Automotive ECU Market by Application, ECU Capacity (16-bit, 32-bit, 64 bit), Propulsion (BEVs, HEVs, ICE), Level of Autonomous Driving, Vehicle Type (LDV, HCV, Construction & Mining Equipment, Agricultural Tractors), and Region - Global Forecast to 2025

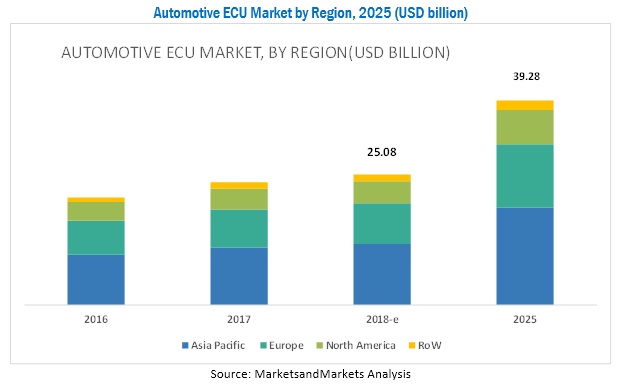

The automotive ECU market (Electronic Control Unit) was valued at USD 23.55 billion in 2017 and is projected to reach USD 39.28 billion by 2025, at a CAGR of 5.77% during the forecast period. The base year for the report is 2017 and the forecast period is 2018 to 2025.

Objectives of the report

- To define, segment, and forecast the market (2018–2025), in terms of volume (million units) and value (USD million)

- To provide detailed analysis of the various forces acting in the market (drivers, restraints, opportunities, and challenges)

- To segment the market and forecast the market size, by volume and value, based on application, ECU capacity, propulsion, level of autonomous driving, vehicle type, and region (Asia Pacific, Europe, North America, and the Rest of the World)

- To segment the market and forecast the market size, by volume and value, based on application—ADAS & safety system, body control & comfort system, infotainment & communication system, and powertrain system

- To segment the market and forecast the market size, by volume and value, based on ECU type— 16-bit ECU, 32-bit ECU, and 64-bit ECU

- To segment the market and forecast the market size, by volume and value, based on fuel type—BEVs, hybrid vehicles, and ICE vehicles

- To segment the market and forecast the market size, by volume and value, based on vehicle type—Light-duty vehicles, heavy commercial vehicles, construction & mining equipment, and agricultural tractors

- To segment the market and forecast the market size, by volume and value, based on the level of autonomous driving—autonomous, conventional, and semi-autonomous

- To track and analyze competitive developments such as joint ventures, mergers & acquisitions, new product launches, expansions, and other activities carried out by key industry participants

The research methodology used in the report involves primary and secondary sources and follows a bottom-up approach for the purpose of data triangulation. The study involves the country-level OEM and model-wise analysis of automotive ECU market. This analysis involves historical trends as well as existing market penetrations by country as well as vehicle type. The analysis is projected based on various factors such as growth trends in vehicle production and adoption rate by OEMs. The analysis has been discussed with and validated by primary respondents, which include experts from the automotive industry, manufacturers, and suppliers. Secondary sources include associations such as China Association of Automobile Manufacturers (CAAM), International Organization of Motor Vehicle Manufacturers (OICA), European Automobile Manufacturers Association (ACEA), Environmental Protection Agency (EPA), Society of Indian Automotive Manufacturers, SAE International, and paid databases and directories such as Factiva.

The figure below illustrates the break-up of the profile of industry experts who participated in primary discussions.

To know about the assumptions considered for the study, download the pdf brochure

The ecosystem of the Automotive ECU Market consists of automotive ECU manufacturers such as Continental (Germany), Bosch (Germany), Aptiv (UK), Denso (Japan), Autoliv (Sweden), Mitsubishi Electric (Japan), ZF (Germany), Hitachi (Japan), and Magneti Marelli (Italy). The automotive ECUs are supplied to the Tier 1 companies manufacturing electronic systems and automotive OEMs.

