Tactical Optics Market by Product (Weapon Scopes & Sights, Handheld Sighting Devices, Cameras & Displays), Platform, Application (ISR, Target Acquisition & Identification, Border & Coastal Patrol), End Use, Range, and Region - Global Forecast to 2025

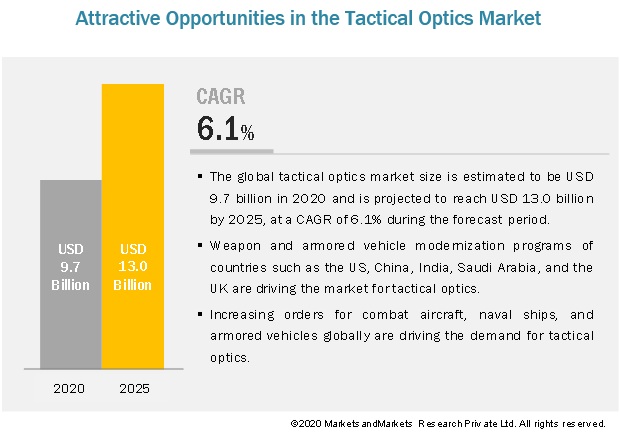

[251 Pages Report] The global Tactical Optics Market size is projected to grow from USD 9.7 Billion in 2020 to USD 13.0 Billion by 2025, at a CAGR of 6.1% from 2020 to 2025. Some of the factors expected to fuel the demand for Tactical Optics Industry include the increased procurement of military equipment, modernization programs by militaries globally, and the need for remote weapon stations and turrets for armored vehicles and naval ships.

The market includes major Tier 1 players, such as Kongsberg Gruppen AS (Norway), Raytheon Company (US), Elbit Systems Ltd. (Israel), Saab AB (Sweden), and BAE Systems plc (UK). These companies offer advanced electro-optic cameras and thermal cameras, which make up the majority of the tactical optics market share. The tactical optics industry also constitutes Tier 2 and Tier 3 players who offer tactical optics for dismounted soldiers, which cost comparatively lesser. These players include Sig Sauer, Inc. (US), Vortex Optics (US), Bushnell Corporation (US), and Leupold & Stevens, Inc. (US).

The airborne segment is projected to register the highest CAGR during the forecast period.

Based on platform, the tactical optics market has been segmented into airborne, naval, and land. The airborne segment is projected to witness the highest CAGR from 2020 to 2025. Several countries are ordering new generation and advanced fighter aircraft, attack helicopters, and unmanned aerial vehicles. Countries such as the US, Canada, France, India, China, and Russia have invested substantially in developing a strong air force with modern aircraft, which is subsequently driving the market for tactical optics.

The target acquisition & identification application segment is expected to lead the tactical optics from 2020 to 2025.

Based on application, the market has been segmented into target acquisition & identification; search & rescue; intelligence, surveillance, & reconnaissance; and border & coastal patrol. The target acquisition & identification segment is projected to lead the tactical optics market during the forecast period due to the increased procurement of armored vehicles & aircraft and modernization of naval fleets, globally.

The long-range (>25 km) segment is projected to register the highest CAGR from 2020 to 2025.

Based on range, the tactical optics market has been segmented into short-range (< 3 km), medium-range (3–25 km), and long-range (> 25 km). The long-range (> 25 km) segment is projected to lead the market during the forecast period. Growth in this segment can be attributed to the strong demand for electro-optic/infrared cameras, day cameras, and thermal cameras, among other tactical optics. Additionally, there is an increasing demand for remote weapon stations for armored vehicles and naval ships.

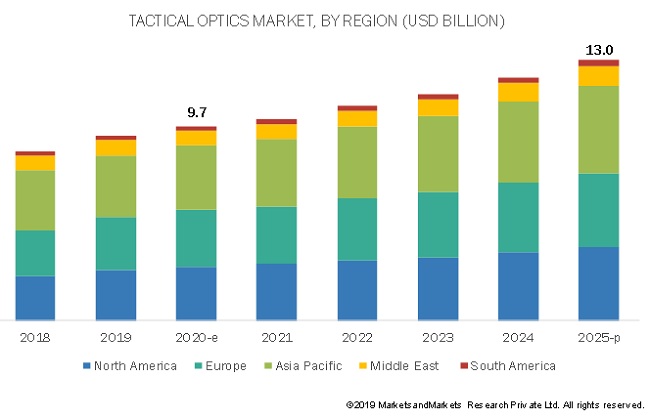

Asia Pacific is projected to lead the tactical optics market from 2020 to 2025.

By region, Asia Pacific is estimated to account for the largest market share during the forecast period due to the increased demand for tactical optics for ground, naval, and airborne platforms in the region.

Tactical Optics Industry Companies: Top Key Market Players

The Tactical Optics Companies are dominated by globally established players such as Kongsberg Gruppen AS (Norway), Raytheon Company (US), Elbit Systems Ltd. (Israel), Saab AB (Sweden), Thales Group (France), and BAE Systems plc (UK). These companies offer advanced electro-optic cameras and thermal cameras, which make up the majority of the tactical optics market. The market also constitutes Tier 2 and Tier 3 players who offer tactical optics for dismounted soldiers, which cost comparatively lesser. These players include Sig Sauer, Inc. (US), Vortex Optics (US), Bushnell Corporation (US), and Leupold & Stevens, Inc. (US).

Scope of the Report

|

Report Metric |

Details |

|

Estimated Market Size |

USD 9.7 Billion in 2020 |

|

Projected Market Size |

USD 13.0 Billion by 2025 |

|

Growth Rate |

CAGR 6.1% |

|

Market Size Available for Years |

2018–2025 |

|

Base Year Considered |

2020 |

|

Forecast Period |

2020–2025 |

|

Forecast Monetary Unit |

Value (USD) |

|

Segments Covered |

Product, Platform, Application, End Use, Range, and Region |

|

Regions Covered |

North America, Europe, Asia Pacific, Middle East, and South America |

|

Companies Covered |

Leonardo S.p.A. (Italy), BAE Systems plc (UK) Kongsberg Gruppen AS (Norway), Raytheon Company (US), Saab AB (Sweden), Sig Sauer, Inc. (US), Bushnell Corporation (US), and Leupold & Stevens, Inc. (US), among others |

This research report categorizes the tactical optics market based on product, platform, application, end use, range, and region.

