Cryogenic Insulation Market by Type (PU & PIR, Cellular Glass, Polystyrene, Fiberglass, Perlite), Cryogenic Equipment (Tanks, Valves), End-Use Industry (Energy & Power, Chemicals, Metallurgical, Electronics, Shipping) - Global Forecast to 2023

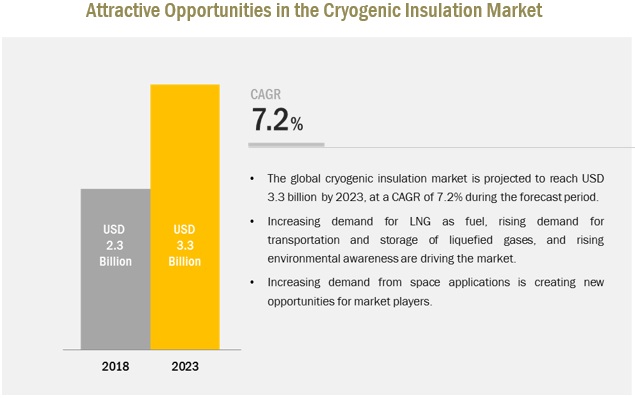

[143 Pages Report] The cryogenic insulation market size is estimated to be USD 2.3 billion in 2018 and is projected reach USD 3.3 billion by 2023, at a CAGR of 7.20% between 2018 and 2023. The study involved four major activities to estimate the market size for cryogenic insulation. Exhaustive secondary research was done to collect information on the market, the peer market, and the parent market. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the complete market size. Thereafter, the market breakdown and data triangulation procedures were used to estimate the market size of the segments and subsegments.

Secondary Research

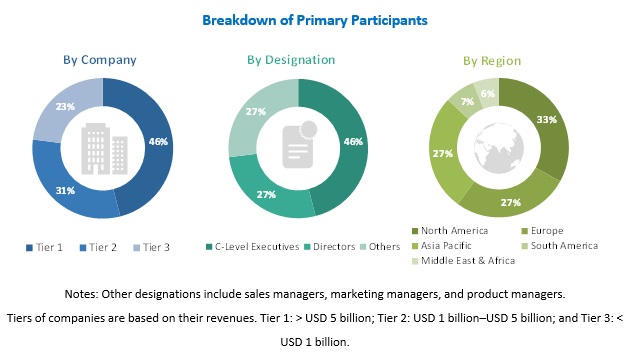

Secondary sources used in this study included annual reports, press releases, and investor presentations of companies; white papers; certified publications; articles from recognized authors; and gold standard & silver standard websites such as Factiva, ICIS, Bloomberg, and others. Findings of this study were verified through primary research by conducting extensive interviews with key officials such as CEOs, VPs, directors, and other executives. The breakdown of profiles of the primary interviewees is illustrated in the figure below:

Primary Research

The cryogenic insulation market comprises several stakeholders such as raw material suppliers, end-product manufacturers, and regulatory organizations in the supply chain. The demand side of this market is characterized by the development of energy & power, chemicals, metallurgical, electronics, and shipping industries. The supply side is characterized by advancements in technology and diverse application industries. Various primary sources from both the supply and demand sides of the market were interviewed to obtain qualitative and quantitative information.

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

Both top-down and bottom-up approaches were used to estimate and validate the total size of the cryogenic insulation market. These methods were also used extensively to estimate the size of various subsegments in the market. The research methodology used to estimate the market size includes the following:

The key players in the industry have been identified through extensive secondary research.

- The industry�s supply chain and market size, in terms of value, have been determined through primary and secondary research processes.

- All percentage shares, splits, and breakdowns have been determined using secondary sources and verified through primary sources.

Data Triangulation

After arriving at the overall market size using the market size estimation processes as explained above�the market was split into several segments and subsegments. In order to complete the overall market engineering process and arrive at the exact statistics of each market segment and subsegment, the data triangulation and market breakdown procedures were employed, wherever applicable. The data was triangulated by studying various factors and trends from both the demand and supply sides in the energy & power, chemical, metallurgical electronics, shipping, and other industries.