Target Audience

- Automotive ECU manufacturers

- Automotive cockpit electronics manufacturers

- Automotive powertrain manufacturers

- Automotive safety and comfort system manufacturers

- Industry associations

- Raw material suppliers for automotive ECU manufacturers

- The Automobile Industry as an end-user, traders, distributors, and suppliers of automotive ECUs

Scope of the Report

Market By Application

- ADAS & Safety System

- Body Control & Comfort System

- Infotainment & Communication System

- Powertrain System

Market By ECU Capacity

- 16-bit ECU

- 32-bit ECU

- 64-bit ECU

Market By Propulsion Type

- BEVs

- Hybrid Vehicles

- ICE Vehicles

Market By Level of Autonomous Driving

- Autonomous Vehicles

- Conventional Vehicles

- Semi-Autonomous Vehicles

Market By Vehicle Type

- Light-Duty Vehicles

- Heavy Commercial Vehicles

- Construction & Mining Equipment

- Agricultural Tractors

Market By Region

- Asia Pacific (China, India, Japan, South Korea, and Rest of Asia Pacific)

- Europe (Germany, France, Spain, UK, and Rest of Europe)

- North America (US, Mexico, and Canada)

- Rest of the World (Brazil, Iran and Others)

Available Customizations

With the given market data, MarketsandMarkets offers customizations in accordance with the company’s specific needs.

Market For Infotainment And Communication System, By Region

- Asia Pacific

- Europe

- North America

- Rest of the World

Market For Battery Electric Vehicles, By Region

- Asia Pacific

- Europe

- North America

- Rest of the World

The Automotive ECU Market (Electronic Control Unit) is projected to grow at a CAGR of 5.77% from 2018 to 2025. The market for automotive ECUs is estimated to be USD 25.08 billion in 2018 and is projected to reach USD 39.28 billion by 2025. The key growth drivers of this market are the increased incorporation of advanced safety, convenience, and comfort systems in vehicles and the increase in demand for hybrid electric vehicles (HEV) and battery electric vehicles (BEV).

The ADAS & safety system segment is estimated to hold the largest market share in the global market. The market growth in this segment can be attributed to the increasing number of government mandates for ADAS features and the inclusion of basic safety systems such as ABS, airbags, and TPMS.

The 64-bit ECU is estimated to be the fastest growing segment of market. Rising demand for advanced electronics such as windshield HUDs, camera modules, drive mode selector, RADAR, LiDAR, and advanced telematics that require fast and real-time processing is expected to drive the 64-bit ECU market.

By vehicle type, the light-duty vehicles segment is estimated to hold the largest market share of the market. Luxury light-duty vehicles use a large number of ECUs as these vehicles are equipped with advanced vehicle electronics functions for better comfort, convenience, and safety. Additionally, factors such as the sizeable number of luxury light-duty vehicles in Europe and North America and the increasing demand for these vehicles in the Asia Pacific region are increasing the demand for automotive ECUs. In the Asia Pacific region, the demand for luxury light-duty vehicles is growing due to the increasing purchasing power of consumers and the growing demand for comfort and safety features in a vehicle.

The automotive ECU market for Battery Electric Vehicles (BEVs) segment is estimated to grow at the highest rate during the forecast period. BEVs have many electric components and ECUs in the drivetrain, interior, and body. BEV manufacturers are also adopting advanced technologies to attract more customers.

Asia Pacific is estimated to dominate the ECU market for automotive, by volume as well as value. The growth of this market can be attributed to the increase in production and demand for passenger cars and electric vehicles. The increasing demand for advanced electronics in vehicles, growing purchasing power of the consumers, and rising consumer awareness for safety features in the developing countries are the key factors driving the market in the Asia Pacific region.

A key factor restraining the growth of the automotive ECU market is the increasing consumer preference for BYOD (Bring Your Own Device) and the approach of ECU consolidation. Unlike conventional cockpit electronics system, the BYOD technology eliminates the need for embedded display and infotainment systems in the vehicle. It also indirectly reduces the use of ECUs, which are required to run these technologies. In addition, OEMs are adopting BYOD technology as it is easy to use and helps to cut down the overall cost of the vehicle.

Some of the key market players are Continental (Germany), Bosch (Germany), Aptiv (UK), Denso (Japan), Autoliv (Sweden), Mitsubishi Electric (Japan), and Hitachi (Japan).

To speak to our analyst for a discussion on the above findings, click Speak to Analyst