Based on Product:

-

Weapon Scopes & Sights

-

Riflescopes

- Day Sights

- Night Sights

- Digital Sights

-

Night Vision Scopes

- Thermal Scopes

- Infrared Scopes

- Image Intensifiers

- Electro-Optic/Infrared (EO/IR) Sights

-

Riflescopes

-

Handheld Sighting Devices

-

Binoculars & monoculars

- Day Sights

- Night Sights

- Night Vision Goggles

- Spotter Scopes

- Rangefinders

- Target Acquisition & Surveillance Systems

-

Binoculars & monoculars

-

Cameras & Displays

- Head-mounted Displays (HMDs)

- Thermal Cameras

- Electro-Optic/Infrared (EO/IR) Cameras

Based on Platform:

-

Ground

-

Vehicle Mounted

- Main Battle Tanks (MBTs)

- Infantry Fighting Vehicles (IFVs)

- Armored Personnel Carriers (APCs)

- Armored Amphibious Vehicles (AAVs)

- Light Protected Vehicles (LPVs)

- Self-propelled Howitzers (SPHs)

- Armored Mortar Carriers (AMCs)

- Unmanned Ground Vehicles (UGVs)

- Fixed Installation

-

Portable

- Man-portable

- Dismounted Soldier

-

Vehicle Mounted

-

Naval

- Aircraft Carriers

- Destroyers

- Frigates

- Corvettes

- Offshore Patrol Vessels (OPVs)

- Unmanned Marine Vessels (UMVs)

-

Airborne

- Combat Aircraft

- Combat Helicopters

- Special Mission Aircraft

- Unmanned Aerial Vehicles (UAVs)

Based on Application:

- Intelligence, Surveillance, & Reconnaissance (ISR)

- Target Acquisition & Identification

- Search & Rescue

- Border & Coastal Patrol

Based on End Use:

- Manned Platform

- Weapon Mounted

- Soldier

- Unmanned Platform

Based on Range:

- Short-range (< 3 km)

- Medium-range (3–25 km)

- Long-range (> 25 km)

Based on Region:

- North America

- Europe

- Asia Pacific

- Middle East

- South America

Recent Developments

- In March 2020, Elbit Systems announced that one of its subsidiaries in Europe was awarded a contract from an unnamed European country for the supply of multiple advanced Electro-Optic systems for individual infantry soldiers. The USD 35 million contract will be performed over two years.

- In December 2019, Kongsberg Defence & Aerospace AS, a subsidiary of Kongsberg Gruppen AS, secured a contract worth USD 31 million from the Danish Ministry of Defence Acquisition and Logistics Organisation (DALO) for the delivery of the KONGSBERG PROTECTOR Remote Weapon Station (RWS) to the Danish Army.

- In February 2019, Thales Deutschland, a subsidiary of Thales Group, secured a contract worth USD 67 million from the German Defense Procurement Agency for the supply of 12 Mirador Mk2 Electro-optical systems

- In December 2018, Raytheon Company secured a contract worth USD 40 million from the US Navy for the repair of the multi-spectral targeting systems of the H-60 aircraft.

Key Questions Addressed by the Report

- What is the growth prospect of the tactical optics? What are the key dynamics, such as drivers and opportunities, governing the market?

- What are the key sustainability strategies adopted by leading players operating in the tactical optics market?

- What are the new emerging technologies and use cases disrupting the tactical optics market?

- What are the applications, wherein tactical optics play a significant role?

- What are the key trends and opportunities in the tactical optics across different regions and their respective countries?

- Who are the key players and innovators in the ecosystem of tactical optics?

- How is the competitive landscape changing in the client ecosystem, and how is it impacting the revenue of companies?

To speak to our analyst for a discussion on the above findings, click Speak to Analyst

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TABLE OF CONTENTS

1 INTRODUCTION (Page No. - 26)

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.2.1 MARKETS COVERED

1.2.2 REGIONAL SCOPE

1.2.3 YEARS CONSIDERED FOR THE STUDY

1.3 CURRENCY & PRICING

1.4 USD EXCHANGE RATES

1.5 LIMITATIONS

1.6 MARKET STAKEHOLDERS

2 RESEARCH METHODOLOGY (Page No. - 30)

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.2 MARKET DEFINITION & SCOPE

2.2.1 PRIMARY DATA

2.2.1.1 Key data from primary sources

2.2.1.2 Breakdown of primaries

2.2.2 SEGMENT DEFINITIONS

2.2.2.1 Tactical optics market, by product

2.2.2.2 Tactical optics market, by platform

2.2.2.3 Tactical optics market, by application

2.2.2.4 Tactical optics market, by end use

2.2.2.5 Tactical optics market, by range

2.2.3 EXCLUSIONS

2.3 MARKET SIZE ESTIMATION & METHODOLOGY

2.3.1 TOP-DOWN APPROACH

2.4 DATA TRIANGULATION

2.4.1 MARKET SIZING & FORECASTING

2.5 ASSUMPTIONS OF THE RESEARCH STUDY

2.6 LIMITATIONS

2.7 LIST PRICE FOR TACTICAL OPTICS

3 EXECUTIVE SUMMARY (Page No. - 45)

4 PREMIUM INSIGHTS (Page No. - 49)

4.1 ATTRACTIVE OPPORTUNITIES IN TACTICAL OPTICS MARKET

4.2 GROUND TACTICAL OPTICS MARKET, BY VEHICLE TYPE

4.3 NAVAL TACTICAL OPTICS MARKET, BY VESSEL TYPE

4.4 AIRBORNE TACTICAL OPTICS MARKET, BY AIRCRAFT TYPE

4.5 WEAPON SCOPES & SIGHTS MARKET, BY TYPE

4.6 HANDHELD DEVICES MARKET, BY TYPE

4.7 CAMERAS & DISPLAYS MARKET, BY TYPE

4.8 TACTICAL OPTICS MARKET, BY REGION

5 MARKET OVERVIEW (Page No. - 53)

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Increase in procurement of tactical optics for dismounted soldiers and vehicle platforms