Report Objectives

- To analyze and forecast the size of the cryogenic insulation market in terms value

- To define, describe, and segment the cryogenic insulation market on the basis of type, form, cryogenic equipment, and end-use industry

- To forecast the size of the market segments for regions such as APAC, North America, Europe, South America, and the Middle East & Africa

- To provide detailed information regarding key factors, such as drivers, restraints, and opportunities influencing the growth of the market

- To strategically analyze the segmented markets with respect to individual growth trends, prospects, and contribution to the overall market

- To identify and analyze opportunities for stakeholders in the market

- To analyze competitive developments such as expansions, new product launches, agreements in the cryogenic insulation market

- To strategically profile key players and comprehensively analyze their core competencies

Scope of the Report

|

Report Metric |

Details |

|

Market Size available for years |

2016-2023 |

|

Base year considered |

2017 |

| Forecast period | 2018�2023 |

| Forecast units | Value (USD Million) |

| Segments covered | Type, Cryogenic Equipment, Form, End-Use Industry, and Region |

| Regions covered | APAC, North America, Europe, Middle East & Africa, and South America |

| Companies covered | Armacell International Holding GmbH (Germany), Lydall Inc. (US), BASF SE (Germany), Cabot Corporation (US), Rochling Group (Germany), and Johns Manville Inc. (US). Top 15 major players covered. |

This report categorizes the global cryogenic insulation market based on type, form, cryogenic equipment, end-use industry, and region.

On the basis of type, the cryogenic insulation market has been segmented as follows:

- PU & PIR

- Cellular Glass

- Polystyrene

- Fiberglass

- Perlite

- Others (aerogel, elastomer foams)

On the basis of form, the cryogenic insulation market has been segmented as follows:

- Bulk-fill

- Foam

- Multi-layer

On the basis of cryogenic equipment, the cryogenic insulation market has been segmented as follows:

- Tanks

- Valves

- Vaporizers

- Pumps

- Others (dewar vessels, tunnel freezers, gauges, and flanges, among others)

On the basis of end-use Industry, the cryogenic insulation market has been segmented as follows:

- Energy & Power

- Chemicals

- Metallurgical

- Electronics

- Shipping

- Others (food & beverage, healthcare, transportation of perishable items, and space applications, among others)

On the basis of region, the cryogenic insulation market has been segmented as follows:

- APAC

- North America

- Europe

- Middle East & Arica

- South America

Available Customizations

Along with the given market data, MarketsandMarkets offers customizations according to the company�s specific needs. The following customization options are available for the report:

Regional Analysis

- Further breakdown of a region with respect to a particular country or additional end-use industry

Company Information

- Detailed analysis and profiles of additional market players (up to five)

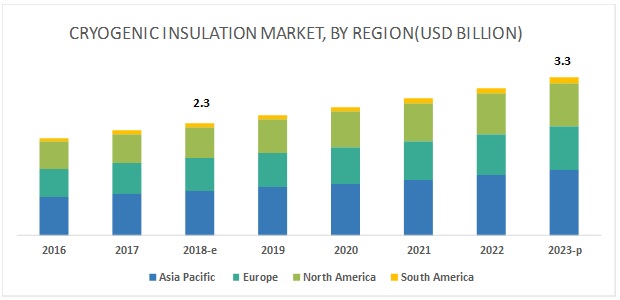

The cryogenic insulation market size is estimated to be USD 2.3 billion in 2018 and is projected reach USD 3.3 billion by 2023, at a CAGR of 7.20% between 2018 and 2023. The cryogenic insulation market is mainly driven by the rising demand for LNG as fuel in developed and developing economies. Rising environmental awareness is also contributing to the growth of the market. Growing demand for cryogenic technologies in space applications has created various opportunities for cryogenic insulation manufacturers. APAC is the key market for cryogenic insulations, globally, followed by Europe and North America. One of the primary drivers of the market is the increasing demand for transportation, storage, and liquefaction of natural gas to LNG in these regions.

PU & PIR segment is expected to be the largest contributor to the overall cryogenic insulation market during the forecast period.

