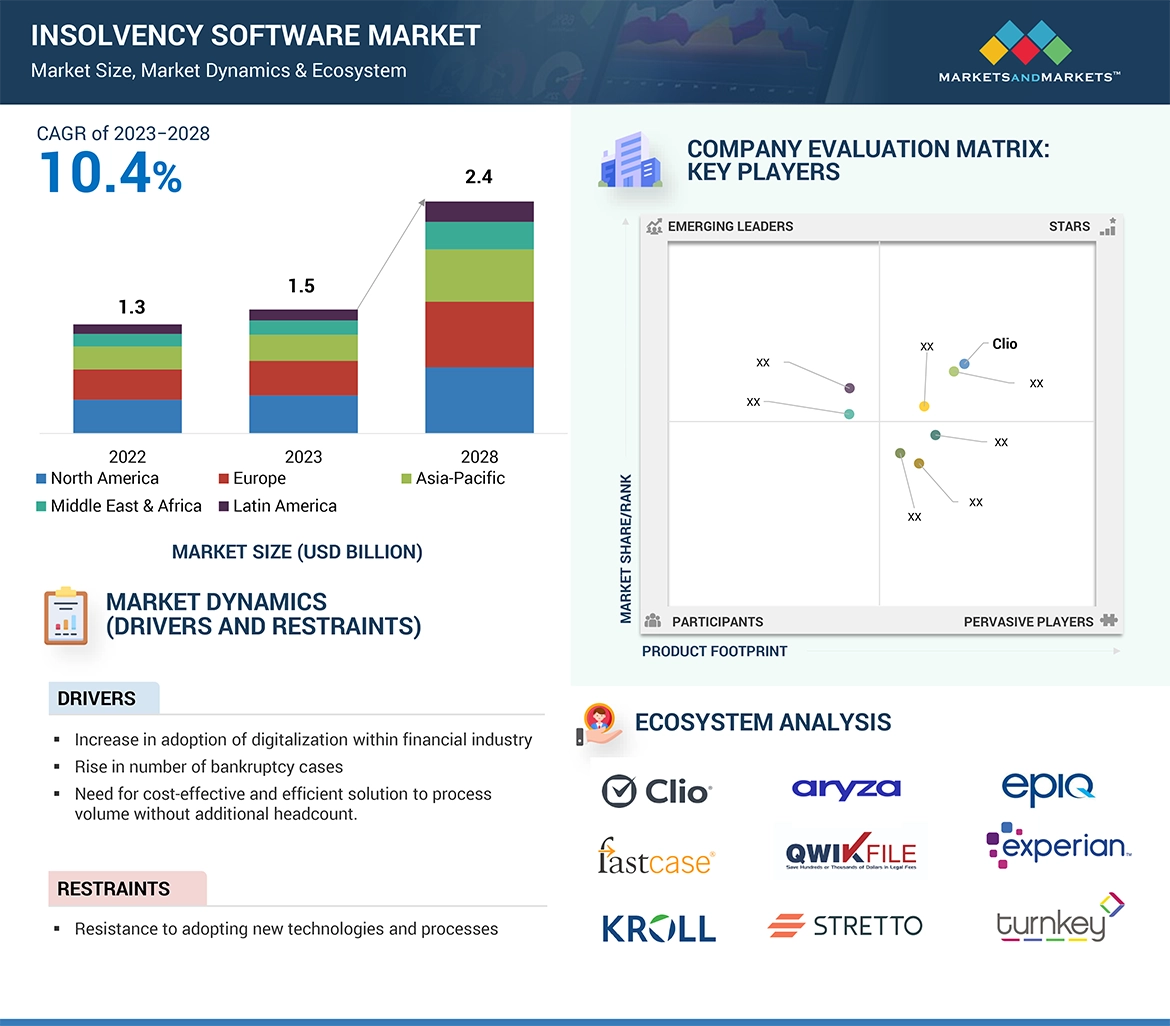

5.2 MARKET DYNAMICS

DRIVERS

- Increase in adoption of digitalization within financial industry

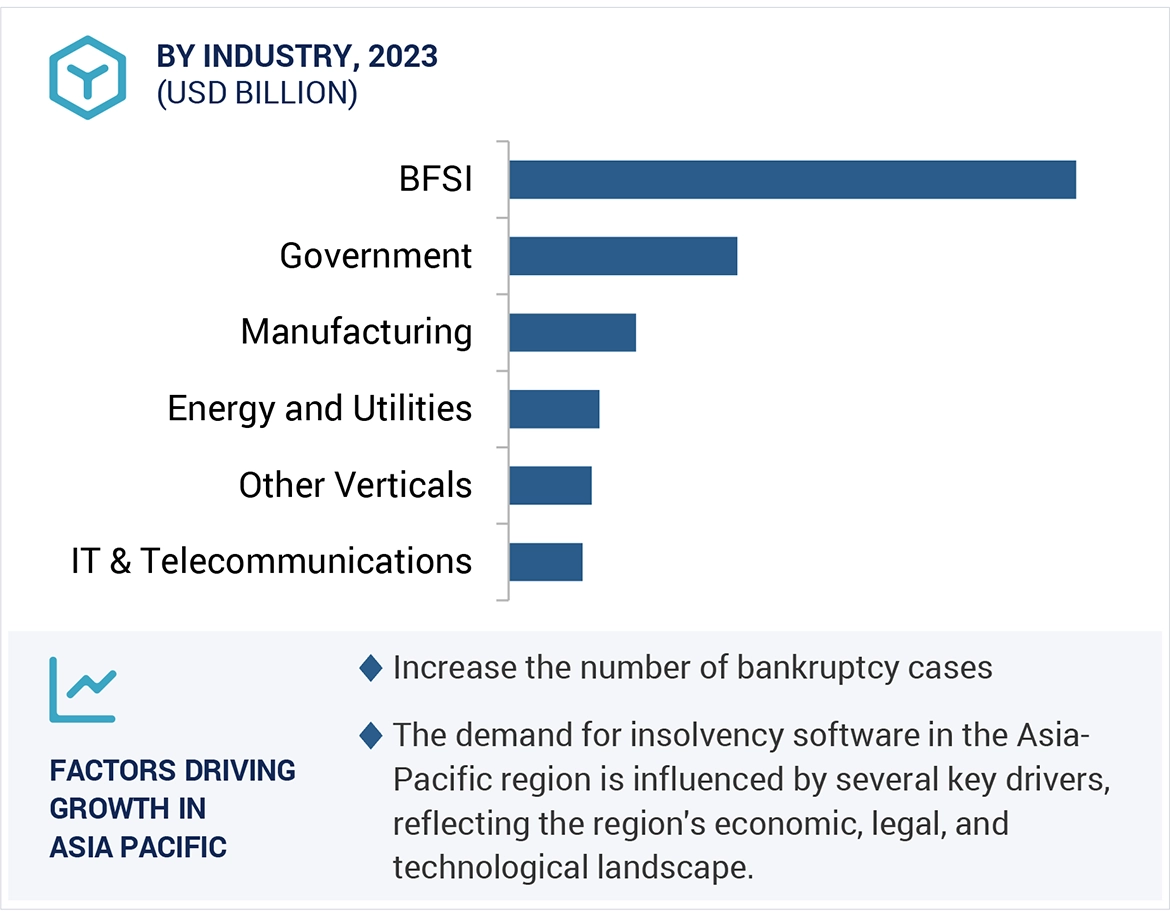

- Rise in number of bankruptcy cases

- Need for cost-effective and efficient solution to process volume without additional headcount

- Growth in demand for automated tools to make well-informed decisions

RESTRAINTS

- Resistance to shift away from legacy systems

OPPORTUNITIES

- Ongoing trend for digitalization in IT industry

- Increase in automation to boost adoption of emerging technology

- Rise in demand for software automation and innovative applications

CHALLENGES

- Lack of data privacy and safety

- Maintaining compliance in changing regulatory landscape

- Need for third-party providers to enable and manage technology and hosting aspects

5.3 INDUSTRY TRENDS

BRIEF HISTORY OF INSOLVENCY SOFTWARE MARKET

- Early software solutions and transition to Windows-based software

- Integration of legal research

- Automation and workflow management

- Cloud-based advanced analytics solutions

- Data privacy and safety concerns

- Enhancement in software with new emerging technologies

BEST PRACTICES IN INSOLVENCY SOFTWARE MARKET

VALUE CHAIN ANALYSIS

ECOSYSTEM MAPPING

PATENT ANALYSIS

- Methodology

- Document type

- Innovation and patent applications

USE CASES

- Aryza Dunning improved Louwman Dealer Group’s debt management system

- Stretto helped Crosby & Fox better its communication systems