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Table of Contents

1 Introduction (Page No. - 15)

1.1 Objectives of the Study

1.2 Automotive ECU Market Definition

1.3 Market Scope

1.3.1 Markets Covered

1.3.2 Years Considered for the Study

1.4 Currency

1.5 Package Size

1.6 Limitations

1.7 Stakeholders

2 Research Methodology (Page No. - 19)

2.1 Research Data

2.2 Secondary Data

2.3 Primary Data

2.3.1 Sampling Techniques & Data Collection Methods

2.3.2 Primary Participants

2.4 Data Triangulation

2.5 Factor Analysis

2.5.1 Introduction

2.5.2 Demand-Side Analysis

2.5.2.1 Growing Demand for Safety Features

2.5.2.2 Growth in Luxury Vehicle Sales

2.5.3 Supply-Side Analysis

2.5.3.1 Focus on Comfort and Convenience Features in Vehicles By Oems

2.5.3.2 Technological Advancements in the Automotive Industry

2.6 Automotive ECU Market Size Estimation

2.7 Assumptions

3 Executive Summary (Page No. - 30)

4 Premium Insights (Page No. - 36)

4.1 Attractive Opportunities in the Automotive ECU Market

4.2 Market, By Region

4.3 Market, By Country

4.4 Market, By Level of Autonomous Driving

4.5 Market, By Vehicle Type

4.6 Market, By Propulsion

4.7 Market, By Application

4.8 Market, By ECU Capacity

5 Automotive ECU Market Overview (Page No. - 42)

5.1 Market Dynamics

5.1.1 Drivers

5.1.1.1 Increased Incorporation of Advanced Safety, Convenience, and Comfort Systems

5.1.1.2 Growing Demand for Electric Vehicles

5.1.2 Restraints

5.1.2.1 Increasing Consumer Preference for Byod

5.1.2.2 Operation Failure in ECUs

5.1.3 Opportunities

5.1.3.1 Advent of Concept Cars and Autonomous Vehicles

5.1.3.2 Increasing Rate of Installation of Advanced Applications in Luxury and Mid-Range Vehicles

5.1.4 Challenges

5.1.4.1 Growing Trend of ECU Consolidation

5.1.4.2 Cost and Quality Trade-Off in the Manufacture of ECUs

6 Technological Overview (Page No. - 49)

6.1 Introduction

6.2 Automotive ECU Market: Market Segmentation

6.2.1 ADAS & Safety System

6.2.2 Body Control & Comfort System

6.2.3 Infotainment & Communication System

6.2.4 Powertrain System

7 Market, By Application (Page No. - 53)

7.1 Introduction

7.2 ADAS & Safety System

7.3 Body Control & Comfort System

7.4 Infotainment & Communication System

7.5 Powertrain System

8 Automotive ECU Market, By Propulsion Type (Page No. - 60)

8.1 Introduction

8.2 BEVS

8.3 Hybrid Vehicles

8.4 ICE Vehicles

9 Market, By ECU Capacity (Page No. - 67)

9.1 Introduction

9.2 16-Bit ECU

9.3 32-Bit ECU

9.4 64-Bit ECU

10 Automotive ECU Market, By Level of Autonomous Driving (Page No. - 73)

10.1 Introduction

10.2 Autonomous Vehicles

10.3 Conventional Vehicles

10.4 Semi-Autonomous Vehicles

11 Market, By Vehicle Type

11.1 Introduction

11.2 Light Duty Vehicles

11.3 Heavy Commercial Vehicles

11.4 Construction and Mining Equipment

11.5 Agricultural Tractor

12 Automotive ECU Market, By Vehicle Type & Region (Page No. - 80)

12.1 Introduction

12.2 Asia Pacific

12.2.1 China

12.2.2 India

12.2.3 Japan

12.2.4 South Korea

12.2.5 Rest of Asia Pacific

12.3 Europe

12.3.1 France

12.3.2 Germany

12.3.3 Italy

12.3.4 UK

12.3.5 Rest of Europe

12.4 North America

12.4.1 Canada

12.4.2 Mexico

12.4.3 US

12.5 Rest of the World

12.5.1 Brazil

12.5.2 Russia

12.5.3 South Africa

13 Competitive Landscape (Page No. - 114)

13.1 Overview

13.2 Automotive ECU Market Ranking Analysis

13.3 Competitive Situation & Trends

13.3.1 New Product Developments

13.3.2 Expansions

13.3.3 Partnerships/Supply Contracts/Collaborations/Joint Ventures/Agreements/Mergers & Acquisitions

14 Company Profiles (Page No. - 120)

(Business Overview, Products Offered, Recent Developments, SWOT Analysis, MnM View)*

14.1 Continental

14.2 Bosch

14.3 Aptiv

14.4 Denso Corporation

14.5 Autoliv

14.6 Mitsubishi Electric

14.7 Magneti Marelli

14.8 ZF

14.9 Hitachi

14.10 Lear

*Details on Business Overview, Products Offered, Recent Developments, SWOT Analysis, MnM View Might Not Be Captured in Case of Unlisted Companies.