On the basis of type, the cryogenic insulation market has been segmented into PU & PIR, cellular glass, polystyrene, fiberglass, perlite, plastic, rubber, metal, ceramic, and others. The PU & PIR segment is expected to lead the cryogenic insulation market between 2018 and 2023, in terms of value. The higher demand for PU & PIR is mainly attributed to their properties and widespread applications. PUR & PIR foam is lightweight, moisture and fire resistant, has low thermal conductivity and density, and provides better structural performance. These properties enable their use in cryogenic conditions. They are used in various applications such as cold storage building, coolers, freezers, tank & pipe insulation, and household refrigerators.

The tank segment accounts for the largest share of the overall market.

On the basis of cryogenic equipment, the cryogenic insulation market has been segmented into tanks, valves, vaporizers, pump, and others. The tank segment is expected to account for the largest share of the cryogenic insulation market during the forecast period. The dominance of the tank segment is expected to continue during the forecast period due to its increasing demand from end-use industries such as energy & power for the storage and transportation of LNG.

The energy & power segment is projected to be the fastest-growing end-use industry of cryogenic insulation during the forecast period.

On the basis of end-use industry, the cryogenic insulation market has been segmented into energy & power, chemicals, metallurgical, electronics, shipping, and others. The energy & power segment is estimated to be the largest end-use industry of the cryogenic insulation market, in terms of value, during the forecast period. The demand for cryogenic insulation in the industry is expected to increase as a result of increasing demand for LNG as fuel.

APAC is expected to account for the largest share of the cryogenic insulation market during the forecast period.

The APAC cryogenic insulation market accounted for the largest share in the global market. The market in the region is driven by the high demand from rapidly growing end-use industries such as energy & power. Rising demand for LNG, increasing investment in the energy sector, urbanization, industrialization, and infrastructural development are expected to drive the cryogenic insulation market during the forecast period.

Key Market Players

Key market players profiled in the report include Armacell International Holding GmbH (Germany), Lydall Inc. (US), BASF SE (Germany), Cabot Corporation (US), Rochling Group (Germany), and Johns Manville Inc. (US).

Lydall Inc. is among the leading players in the cryogenic insulation market. The company through its wide range of product portfolio caters to the specific demand of its customers. The company is focusing on enhancing its market reach by entering new markets and is introducing new products. For instance, Lydall Inc. launched a super-insulating cryogenic media named Cryotherm 233B made from non-biopersistent glass microfibers in March 2014. This enabled the company to expand its product offerings.

Cabot Corporation is one of the leading specialty chemicals and performance materials company. It caters to a wide range of industries, including transportation, infrastructure, environment, and consumer. The company is producing innovative products in the market, which will enable it to cater to the specific demands of its customers and gain competitive advantage. The company also adopted agreement as a strategy to increase its market share and cater to the increasing demand for cryogenic insulation. For instance, Cabot Corporation entered into an agreement with Johns Manville Industrial Insulation Group (IIG) in May 2016. The agreement enabled both companies to produce high-performance insulation for oil & gas applications using Cabot�s proprietary technology and aerogel products.

Recent Developments

- In September 2018, Rochling Group launched Lignostone cryogenic. The product is best suitable to be used for cryogenic tank insulation in LNG and LPG carriers. This will enable the company to serve the oil & gas industry with its advanced products.

- In May 2016, Cabot Corporation entered into an agreement with Johns Manville Industrial Insulation Group (IIG). The agreement will enable both companies to produce high-performance insulation for the oil & gas industry.

- In December 2016, Imerys Perlite USA expanded its assets in cryogenic insulation services by purchasing mobile perlite expanders and related services from JC Hall Company. This will enable the company to improve its cryogenic insulation products & services.

- In March 2014, Lydall Inc. launched a super-insulating cryogenic media named Cryotherm 233B made from non-biopersistent glass microfibers. This enabled the company to expand its product offerings.

Key Questions addressed by the report

- Major developments impacting the market?

- Where will all these developments take the industry in the mid to long term?

- What are the upcoming types of cryogenic insulation?

- What are the emerging end-use industries for cryogenic insulation?

- What are the major factors impacting the market growth during the forecast period?