5.2.1.2 Increasing demand for EO/IR cameras

5.2.2 OPPORTUNITIES

5.2.2.1 Weapon modernization plans across the world

5.2.3 CHALLENGES

5.2.3.1 Requirement for high technical expertise to develop tactical optics

6 INDUSTRY TRENDS (Page No. - 57)

6.1 INTRODUCTION

6.2 EMERGING TRENDS

6.2.1 ECHO3 ELECTRO-OPTICS THERMAL REFLEX SIGHT

6.2.2 FREEFORM OPTICS

6.2.3 INTELLIGENT HARDWARE SOLUTIONS

6.2.4 INTELLIGENT ENTERPRISE: COMMAND AND CONTROL ABOVE THE WEAPONS SYSTEMS

6.2.5 ADVANCEMENTS IN CAMERA TECHNOLOGY

6.2.6 ADVANCED BALLISTIC CALCULATORS

6.2.7 MINIATURIZED ELECTRO-OPTICS

6.2.8 NIGHT VISION RIFLESCOPES

6.2.9 FIBER LASER TECHNOLOGY

6.2.10 ARMORED VEHICLES WITH ADVANCED TACTICAL OPTICS FOR URBAN WARFARE

6.2.11 WEAPONIZED DRONES WITH TACTICAL OPTICS

6.3 ADVANCED TECHNOLOGIES DEVELOPED BY COMPANIES IN THE TACTICAL OPTICS MARKET

6.3.1 ADVANCED SIGHTING SYSTEM

6.3.2 ENHANCED NIGHT VISION GOGGLE (ENVG) WITH FAMILY OF WEAPON SIGHTS (FWS)

6.3.3 MICROSOFT HOLOLENS AUGMENTED REALITY HEADSET

6.3.4 HYPERCENTRIC OPTICS

6.4 INNOVATIONS & PATENT REGISTRATIONS

7 TACTICAL OPTICS MARKET, BY PRODUCT (Page No. - 64)

7.1 INTRODUCTION

7.2 WEAPON SCOPES & SIGHTS

7.2.1 RIFLESCOPES

7.2.1.1 Day Sights

7.2.1.1.1 Development of micro electro-optic systems

7.2.1.2 Night Sights

7.2.1.2.1 Increasing adoption of thermal imaging technology during low visibility/night

7.2.1.3 Digital Sights

7.2.1.3.1 Increase in disruptive technologies leading to the linkage of numerous tactical optics together to create maximum awareness on the battlefield

7.2.2 NIGHT VISION SCOPES

7.2.2.1 Thermal scopes

7.2.2.1.1 Thermal imaging technology for target detection capabilities is driving the market

7.2.2.2 Infrared scopes

7.2.2.2.1 Infrared technology assists soldiers in low light

7.2.2.3 Image intensifiers

7.2.2.3.1 Increasing investments in the defense sector boost the market for image intensifiers

7.2.3 HANDHELD SIGHTING DEVICES

7.2.3.1 Binoculars & monoculars

7.2.3.1.1 New optical technologies, such as digital zoom, thermal binoculars, and night vision binoculars, are driving the market

7.2.3.2 Night vision goggles

7.2.3.2.1 Increased adoption of head-mounted night vision goggles

7.2.3.3 Spotter scopes

7.2.3.3.1 Growing number of snipers leading to increased demand for spotter scopes

7.2.3.4 Rangefinders

7.2.3.4.1 Demand for enhanced situational awareness leading to growth in demand for rangefinders

7.2.3.5 Target acquisition & surveillance systems

7.2.3.5.1 increased use of target acquisition & surveillance systems by militaries worldwide

7.2.4 CAMERAS & DISPLAYS

7.2.4.1 Head-mounted displays (HMDs)

7.2.4.1.1 Rapid development in HMD technology for infantry soldiers

7.2.4.2 Thermal cameras

7.2.4.2.1 Increasing use of thermal cameras for border surveillance

7.2.4.3 EO/IR cameras

7.2.4.3.1 Increased use of drones with EO/IR is driving the tactical optics market

8 TACTICAL OPTICS MARKET, BY PLATFORM (Page No. - 75)

8.1 INTRODUCTION

8.2 GROUND

8.2.1 VEHICLE-MOUNTED

8.2.1.1 Increased procurement of armored vehicles by various militaries globally

8.2.1.1.1 Main battle tanks (MBTs)

8.2.1.1.2 Infantry fighting vehicles (IFVs)

8.2.1.1.3 Armored personnel carriers (APCs)

8.2.1.1.4 Armored amphibious vehicles (AAVs)

8.2.1.1.5 Light protected vehicles (LPVs)

8.2.1.1.6 Self-propelled howitzers (SPHs)

8.2.1.1.7 Armored mortar carriers (AMCs)

8.2.1.1.8 Unmanned ground vehicles (UGVs)

8.2.2 FIXED INSTALLATION

8.2.2.1 Increasing installation of high-tech cameras, sights, and ground-based interceptors with tactical optics for border surveillance and protection

8.2.3 PORTABLE

8.2.3.1 Portable military equipment comprises high-tech tactical optics used to cater to the military modernization requirements

8.2.3.2 Man-portable

8.2.3.2.1 Increasing demand for riflescopes, binoculars, and target designators is driving the market

8.2.3.3 Dismounted soldier

8.2.3.3.1 Upgrades to soldier equipment drive the market for tactical optics devices with respect to dismounted soldier

8.3 NAVAL

8.3.1 AIRCRAFT CARRIERS

8.3.1.1 Upgrades and modernization programs of aircraft carriers undertaken by various countries

8.3.2 DESTROYERS

8.3.2.1 Installation of new weapons systems on destroyers

8.3.3 FRIGATES

8.3.3.1 Increased orders for frigates by several countries such, as India, Russia, and Germany

8.3.4 CORVETTES

8.3.4.1 Ongoing upgrades of corvettes by various countries, such as India, Israel, and Finland

8.3.5 OFFSHORE PATROL VESSELS (OPVS)

8.3.5.1 Modernization programs of OPVs drive the market

8.3.6 UNMANNED MARINE VESSELS (UMVS)

8.3.6.1 Increased use of UMVs for surveillance

8.4 AIRBORNE

8.4.1 COMBAT AIRCRAFT

8.4.1.1 Upgrades and modernization programs of combat aircraft by various leading market players

8.4.2 ATTACK HELICOPTERS

8.4.2.1 Increased procurement of attack helicopters by India and South Korea, among others, drives the market

8.4.3 SPECIAL MISSION AIRCRAFT

8.4.3.1 Ongoing procurement of special mission aircraft by countries such as Finland and Bulgaria, among others, drives the market

8.4.4 UNMANNED AERIAL VEHICLES (UAVS)

8.4.4.1 Continuous development programs to utilize tactical UAVs by defense forces

9 TACTICAL OPTICS MARKET, BY APPLICATION (Page No. - 96)

9.1 INTRODUCTION

9.2 INTELLIGENCE, SURVEILLANCE & RECONNAISSANCE (ISR)

9.2.1 INCREASED NEED FOR ISR CAPABILITIES BY MILITARIES GLOBALLY

9.3 TARGET IDENTIFICATION & ACQUISITION

9.3.1 INSTALLATION OF TARGET IDENTIFICATION & ACQUISITION PRODUCTS ON VARIOUS PLATFORMS INCREASES THE DEMAND FOR TACTICAL OPTICS