15 Appendix (Page No. - 152)

15.1 Insights of Industry Experts

15.2 Discussion Guide

15.3 Knowledge Store: Marketsandmarkets’ Subscription Portal

15.4 Introducing RT: Real Time Market Intelligence

15.5 Available Customizations

15.5.1 Automotive ECU Market for Infotainment and Communication System, By Region and Country

15.5.1.1 Asia Pacific

15.5.1.2 Europe

15.5.1.3 North America

15.5.1.4 Rest of the World

15.5.2 Automotive ECU Market for Battery Electric Vehicles, By Region and Country

15.5.2.1 Asia Pacific

15.5.2.2 Europe

15.5.2.3 North America

15.5.2.4 Rest of the World

15.6 Related Reports

15.7 Author Details

List of Tables (91 Tables)

Table 1 Currency Exchange Rates (Wrt USD)

Table 2 Regulations for Driving Assistance Safety Systems

Table 3 Automotive ECU Market Size, By Application, 2015–2025 (Million Units)

Table 4 Market Size, By Application, 2015–2025 (USD Million)

Table 5 ADAS & Safety System: Market Size, By Region, 2015–2025 (Million Units)

Table 6 ADAS & Safety System: Market Size, By Region, 2015–2025 (USD Million)

Table 7 Body Control & Comfort System: Market Size, By Region, 2015–2025 (Million Units)

Table 8 Body Control & Comfort System: Market Size, By Region, 2015–2025 (USD Million)

Table 9 Infotainment & Communication System: Market Size, By Region, 2015–2025 (Million Units)

Table 10 Infotainment & Communication System: Market Size, By Region, 2015–2025 (USD Million)

Table 11 Powertrain System: Market Size, By Region, 2015–2025 (Million Units)

Table 12 Powertrain System: Market Size, By Region, 2015–2025 (USD Million)

Table 13 Market Size, By Propulsion Type, 2015–2025 (Million Units)

Table 14 Market Size, By Propulsion Type, 2015–2025 (USD Million)

Table 15 BEVS: Market Size, By Region, 2015–2025 (Million Units)

Table 16 BEVS: Market Size, By Region, 2015–2025 (USD Million)

Table 17 HEVS: Market Size, By Region, 2015–2025 (Million Units)

Table 18 HEVS: Market Size, By Region, 2015–2025 (USD Million)

Table 19 ICE Vehicles: Market Size, By Region, 2015–2025 (Million Units)

Table 20 ICE Vehicles: Market Size, By Region, 2015–2025 (USD Million)

Table 21 Market Size, By Capacity, 2015–2025 (Million Units)

Table 22 Market Size, By Capacity, 2015–2025 (USD Million)

Table 23 16-Bit ECU: Market Size, By Region, 2015–2020 (Million Units)

Table 24 16-Bit ECU: Market Size, By Region, 2015–2020 (USD Million)

Table 25 32-Bit ECU: Market Size, By Region, 2015–2025 (Million Units)

Table 26 32-Bit ECU: Market Size, By Region, 2015–2025 (USD Million)

Table 27 64-Bit ECU: Market Size, By Region, 2015–2025 (Million Units)

Table 28 64-Bit ECU: Market Size, By Region, 2015–2025 (USD Million)

Table 29 Market Size, By Level of Autonomous Driving, 2015–2025 (Million Units)

Table 30 Market Size, By Level of Autonomous Driving, 2015–2025 (USD Million)

Table 31 Autonomous Vehicles: Market Size, By Region, 2022–2025 (Million Units)

Table 32 Autonomous Vehicles: Market Size, By Region, 2015–2025 (USD Million)

Table 33 Conventional Vehicles: Market Size, By Region, 2015–2025 (Million Units)

Table 34 Conventional Vehicles: Market Size, By Region, 2015–2025 (USD Million)

Table 35 Semi-Autonomous Vehicles: Market Size, By Region, 2015–2025 (Million Units)

Table 36 Semi-Autonomous Vehicles: Market Size, By Region, 2015–2025 (USD Million)

Table 37 Market Size, By Region, 2015–2025 (Million Units)

Table 38 Market Size, By Region, 2015–2025 (USD Million)

Table 39 Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 40 Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 41 Asia Pacific: Market Size, By Country, 2015–2025 (Million Units)

Table 42 Asia Pacific: Market Size, By Country, 2015–2025 (USD Million)

Table 43 Asia Pacific: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 44 Asia Pacific: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 45 China: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 46 China: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 47 India: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 48 India: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 49 Japan: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 50 Japan: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 51 South Korea: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 52 South Korea: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 53 Rest of Asia Pacific: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 54 Rest of Asia Pacific: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 55 Europe: Market Size, By Country, 2015–2025 (Million Units)