To speak to our analyst for a discussion on the above findings, click Speak to Analyst

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Table of Contents

1 Introduction (Page No. - 14)

1.1 Objectives of the Study

1.2 Market Definition

1.3 Market Scope

1.3.1 Years Considered for the Study

1.4 Currency

1.5 Limitations

1.6 Stakeholders

2 Research Methodology (Page No. - 17)

2.1 Research Data

2.1.1 Secondary Data

2.1.1.1 Key Data From Secondary Sources

2.1.2 Primary Data

2.1.2.1 Key Data From Primary Sources

2.1.2.2 Breakdown of Primary Interviews

2.2 Market Size Estimation

2.2.1 Bottom-Up Approach

2.2.2 Top-Down Approach

2.3 Data Triangulation

2.4 Assumptions

3 Executive Summary (Page No. - 24)

4 Premium Insights (Page No. - 29)

4.1 Attractive Opportunities in Cryogenic Insulation Market

4.2 APAC Cryogenic Insulation Market, By End-Use Industry and Country

4.3 Cryogenic Insulation Market, By Region

4.4 Cryogenic Insulation Market, By Region and End-Use Industry

4.5 Cryogenic Insulation Market, By Country

5 Market Overview (Page No. - 34)

5.1 Introduction

5.2 Market Dynamics

5.2.1 Drivers

5.2.1.1 Rising Demand for LNG as Fuel

5.2.1.2 Rising Environmental Awareness

5.2.2 Opportunities

5.2.2.1 Growing Demand for Cryogenic Technologies From Space Applications

5.2.3 Restraints

5.2.3.1 Volatile Raw Material Prices

5.3 Porter�s Five Forces Analysis

5.3.1 Threat of Substitutes

5.3.2 Threat of New Entrants

5.3.3 Bargaining Power of Suppliers

5.3.4 Bargaining Power of Buyers

5.3.5 Intensity of Competitive Rivalry

5.4 Macroeconomic Indicators

5.4.1 GDP Forecast of Major Economies

5.4.2 Trends and Forecast of Natural Gas Industry and Its Impact on Cryogenic Insulation Market

6 Cryogenic Insulation Market, By Type (Page No. - 43)

6.1 Introduction

6.2 Pu & Pir

6.3 Cellular Glass

6.4 Polystyrene Foam

6.5 Fiberglass

6.6 Perlite

6.7 Others

7 Cryogenic Insulation Market, By Cryogenic Equipment (Page No. - 51)

7.1 Introduction

7.2 Tank

7.3 Valve

7.3.1 Rising Demand for Transport of Liquified Gases to Drive the Demand for Valves

7.4 Vaporizer

7.5 Pump

7.5.1 Increase in LNG Projects and Import Terminals are Expected to Drive the Demand for Pumps

7.6 Other

8 Cryogenic Insulation Market, By Form (Page No. - 59)

8.1 Introduction

8.2 Mulit-Layer

8.3 Foam

8.4 Bulk-Fill

9 Cryogenic Insulation Market, By End-Use Industry (Page No. - 63)

9.1 Introduction

9.2 Energy & Power

9.2.1 Energy & Power Segment Accounted for the Largest End-Use Industry of Cryogenic Insulation

9.3 Chemicals

9.3.1 Growing Chemical Industry in Emerging Economies to Drive the Demand for Cryogenic Insulation

9.4 Metallurgical

9.4.1 Increasing Spending on Infrastructure to Drive the Demand for Cryogenic Insulation in Metallurgical Industry

9.5 Electronics

9.5.1 Growing Electronics Industry in APAC is Expected to Drive the Demand for Cryogenic Insulation

9.6 Shipping

9.6.1 Rising Demand for LNG as Fuel to Drive the Demand for Cryogenic Insulation in Shipping Industry

9.7 Others

10 Cryogenic Insulation Market, By Region (Page No. - 71)

10.1 Introduction

10.2 APAC

10.2.1 China

10.2.1.1 China to Be the Largest Country for Cryogenic Insulation in APAC Region

10.2.2 India

10.2.2.1 Increasing Demand From Energy & Power Industry to Contribute Significantly to the Growth of the Cryogenic Insulation in the Country