9.4 SEARCH & RESCUE

9.4.1 INCREASED USE OF DRONES FOR SEARCH & RESCUE MISSIONS

9.5 BORDER & COASTAL PATROL

9.5.1 INCREASED INSTALLATION OF EO/IR CAMERAS FOR BORDER & COASTAL SURVEILLANCE

10 TACTICAL OPTICS MARKET, BY END USE (Page No. - 102)

10.1 INTRODUCTION

10.2 MANNED PLATFORM

10.2.1 NEED FOR SITUATIONAL AWARENESS DRIVES THE MARKET FOR TACTICAL OPTICS IN THE MANNED PLATFORM SEGMENT

10.3 WEAPON MOUNTED

10.3.1 PROCUREMENT OF NEW WEAPONS IS DRIVING THE WEAPON MOUNTED TACTICAL OPTICS MARKET

10.4 SOLDIER

10.4.1 VARIOUS INFANTRY MODERNIZATION PROGRAMS GLOBALLY DRIVE THE DEMAND FOR TACTICAL OPTICS

10.5 UNMANNED PLATFORM

10.5.1 INCREASING USE OF UNMANNED PLATFORMS FOR SURVEILLANCE AND ASSAULT

11 TACTICAL OPTICS MARKET, BY RANGE (Page No. - 107)

11.1 INTRODUCTION

11.2 SHORT-RANGE (< 3 KM)

11.2.1 NEED FOR HANDHELD TACTICAL OPTICS IS DRIVING THE TACTICAL OPTICS MARKET

11.3 MEDIUM-RANGE (3–25 KM)

11.3.1 INCREASING USE OF DRONES LEADING TO INCREASED DEMAND FOR MEDIUM-RANGE TACTICAL OPTICS

11.4 LONG-RANGE (> 25 KM)

11.4.1 INCREASING PROCUREMENT OF NAVAL SHIPS, AIRCRAFT, AND ARMORED VEHICLES DRIVE THE MARKET FOR LONG-RANGE TACTICAL OPTICS

12 REGIONAL ANALYSIS (Page No. - 112)

12.1 INTRODUCTION

12.2 NORTH AMERICA

12.2.1 US

12.2.1.1 Procurement of new fighter aircraft

12.2.2 CANADA

12.2.2.1 Numerous defense procurement projects for land, sea, and air platforms

12.3 EUROPE

12.3.1 FRANCE

12.3.1.1 Armored vehicle modernization program to impact the market in France

12.3.2 RUSSIA

12.3.2.1 Serial production of T-90 and T-14 Armata tanks, among others

12.3.3 UK

12.3.3.1 Orders for new family of Ajax multi-role armored vehicles in 2018-2019

12.3.4 GERMANY

12.3.4.1 Modernization programs for naval, airborne, and land fleets

12.3.5 ITALY

12.3.5.1 High procurement spending in 2019 is expected to drive the market in Italy

12.3.6 SPAIN

12.3.6.1 Three military modernization programs planned until 2032

12.3.7 POLAND

12.3.7.1 Multi-billion military modernization program by Poland

12.4 ASIA PACIFIC

12.4.1 CHINA

12.4.1.1 Major expansions in navy and air force are driving the market in China

12.4.2 INDIA

12.4.2.1 Five-year modernization plan for its armed forces is driving the market in India

12.4.3 JAPAN

12.4.3.1 Increased funding for the acquisition of new combat aircraft

12.4.4 SOUTH KOREA

12.4.4.1 Estimated multi-billion spending on arms purchase for troops in 2020

12.4.5 AUSTRALIA

12.4.5.1 Procurement of new military platforms from 2020 to 2028

12.5 MIDDLE EAST

12.5.1 SAUDI ARABIA

12.5.1.1 Multi-billion contracts with the US drive the tactical optics market in Saudi Arabia

12.5.2 TURKEY

12.5.2.1 Substantial rise in military spending in 2018

12.5.3 ISRAEL

12.5.3.1 Ongoing procurement of armored vehicles and combat aircraft to drive the market in Israel

12.6 SOUTH AMERICA

12.6.1 BRAZIL

12.6.1.1 Short and medium-term investments to modernize armed forces in Brazil

12.6.2 MEXICO

12.6.2.1 Procurement of armored vehicles and weapons for soldiers

13 COMPETITIVE LANDSCAPE – TIER 1 COMPANIES (Page No. - 175)

13.1 INTRODUCTION

13.2 COMPETITIVE ANALYSIS

13.3 MARKET RANKING ANALYSIS, 2019

13.4 COMPETITIVE LEADERSHIP MAPPING

13.4.1 VISIONARY LEADERS

13.4.2 INNOVATORS

13.4.3 DYNAMIC DIFFERENTIATORS

13.4.4 EMERGING COMPANIES

13.5 STRENGTH OF PRODUCT PORTFOLIO

13.6 BUSINESS STRATEGY EXCELLENCE

13.7 COMPETITIVE SCENARIO

13.7.1 CONTRACTS

13.7.2 NEW PRODUCT DEVELOPMENTS

13.7.3 ACQUISITIONS

14 COMPETITIVE LANDSCAPE – TIER 2 & 3 COMPANIES (Page No. - 182)

14.1 INTRODUCTION

14.2 COMPETITIVE ANALYSIS

14.3 MARKET RANKING ANALYSIS, 2019

14.4 COMPETITIVE LEADERSHIP MAPPING

14.4.1 VISIONARY LEADERS

14.4.2 INNOVATORS

14.4.3 DYNAMIC DIFFERENTIATORS

14.4.4 EMERGING COMPANIES

14.5 STRENGTH OF PRODUCT PORTFOLIO

14.6 BUSINESS STRATEGY EXCELLENCE

14.7 COMPETITIVE SCENARIO

14.7.1 CONTRACTS

14.7.2 NEW PRODUCT LAUNCHES

14.7.3 ACQUISITIONS AND PARTNERSHIPS

15 COMPANY PROFILES (Page No. - 190)

(Business Overview, Products Offered, Recent Developments, SWOT Analysis, MnM View)*

15.1 LEONARDO S.P.A.

15.2 BAE SYSTEMS, PLC

15.3 ELBIT SYSTEMS LTD.

15.4 KONGSBERG GRUPPEN AS

15.5 L3HARRIS TECHNOLOGIES

15.6 LOCKHEED MARTIN CORPORATION

15.7 NORTHROP GRUMMAN CORPORATION

15.8 RAYTHEON COMPANY

15.9 THALES GROUP

15.10 SAAB AB

15.11 RAFAEL ADVANCED DEFENSE SYSTEMS LTD

15.12 FLIR SYSTEMS, INC.

15.13 ISRAEL AEROSPACE INDUSTRIES

15.14 WUHAN JOHO TECHNOLOGY CO. LTD.

15.15 AIMPOINT

15.16 ATN CORPORATION

15.17 BUSHNELL CORPORATION

15.18 BURRIS COMPANY, INC.

15.19 LEUPOLD & STEVENS, INC.

15.20 NIGHTFORCE OPTICS

15.21 SIG SAUER, INC.

15.22 SIGHTMARK

15.23 TRIJICON INC.

15.24 VORTEX OPTICS

*Details on Business Overview, Products Offered, Recent Developments, SWOT Analysis, MnM View might not be captured in case of unlisted companies.

