45 BROADCOM: COMPANY SNAPSHOT

FIGURE 46 ARROW ELECTRONICS: COMPANY SNAPSHOT

FIGURE 47 FUJITSU: COMPANY SNAPSHOT

FIGURE 48 DXC TECHNOLOGY: COMPANY SNAPSHOT

FIGURE 49 WIPRO: COMPANY SNAPSHOT

FIGURE 50 AWS: COMPANY SNAPSHOT

FIGURE 51 INFOSYS: COMPANY SNAPSHOT

Growth opportunities and latent adjacency in Cloud Services Brokerage Market