10.2.3 Australia

10.2.3.1 Australia to Be the Fastest-Growing Country for Cryogenic Insulation in APAC Region

10.2.4 Japan

10.2.4.1 Rising Demand for Renewable Source of Energy to Drive the Demand for Cryogenic Insulation in the Country

10.2.5 Malaysia

10.2.5.1 Rising Demand for LNG Transportation and Storage to Drive the Demand for Cryogenic Insulation in the Country

10.3 North America

10.3.1 Us

10.3.1.1 US Accounted for the Largest Market Size in the Cryogenic Insulation Market in North America

10.3.2 Canada

10.3.2.1 The Growing Demand From Energy & Power Industry Will Support the Demand for Cryogenic Insulation in the Country

10.3.3 Mexico

10.3.3.1 Mexico Accounted for the Third Largest Market Size in the Cryogenic Insulation Market in North America

10.4 Europe

10.4.1 Uk

10.4.1.1 Rising Demand From Emerging Applications to Drive the Demand for Cryogenic Insulation in the Country

10.4.2 Russia

10.4.2.1 Rising Demand From Energy & Power Sector to Drive the Demand for Cryogenic Insulation in the Country

10.4.3 France

10.4.3.1 Rising Demand for Means of Renewable Source of Energy to Drive the Demand for Cryogenic Insulation in the Country

10.4.4 Germany

10.4.4.1 Rising Demand From Emerging Applications to Drive the Demand for Cryogenic Insulation in the Country

10.5 Middle East & Africa

10.5.1 Saudi Arabia

10.5.1.1 Energy & Power Segment to Be the Fastest Growing End-Use Industry for Cryogenic Insulation Market in Saudi Arabia

10.5.2 Qatar

10.5.2.1 Qatar to Be the Fastest-Growing Country for Cryogenic Insulation in Middle East & Africa Region

10.5.3 UAE

10.5.3.1 Increasing Demand From Energy & Power Industry to Drive the Market in the Country

10.5.4 South Africa

10.5.4.1 Energy & Power Segment to Be the Fastest-Growing End-Use Industry for Cryogenic Insulation in South Africa

10.5.5 Nigeria

10.5.5.1 Increasing in Demand for Storage and Transportation Facilities for LNG to Drive the Demand for Cryogenic Insulation in the Country

10.5.6 Algeria

10.5.6.1 Increasing Domestic Gas Demands and Gas Processing Industries to Drive the Demand for Cryogenic Insulation in the Country

10.6 South America

10.6.1 Brazil

10.6.1.1 Brazil to Be the Largest Country for Cryogenic Insulation in South America Region

10.6.2 Argentina

10.6.2.1 Rising Demand From Energy & Power Segment to Support the Growth of Market in the Country

10.6.3 Venezuela

10.6.3.1 Rising Demand for Gas-Based Electricity Generation is Expected to Drive the Demand for Cryogenic Insulation in the Country