16 APPENDIX (Page No. - 244)

16.1 INDUSTRY EXPERTS

16.2 DISCUSSION GUIDE

16.3 KNOWLEDGE STORE: MARKETSANDMARKETS™ SUBSCRIPTION PORTAL

16.4 AVAILABLE CUSTOMIZATIONS

16.5 RELATED REPORTS

16.6 AUTHOR DETAILS

LIST OF TABLES (186 TABLES)

TABLE 1 MARKET SUMMATION

TABLE 2 SNIPER OPTICS: LIST PRICE USED FOR TACTICAL OPTICS MARKET

TABLE 3 AUTOMATIC RIFLES OPTICS: LIST PRICE USED FOR TACTICAL OPTICS MARKET

TABLE 4 BINOCULARS: LIST PRICE USED FOR TACTICAL OPTICS MARKET

TABLE 5 SPOTTING SCOPES: LIST PRICE USED FOR TACTICAL OPTICS MARKET

TABLE 6 RANGEFINDERS: LIST PRICE USED FOR TACTICAL OPTICS MARKET

TABLE 7 NIGHT VISION GOGGLES: LIST PRICE USED FOR TACTICAL OPTICS MARKET

TABLE 8 MACHINE GUN PROCUREMENT BY MILITARIES WORLDWIDE

TABLE 9 EXPECTED FUTURE REQUIREMENTS OF EO/IR CAMERAS (UNIT), BY COUNTRY

TABLE 10 BOXER ARMORED VEHICLE ARMAMENTS

TABLE 11 TYPES OF WEAPONIZED DRONES

TABLE 12 INNOVATIONS & PATENT REGISTRATIONS, 2009–2017

TABLE 13 TACTICAL OPTICS MARKET SIZE, BY PRODUCT, 2018–2025 (USD MILLION)

TABLE 14 WEAPON SCOPES & SIGHTS TACTICAL OPTICS MARKET SIZE, BY REGION, 2018–2025 (USD MILLION)

TABLE 15 WEAPON SCOPES & SIGHTS TACTICAL OPTICS MARKET SIZE, BY TYPE, 2018–2025 (USD MILLION)

TABLE 16 RIFLESCOPES TACTICAL OPTICS MARKET SIZE, BY TYPE, 2018–2025 (USD MILLION)

TABLE 17 NIGHT VISION SCOPES TACTICAL OPTICS MARKET SIZE, BY TYPE, 2018–2025 (USD MILLION)

TABLE 18 HANDHELD SIGHTING DEVICES TACTICAL OPTICS MARKET SIZE, BY TYPE, 2018–2025 (USD MILLION)

TABLE 19 HANDHELD SIGHTING DEVICES TACTICAL OPTICS MARKET SIZE, BY REGION, 2018–2025 (USD MILLION)

TABLE 20 CAMERAS & DISPLAYS TACTICAL OPTICS MARKET SIZE, BY TYPE, 2018–2025 (USD MILLION)

TABLE 21 CAMERAS & DISPLAYS TACTICAL OPTICS MARKET SIZE, BY REGION, 2018–2025 (USD MILLION)

TABLE 22 TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 23 GROUND TACTICAL OPTICS MARKET SIZE, BY TYPE, 2018–2025 (USD MILLION)

TABLE 24 GROUND TACTICAL OPTICS MARKET SIZE, BY REGION, 2018–2025 (USD MILLION)

TABLE 25 VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 26 TACTICAL OPTICS: CONFIGURATIONS FOR ARMORED VEHICLES

TABLE 27 GLOBAL FLEET OF MAIN BATTLE TANKS AS OF DECEMBER 2019

TABLE 28 GLOBAL FLEET OF INFANTRY FIGHTING VEHICLES AS OF DECEMBER 2019

TABLE 29 GLOBAL FLEET OF SELF-PROPELLED HOWITZERS AS OF DECEMBER 2019

TABLE 30 PORTABLE TACTICAL OPTICS MARKET SIZE, BY PORTABLE TYPE, 2018–2025 (USD MILLION)

TABLE 31 NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 32 NAVAL TACTICAL OPTICS MARKET SIZE, BY REGION, 2018–2025 (USD MILLION)

TABLE 33 NUMBER OF AIRCRAFT CARRIERS, BY COUNTRY, FEBRUARY 2020

TABLE 34 NUMBER OF DESTROYERS, BY COUNTRY, FEBRUARY 2020

TABLE 35 NUMBER OF FRIGATES, BY COUNTRY, FEBRUARY 2020

TABLE 36 NUMBER OF CORVETTES, BY COUNTRY, FEBRUARY 2020

TABLE 37 NUMBER OF OPVS, BY COUNTRY, FEBRUARY 2020

TABLE 38 AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 39 AIRBORNE TACTICAL OPTICS MARKET SIZE, BY REGION, 2018–2025 (USD MILLION)

TABLE 40 NUMBER OF FIGHTER AIRCRAFT, BY COUNTRY, FEBRUARY 2020

TABLE 41 NUMBER OF MILITARY HELICOPTERS, BY COUNTRY, FEBRUARY 2020

TABLE 42 NUMBER OF SPECIAL MISSION AIRCRAFT, BY COUNTRY, FEBRUARY 2020

TABLE 43 TACTICAL OPTICS MARKET SIZE, BY APPLICATION, 2018–2025 (USD MILLION)

TABLE 44 TACTICAL OPTICS MARKET SIZE FOR INTELLIGENCE, SURVEILLANCE, & RECONNAISSANCE, BY REGION, 2018–2025 (USD MILLION)

TABLE 45 TACTICAL OPTICS MARKET SIZE FOR TARGET IDENTIFICATION & ACQUISITION, BY REGION, 2018–2025 (USD MILLION)

TABLE 46 TACTICAL OPTICS MARKET SIZE FOR SEARCH & RESCUE, BY REGION, 2018–2025 (USD MILLION)

TABLE 47 TACTICAL OPTICS CONTRACTS, PROCUREMENTS, AND MODERNIZATION PLANS, BY APPLICATION

TABLE 48 TACTICAL OPTICS MARKET SIZE FOR BORDER & COASTAL PATROL, BY REGION, 2018–2025 (USD MILLION)