- Stretto offered Richard West Law Office its Best Case solution for efficient case-filing

- Stretto’s solutions streamlined Nelson Law Office’s functionalities

PRICING ANALYSIS

- Average selling price trend of key players, by offering

- Indicative pricing analysis of key players, By Solution

TYPE OF CHAPTERS IN INSOLVENCY SOFTWARE

- Chapter 7

- Chapter 11

- Chapter 12

- Chapter 13

- Chapter 15

INSOLVENCY SOFTWARE MARKET: COUNTRY-LEVEL OUTLOOK

- India

- US

- Canada

- European Countries

TECHNOLOGY ANALYSIS

- Adjacent technologies

PORTER’S FIVE FORCES ANALYSIS

- Threat of new entrants

- Threat of substitutes

- Bargaining power of buyers

- Bargaining power of suppliers

- Intensity of competitive rivalry

DISRUPTIONS IMPACTING BUYERS/CUSTOMERS IN INSOLVENCY SOFTWARE MARKET

REGULATORY LANDSCAPE

- International Organization for Standardization 27001

- Basel Committee on Banking Supervision

- DODD-FRANK Act

- Health Insurance Portability and Accountability Act

- General Data Protection Regulation

- Markets in Financial Instruments Directive

- Financial Industry Information Systems

KEY CONFERENCES & EVENTS

KEY STAKEHOLDERS & BUYING CRITERIA

- Key stakeholders in buying process

- Buying criteria

FUTURE DIRECTION OF INSOLVENCY SOFTWARE MARKET

- Insolvency software roadmap till 2030

- Short-term roadmap (2023–2025)

- Mid-term roadmap (2026–2028)

- Long-term roadmap (2029–2030)

Growth opportunities and latent adjacency in Insolvency Software Market