11 Competitive Landscape (Page No. - 111)

11.1 Introduction

11.2 Major Market Players

11.2.1 Armacell International Holding GmbH

11.2.2 Lydall Inc.

11.2.3 BASF SE

11.2.4 Cabot Corporation

11.2.5 Rochling Group

11.3 Competitive Scenarios

11.3.1 Agreement

11.3.2 New Product Launch

12 Company Profiles (Page No. - 114)

12.1 Armacell International Holding GmbH

12.1.1 Business Overview

12.1.2 Products Offered

12.1.3 SWOT Analysis

12.1.4 MnM View

12.2 Lydall Inc.

12.2.1 Business Overview

12.2.2 Products Offered

12.2.3 Recent Developments

12.2.4 SWOT Analysis

12.2.5 MnM View

12.3 BASF SE

12.3.1 Business Overview

12.3.2 Products Offered

12.3.3 SWOT Analysis

12.3.4 MnM View

12.4 Cabot Corporation

12.4.1 Business Overview

12.4.2 Products Offered

12.4.3 Recent Developments

12.4.4 SWOT Analysis

12.4.5 MnM View

12.5 Rochling Group

12.5.1 Business Overview

12.5.2 Products Offered

12.5.3 Recent Developments

12.5.4 SWOT Analysis

12.5.5 MnM View

12.6 Johns Manville Inc.

12.6.1 Business Overview

12.6.2 Products Offered

12.6.3 Recent Developments

12.7 Dunmore Corporation

12.7.1 Business Overview

12.7.2 Products Offered

12.8 Pittsburgh Corning Corporation

12.8.1 Business Overview

12.8.2 Products Offered

12.9 Imerys Minerals

12.9.1 Business Overview

12.9.2 Products Offered

12.9.3 Recent Developments

12.10 Aspen Aerogels

12.10.1 Business Overview

12.10.2 Products Offered

12.11 Isover (Saint Gobain)

12.11.1 Business Overview

12.11.2 Products Offered

12.12 Hertel

12.12.1 Business Overview

12.12.2 Products Offered

12.13 Amol Dicalite Limited

12.13.1 Business Overview

12.13.2 Products Offered

12.14 G+H Group

12.14.1 Business Overview

12.14.2 Products Offered

13 Appendix (Page No. - 136)

13.1 Insights From Industry Experts

13.2 Discussion Guide

13.3 Knowledge Store: Marketsandmarkets� Subscription Portal

13.4 Introducing RT: Real-Time Market Intelligence

13.5 Available Customizations

13.6 Related Reports

List of Tables (63 Tables)

Table 1 Trends and Forecast of GDP, 2017�2022 (USD Billion)

Table 2 Cryogenic Insulation Market Size, By Type, 2016�2023 (USD Million)

Table 3 Cryogenic Insulation Market Size for Pu & Pir, By Region, 2016-2023 (USD Million)

Table 4 Cryogenic Insulation Market Size for Cellular Glass, By Region, 2016-2023 (USD Million)

Table 5 Cryogenic Insulation Market Size for Polystyrene Foam, By Region, 2016-2023 (USD Million)

Table 6 Cryogenic Insulation Market for Fiberglass, By Region, 2016-2023 (USD Million)

Table 7 Cryogenic Insulation Market for Perlite, By Region, 2016-2023 (USD Million)

Table 8 Cryogenic Insualtion for Others, By Region, 2016-2023 (USD Million)

Table 9 Cryogenic Insulation Market Size, By Cryogenic Equipment, 2016�2023 (USD Million)

Table 10 By Market Size for Tanks, By Region, 2016-2023 (USD Million)

Table 11 By Market Size for Valves, By Region, 2016-2023 (USD Million)

Table 12 By Market Size for Vaporizer, By Region, 2016-2023 (USD Million)

Table 13 By Market for Pump, By Region, 2016-2023 (USD Million)

Table 14 By Market for Other Equipment, By Region, 2018-2023 (USD Million)

Table 15 By Market Size, By Form, 2016�2023 (USD Million)

Table 16 By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 17 By Market Size in Energy & Power, 2016�2023 (USD Million)

Table 18 By Market Size in Chemicals, By Region, 2016�2023 (USD Million)

Table 19 By Market Size in Metallurgical, By Region, 2016�2023 (USD Million)

Table 20 By Market Size in Electronics, By Region, 2016�2023 (USD Million)

Table 21 By Market Size in Shipping, By Region, 2016�2023 (USD Million)

Table 22 By Market Size in Other Industry, By Region, 2016�2023 (USD Million)

Table 23 By Market Size, By Region, 2016�2023 (USD Million)

Table 24 APAC: By Market Size, By Country, 2016�2023 (USD Million)

Table 25 APAC: By Market Size, By Type, 2016�2023 (USD Million)

Table 26 APAC: By Market Size, By Form, 2016�2023 (USD Million)

Table 27 APAC: By Market Size, By Cryogenic Equipment, 2016�2023 (USD Million)

Table 28 APAC: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 29 China: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 30 India: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 31 Australia: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 32 Japan: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 33 Malaysia: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 34 North America: By Market Size, By Country, 2016�2023 (USD Million)

Table 35 North America: By Market Size, By Type, 2016�2023 (USD Million)

Table 36 North America: By Market Size, By Form, 2016�2023 (USD Million)

Table 37 North America: By Market Size, By Cryogenic Equipment, 2016�2023 (USD Million)

Table 38 North America: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 39 US: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 40 Canada: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 41 Mexico: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 42 Europe: By Market Size, By Country, 2016�2023 (USD Million)