TABLE 49 TACTICAL OPTICS MARKET SIZE, BY END USE, 2018–2025 (USD MILLION)

TABLE 50 MANNED PLATFORM TACTICAL OPTICS MARKET SIZE, BY REGION, 2018–2025 (USD MILLION)

TABLE 51 WEAPON MOUNTED TACTICAL OPTICS MARKET SIZE, BY REGION, 2018–2025 (USD MILLION)

TABLE 52 SOLDIER TACTICAL OPTICS MARKET SIZE, BY REGION, 2018–2025 (USD MILLION)

TABLE 53 UNMANNED PLATFORM TACTICAL OPTICS MARKET SIZE, BY REGION, 2018–2025 (USD MILLION)

TABLE 54 TACTICAL OPTICS MARKET SIZE, BY RANGE, 2018–2025 (USD MILLION)

TABLE 55 SHORT-RANGE (< 3 KM) TACTICAL OPTICS MARKET SIZE, BY REGION, 2018–2025 (USD MILLION)

TABLE 56 MEDIUM RANGE (3-25 KM) TACTICAL OPTICS MARKET SIZE, BY REGION, 2018–2025 (USD MILLION)

TABLE 57 LONG-RANGE (> 25 KM) TACTICAL OPTICS MARKET SIZE, BY REGION, 2018–2025 (USD MILLION)

TABLE 58 TACTICAL OPTICS MARKET SIZE, BY REGION, 2018–2025 (USD MILLION)

TABLE 59 NORTH AMERICA: TACTICAL OPTICS MARKET SIZE, BY PRODUCT, 2018–2025 (USD MILLION)

TABLE 60 NORTH AMERICA: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 61 NORTH AMERICA: TACTICAL OPTICS MARKET SIZE, BY END USE, 2018–2025 (USD MILLION)

TABLE 62 NORTH AMERICA: TACTICAL OPTICS MARKET SIZE, BY APPLICATION, 2018–2025 (USD MILLION)

TABLE 63 NORTH AMERICA: GROUND TACTICAL OPTICS MARKET SIZE, BY RANGE, 2018–2025 (USD MILLION)

TABLE 64 NORTH AMERICA: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 65 NORTH AMERICA: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 66 NORTH AMERICA: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 67 NORTH AMERICA: TACTICAL OPTICS MARKET SIZE, BY COUNTRY, 2018–2025 (USD MILLION)

TABLE 68 US DEFENSE CONTRACTS FOR TACTICAL OPTICS, 2012–2020

TABLE 69 US: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 70 US: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 71 US: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 72 US: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 73 CANADA: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 74 CANADA: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 75 CANADA: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 76 CANADA: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 77 EUROPE: TACTICAL OPTICS MARKET SIZE, BY PRODUCT, 2018–2025 (USD MILLION)

TABLE 78 EUROPE: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 79 EUROPE: TACTICAL OPTICS MARKET SIZE, BY END USE, 2018–2025 (USD MILLION)

TABLE 80 EUROPE: TACTICAL OPTICS MARKET SIZE, BY APPLICATION, 2018–2025 (USD MILLION)

TABLE 81 EUROPE: GROUND TACTICAL OPTICS MARKET SIZE, BY RANGE, 2018–2025 (USD MILLION)

TABLE 82 EUROPE: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 83 EUROPE: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 84 EUROPE: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 85 EUROPE: TACTICAL OPTICS MARKET SIZE, BY COUNTRY, 2018–2025 (USD MILLION)

TABLE 86 FRANCE: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 87 FRANCE: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 88 FRANCE: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 89 FRANCE: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 90 RUSSIA: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 91 RUSSIA: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 92 RUSSIA: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 93 RUSSIA: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 94 UK: EQUIPMENT PLAN FUNDING ALLOCATIONS, 2018-2028

TABLE 95 UK: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 96 UK: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 97 UK: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 98 UK: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 99 GERMANY: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 100 GERMANY: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 101 GERMANY: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 102 GERMANY: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 103 ITALY: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 104 ITALY: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 105 ITALY: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 106 ITALY: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 107 SPAIN: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 108 SPAIN: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 109 SPAIN: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 110 SPAIN: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 111 POLAND: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 112 POLAND: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 113 POLAND: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 114 POLAND: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 115 ASIA PACIFIC: TACTICAL OPTICS MARKET SIZE, BY PRODUCT, 2018–2025 (USD MILLION)

TABLE 116 ASIA PACIFIC: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 117 ASIA PACIFIC: TACTICAL OPTICS MARKET SIZE, BY END USE, 2018–2025 (USD MILLION)

TABLE 118 ASIA PACIFIC: TACTICAL OPTICS MARKET SIZE, BY APPLICATION, 2018–2025 (USD MILLION)

TABLE 119 ASIA PACIFIC: GROUND TACTICAL OPTICS MARKET SIZE, BY RANGE, 2018–2025 (USD MILLION)

TABLE 120 ASIA PACIFIC: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 121 ASIA PACIFIC: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 122 ASIA PACIFIC: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 123 ASIA PACIFIC: TACTICAL OPTICS MARKET SIZE, BY COUNTRY, 2018–2025 (USD MILLION)

TABLE 124 CHINA: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 125 CHINA: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 126 CHINA: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 127 CHINA: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 128 INDIA: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 129 INDIA: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 130 INDIA: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 131 INDIA: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 132 JAPAN: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 133 JAPAN: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 134 JAPAN: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 135 JAPAN: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 136 SOUTH KOREA: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 137 SOUTH KOREA: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 138 SOUTH KOREA: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 139 SOUTH KOREA: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 140 AUSTRALIA: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 141 AUSTRALIA: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 142 AUSTRALIA: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 143 AUSTRALIA: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 144 MIDDLE EAST: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 145 MIDDLE EAST: TACTICAL OPTICS MARKET SIZE, BY END USE, 2018–2025 (USD MILLION)

TABLE 146 MIDDLE EAST: TACTICAL OPTICS MARKET SIZE, BY APPLICATION, 2018–2025 (USD MILLION)

TABLE 147 MIDDLE EAST: GROUND TACTICAL OPTICS MARKET SIZE, BY RANGE, 2018–2025 (USD MILLION)

TABLE 148 MIDDLE EAST: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 149 MIDDLE EAST: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 150 MIDDLE EAST: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 151 MIDDLE EAST: TACTICAL OPTICS MARKET SIZE, BY COUNTRY, 2018–2025 (USD MILLION)