Table 43 Europe: By Market Size, By Type, 2016�2023 (USD Million)

Table 44 Europe: By Market Size, By Form, 2016�2023 (USD Million)

Table 45 Europe: By Market Size, By Cryogenic Equipment, 2016�2023 (USD Million)

Table 46 Europe: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 47 UK: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 48 Russia: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 49 France: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 50 Germany: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 51 Middle East & Africa: By Market Size, By Cryogenic Equipment, 2016�2023 (USD Million)

Table 52 Saudi Arabia: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 53 Qatar: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 54 UAE: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 55 South Africa: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 56 Nigeria: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 57 Algeria: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 58 South America: By Market Size, By Country, 2016�2023 (USD Million)

Table 59 Brazil: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 60 Argentina: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 61 Venezuela: By Market Size, By End-Use Industry, 2016�2023 (USD Million)

Table 62 Agreement, 2013�2017

Table 63 New Product Launch, 2013�2017

List of Figures (41 Figures)

Figure 1 Cryogenic Insulation Market Segmentation

Figure 2 Cryogenic Insulation Market: Research Design

Figure 3 Cryogenic Insulation Market: Data Triangulation

Figure 4 Pu & Pir to Dominate the Cryogenic Insulation Market

Figure 5 Energy & Power to Be the Leading End-Use Industry of Cryogenic Insulation

Figure 6 Tank Segment to Dominate the Cryogenic Insulation Market

Figure 7 APAC Dominated the Cryogenic Insulation Market in 2017

Figure 8 Increasing Demand for LNG to Drive the Cryogenic Insulation Market Between 2018 and 2023

Figure 9 China Accounted for the Largest Market Share in APAC

Figure 10 APAC Accounted for Largest Market Share in 2017

Figure 11 Energy & Power Segment Accounted for the Largest Market Share in Middle East & Africa in 2017

Figure 12 China to Be Fastest-Growing Market Between 2018 and 2023

Figure 13 Drivers, Opportunities, and Challenges in Cryogenic Insulation Market

Figure 14 Global Natural Gas Annual Production, 2012-2017 (Million Tonnes Oil Equivalent)

Figure 15 Cryogenic Insualtion Market: Porter�s Five Forces Analysis

Figure 16 Global Natural Gas Annual Production vs Consumption (Million Tonnes Oil Equivalent), 2011-2017

Figure 17 Global Natural Gas Annual Production, 2011-2017 (Million Tonnes Oil Equivalent)

Figure 18 Pu & Pir Segment to Dominate the Cryogenic Insulation Market Between 2018 and 2023

Figure 19 Tanks to Dominate the Cryogenic Insulation Market Between 2018 and 2023

Figure 20 Multi-Layer Segment to Dominate Between 2018 and 2023

Figure 21 Energy & Power Segment to Register Highest CAGR During Forecast Period

Figure 22 Middle East & Africa Market to Register Highest CAGR During the Forecast Period

Figure 23 APAC Cryogenic Insulation Market Snapshot

Figure 24 North American Cryogenic Insulation Market Snapshot

Figure 25 Europe Cryogenic Insulation Market Snapshot

Figure 26 Companies Adopted New Product Launches as the Key Growth Strategy Between 2013 and 2018

Figure 27 Armacell International Holding GmbH : Company Snapshot

Figure 28 Lydall Inc. : Company Snapshot

Figure 29 BASF SE : Company Snapshot

Figure 30 Cabot Corporation: Company Snapshot

Figure 31 Cabot Corporation: SWOT Analysis

Figure 32 Rochling Group : Company Snapshot

Figure 33 Johns Manville Inc.: Company Snapshot

Figure 34 Dunmore Corporation : Company Snapshot

Figure 35 Pittsburgh Corning Corporation: Company Snapshot

Figure 36 Imerys SA: Company Snapshot

Figure 37 Aspen Aerogels: Company Snapshot

Figure 38 Isover (Saint Gobain) : Company Snapshot

Figure 39 Hertel: Company Snapshot

Figure 40 Amol Dicalite Limited: Company Snapshot

Figure 41 G+H Group: Company Snapshot

Growth opportunities and latent adjacency in Cryogenic Insulation Market