TABLE 152 SAUDI ARABIA: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 153 SAUDI ARABIA: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 154 SAUDI ARABIA: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 155 SAUDI ARABIA: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 156 TURKEY: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 157 TURKEY: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 158 TURKEY: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 159 TURKEY: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 160 ISRAEL: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 161 ISRAEL: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 162 ISRAEL: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 163 ISRAEL: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 164 SOUTH AMERICA: TACTICAL OPTICS MARKET SIZE, BY PRODUCT, 2018–2025 (USD MILLION)

TABLE 165 SOUTH AMERICA: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 166 SOUTH AMERICA: TACTICAL OPTICS MARKET SIZE, BY END USE, 2018–2025 (USD MILLION)

TABLE 167 SOUTH AMERICA: TACTICAL OPTICS MARKET SIZE, BY APPLICATION, 2018–2025 (USD MILLION)

TABLE 168 SOUTH AMERICA: GROUND TACTICAL OPTICS MARKET SIZE, BY RANGE, 2018–2025 (USD MILLION)

TABLE 169 SOUTH AMERICA: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 170 SOUTH AMERICA: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 171 SOUTH AMERICA: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 172 SOUTH AMERICA: TACTICAL OPTICS MARKET SIZE, BY COUNTRY, 2018–2025 (USD MILLION)

TABLE 173 BRAZIL: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 174 BRAZIL: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 175 BRAZIL: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 176 BRAZIL: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 177 MEXICO: TACTICAL OPTICS MARKET SIZE, BY PLATFORM, 2018–2025 (USD MILLION)

TABLE 178 MEXICO: VEHICLE-MOUNTED TACTICAL OPTICS MARKET SIZE, BY VEHICLE TYPE, 2018–2025 (USD MILLION)

TABLE 179 MEXICO: NAVAL TACTICAL OPTICS MARKET SIZE, BY VESSEL TYPE, 2018–2025 (USD MILLION)

TABLE 180 MEXICO: AIRBORNE TACTICAL OPTICS MARKET SIZE, BY AIRCRAFT TYPE, 2018–2025 (USD MILLION)

TABLE 181 CONTRACTS, JANUARY 2016– FEBRUARY 2020

TABLE 182 NEW PRODUCT DEVELOPMENTS, JANUARY 2016– FEBRUARY 2020

TABLE 183 ACQUISITIONS JANUARY 2016–FEBRUARY 2020

TABLE 184 CONTRACTS, JULY 2016–MARCH 2020

TABLE 185 NEW PRODUCT LAUNCHES, JULY 2016–MARCH 2020

TABLE 186 ACQUISITIONS AND PARTNERSHIPS, JULY 2016–MARCH 2020

LIST OF FIGURES (77 FIGURES)

FIGURE 1 REPORT PROCESS FLOW

FIGURE 2 TACTICAL OPTICS MARKET: RESEARCH DESIGN

FIGURE 3 BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

FIGURE 6 DATA TRIANGULATION

FIGURE 7 BY PRODUCT, CAMERAS & DISPLAYS SEGMENT TO DOMINATE TACTICAL OPTICS MARKET FROM 2020 TO 2025

FIGURE 8 BY APPLICATION, TARGET IDENTIFICATION & ACQUISITION SEGMENT TO LEAD TACTICAL OPTICS MARKET FROM 2020 TO 2025

FIGURE 9 BY END USE, UNMANNED PLATFORM SEGMENT TO REGISTER HIGHEST CAGR FROM 2020 TO 2025

FIGURE 10 BY PLATFORM, GROUND SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE FROM 2020 TO 2025

FIGURE 11 BY RANGE, LONG-RANGE (> 25 KM) SEGMENT TO LEAD TACTICAL OPTICS MARKET FROM 2020 TO 2025

FIGURE 12 TACTICAL OPTICS MARKET IN ASIA PACIFIC TO ACCOUNT FOR THE LARGEST SHARE OF THE MARKET FROM 2020 TO 2025

FIGURE 13 INCREASING ORDERS FOR COMBAT AIRCRAFT, ARMORED VEHICLES, AND NAVAL SHIPS DRIVING THE MARKET FOR TACTICAL OPTICS

FIGURE 14 UNMANNED GROUND VEHICLES SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 15 CORVETTES SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 16 UNMANNED AERIAL VEHICLES SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 17 ELECTRO-OPTIC/INFRARED SIGHTS SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 18 TARGET ACQUIS ION & SURVEILLANCE SYSTEMS SEGMENT TO LEAD TACTICAL OPTICS MARKET DURING FORECAST PERIOD

FIGURE 19 ELECTRO-OPTIC/INFRARED CAMERAS SEGMENT TO LEAD TACTICAL OPTICS MARKET DURING FORECAST PERIOD

FIGURE 20 TACTICAL OPTICS MARKET IN NORTH AMERICA PROJECTED TO WITNESS HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 21 EVOLUTION OF THE RIFLESCOPE

FIGURE 22 TACTICAL OPTICS MARKET DYNAMICS: DRIVERS, OPPORTUNITIES, AND CHALLENGES

FIGURE 23 TOP 15 MILITARY SPENDING COUNTRIES, 2019 (USD BILLION)

FIGURE 24 MAJOR INDUSTRY TRENDS

FIGURE 25 CAMERAS & DISPLAYS SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 26 AIRBORNE SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 27 INTELLIGENCE, SURVEILLANCE, & RECONNAISSANCE SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 28 UNMANNED PLATFORM SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 29 LONG-RANGE (> 25 KM) SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 30 ASIA PACIFIC ESTIMATED TO ACCOUNT FOR LARGEST SHARE OF TACTICAL OPTICS MARKET IN 2020

FIGURE 31 NORTH AMERICA TACTICAL OPTICS MARKET SNAPSHOT

FIGURE 32 US DEFENSE BUDGET, 2010–2019

FIGURE 33 US MODERNIZATION BUDGET BREAKDOWN, 2019 (USD BILLION)

FIGURE 34 CANADA DEFENSE BUDGET, 2010–2019

FIGURE 35 EUROPE TACTICAL OPTICS MARKET SNAPSHOT

FIGURE 36 FRANCE DEFENSE BUDGET, 2010–2019

FIGURE 37 RUSSIA DEFENSE BUDGET, 2010–2019

FIGURE 38 UK DEFENSE BUDGET, 2010–2019

FIGURE 39 GERMANY DEFENSE BUDGET, 2010–2019

FIGURE 40 ITALY DEFENSE BUDGET, 2010–2019

FIGURE 41 SPAIN DEFENSE BUDGET 2010-2018

FIGURE 42 POLAND DEFENSE BUDGET, 2010–2019

FIGURE 43 ASIA PACIFIC TACTICAL OPTICS MARKET SNAPSHOT

FIGURE 44 CHINA DEFENSE BUDGET 2010-2018

FIGURE 45 INDIA DEFENSE BUDGET, 2010–2019

FIGURE 46 JAPAN DEFENSE BUDGET, 2010–2019

FIGURE 47 SOUTH KOREA DEFENSE BUDGET, 2010–2019

FIGURE 48 AUSTRALIA DEFENSE BUDGET, 2010–2019

FIGURE 49 MIDDLE EAST TACTICAL OPTICS MARKET SNAPSHOT

FIGURE 50 SAUDI ARABIA DEFENSE BUDGET, 2010–2019

FIGURE 51 TURKEY DEFENSE BUDGET, 2010–2019

FIGURE 52 ISRAEL DEFENSE BUDGET, 2010–2019

FIGURE 53 BRAZIL DEFENSE BUDGET, 2010–2019

FIGURE 54 MEXICO DEFENSE BUDGET, 2010–2019

FIGURE 55 RANK ANALYSIS OF KEY PLAYERS IN THE TACTICAL OPTICS MARKET, 2019

FIGURE 56 TACTICAL OPTICS (TIER 1 COMPANIES) COMPETITIVE LEADERSHIP MAPPING, 2019

FIGURE 57 PRODUCT PORTFOLIO ANALYSIS OF TOP PLAYERS IN TACTICAL OPTICS MARKET (TIER 1 COMPANIES)

FIGURE 58 BUSINESS STRATEGY EXCELLENCE OF TOP PLAYERS IN TACTICAL OPTICS MARKET (TIER 1 COMPANIES)

FIGURE 59 RANK ANALYSIS OF KEY PLAYERS IN THE TACTICAL OPTICS MARKET, 2019

FIGURE 60 TACTICAL OPTICS (TIER 2 & 3 COMPANIES) COMPETITIVE LEADERSHIP MAPPING, 2019

FIGURE 61 PRODUCT PORTFOLIO ANALYSIS OF TOP PLAYERS IN TACTICAL OPTICS MARKET (TIER 2 & 3 COMPANIES)

FIGURE 62 BUSINESS STRATEGY EXCELLENCE OF TOP PLAYERS IN TACTICAL OPTICS MARKET (TIER 2 & 3 COMPANIES)

FIGURE 63 LEONARDO S.P.A.: COMPANY SNAPSHOT

FIGURE 64 BAE SYSTEMS, PLC.: COMPANY SNAPSHOT

FIGURE 65 BAE SYSTEMS, PLC: BUSINESS STRATEGY AND RIGHT TO WIN FACTOR

FIGURE 66 ELBIT SYSTEMS LTD.: COMPANY SNAPSHOT

FIGURE 67 ELBIT SYSTEMS LTD.: BUSINESS STRATEGY AND RIGHT TO WIN FACTOR

FIGURE 68 KONGSBERG GRUPPEN AS: COMPANY SNAPSHOT

FIGURE 69 KONGSBERG GRUPPEN AS: BUSINESS STRATEGY AND RIGHT TO WIN FACTOR

FIGURE 70 L3HARRIS TECHNOLOGIES: COMPANY SNAPSHOT

FIGURE 71 LOCKHEED MARTIN CORPORATION: COMPANY SNAPSHOT

FIGURE 72 NORTHROP GRUMMAN CORPORATION: COMPANY SNAPSHOT

FIGURE 73 RAYTHEON COMPANY: COMPANY SNAPSHOT

FIGURE 74 THALES GROUP: COMPANY SNAPSHOT

FIGURE 75 SAAB AB: COMPANY SNAPSHOT

FIGURE 76 FLIR SYSTEMS, INC.: COMPANY SNAPSHOT

FIGURE 77 ISRAEL AEROSPACE INDUSTRIES: COMPANY SNAPSHOT

Extensive secondary research was undertaken to collect information on the tactical optics market, its adjacent markets, and its parent market. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both the demand- and supply-side analyses were employed to estimate the overall size of the market. Thereafter, the market breakdown and data triangulation procedures were used to estimate the market sizes of different segments and subsegments.

Secondary Research

In the secondary research process, various sources, such as Statista, World Bank, Global Firepower, Defense IQ, Factiva, Bloomberg, BusinessWeek, SEC filings, annual reports, press releases & investor presentations of companies, certified publications, and articles by recognized authors, were referred for identifying and collecting information on the tactical optics market.

Primary Research

The tactical optics market comprises several stakeholders, such as raw material suppliers, processors, end-product manufacturers, and integratory and regulatory organizations in its supply chain. The military forces of different countries characterize the demand side of this market. Technologically advanced hardware manufacturers characterize the supply side for tactical optics catering to the ground, naval, and airborne platforms.

Following is the breakdown of the primary respondents that were interviewed to obtain qualitative and quantitative information about the tactical optics market.

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

Both the top-down and bottom-up approaches were used to estimate and validate the total size of the tactical optics market. These methods were also used extensively to estimate the size of various segments and subsegments of the market. The research methodology used to estimate the market size included the following.

- Key players in the industry and market were identified through extensive secondary research of their product matrix, their geographical presence, and developments undertaken by them.

- All percentage shares, splits, and breakdowns were determined using secondary sources and verified through primary sources.

Data Triangulation

After arriving at the overall size of the tactical optics market using the market size estimation processes explained above, the market was split into several segments and subsegments. To complete the overall market engineering process and arrive at the exact statistics of each market segment and subsegment, the data triangulation and market breakdown procedures were employed, wherever applicable. The data was triangulated by studying various factors and trends from the demand as well as the supply sides of the tactical optics market.

Report Objectives

- To define, describe, and forecast the size of the tactical optics market based on product, platform, application, end use, range, and region

- To identify and analyze key drivers, restraints, opportunities, and challenges influencing the growth of the market

- To identify industry trends, market trends, and technology trends currently prevailing in the market

- To analyze micromarkets with respect to individual technological trends, prospects, and their contribution to the overall market

- To forecast the size of segments of the tactical optics market based on five regions, namely, North America, Europe, Asia Pacific, Middle East, and South America, along with major countries in each region

- To provide a detailed competitive landscape of the market and analyze competitive growth strategies, such as contracts, new product launches, acquisitions, partnerships, and collaborations, adopted by key players in the market

- To identify detailed financial positions, key products, unique selling points, and key developments of leading companies in the market

- To strategically profile key players and comprehensively analyze their market ranking and core competencies

Available Customizations

With the given market data, MarketsandMarkets offers customizations according to the specific requirements of companies.

Product Analysis

- Product matrix, which provides a detailed comparison of the product portfolio of each company

Company Information

- Detailed analysis and profiles of additional market players (up to 5)

Growth opportunities and latent adjacency in Tactical Optics Market