Table 56 Europe: Market Size, By Country, 2015–2025 (USD Million)

Table 57 Europe: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 58 Europe: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 59 France: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 60 France: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 61 Germany: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 62 Germany: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 63 Italy: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 64 Italy: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 65 UK: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 66 UK: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 67 Rest of Europe: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 68 Rest of Europe: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 69 North America: Market Size, By Country, 2015–2025 (Million Units)

Table 70 North America: Market Size, By Country, 2015–2025 (USD Million)

Table 71 North America: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 72 North America: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 73 Canada: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 74 Canada: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 75 Mexico: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 76 Mexico: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 77 US: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 78 US: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 79 RoW: Market Size, By Country, 2015–2025 (Million Units)

Table 80 RoW: Market Size, By Country, 2015–2025 (USD Million)

Table 81 RoW: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 82 RoW: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 83 Brazil: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 84 Brazil: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 85 Russia: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 86 Russia: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 87 South Africa: Market Size, By Vehicle Type, 2015–2025 (Million Units)

Table 88 South Africa: Market Size, By Vehicle Type, 2015–2025 (USD Million)

Table 89 New Product Developments, 2015–2018

Table 90 Expansions, 2016–2018

Table 91 Partnerships/Supply Contracts/Collaborations/Joint Ventures/Agreements/Mergers & Acquisitions, 2016–2018

List of Figures (55 Figures)

Figure 1 Automotive ECU Market: Segmentations Covered

Figure 2 Research Design

Figure 3 Research Methodology Model

Figure 4 Breakdown of Primary Interviews: By Company Type, Designation, & Region

Figure 5 Luxury Vehicle Y-O-Y Sales Growth (2011–2016)

Figure 6 Market: Bottom-Up Approach

Figure 7 Market: Top-Down Approach

Figure 8 ADAS & Safety System Segment to Drive the Growth of the Automotive ECU Market, 2017 vs 2025 (USD Billion)

Figure 9 Conventional Vehicle Segment to Be the Largest Contributor to the Market, 2017 vs 2025 (USD Billion)

Figure 10 32-Bit System to Be the Largest Segment of the Market, 2017 vs 2025 (USD Billion)

Figure 11 Light Duty Vehicles Segment to Be the Largest Contributor to the Market, 2017 vs 2025 (USD Million)

Figure 12 Asia Pacific to Hold the Largest Share of the Market, 2017 vs 2025 (USD Billion)

Figure 13 Increasing Adoption of Advanced Vehicle Electronics to Drive the Market in the Next 8 Years

Figure 14 Asia Pacific to Hold the Largest Share of Market, 2017 vs 2025 (By Value)

Figure 15 The Chinese Market is Expected to Grow at the Highest CAGR During the Forecast Period (By Value)

Figure 16 Conventional Vehicles are Expected to Hold the Largest Share of Market, 2017 vs 2025 (By Value)

Figure 17 Light Duty Vehicles to Hold the Largest Market Share, 2017 vs 2025 (By Value)

Figure 18 ICE Vehicles Segment is Estimated to Lead the Market During the Forecast Period (By Value)

Figure 19 ADAS and Safety System is Estimated to Have the Largest Market Size, 2017 vs 2025 (By Value)

Figure 20 32-Bit ECU to Have the Largest Market Size, 2017 vs 2025 (By Value)

Figure 21 Automotive ECU: Market Dynamics

Figure 22 BEV Sales in Major Regions, 2017 vs 2022 (Thousand Units)

Figure 23 Adoption Trend of Autonomous Vehicles

Figure 24 ECU Consolidation Evolution

Figure 25 Technological Evolution of Automotive ECU Applications

Figure 26 Major Automotive ECU Application Areas

Figure 27 Market, By Application

Figure 28 Market, By Application, 2017 vs 2025 (USD Billion)

Figure 29 Market, By Propulsion Type, 2017 vs 2025 (USD Million)

Figure 30 Market, By Capacity, 2017 vs 2025 (Million Units)

Figure 31 Levels of Autonomous Driving

Figure 32 Market, By Level of Autonomous Driving, 2017 vs 2025 (USD Million)

Figure 33 Market, By Region, 2017 vs 2025

Figure 34 Market, By Vehicle Type, 2017 vs 2025

Figure 35 Asia Pacific: Market Snapshot

Figure 36 Europe: Market, By Country, 2017 vs 2025 (Million Units)

Figure 37 North America: Market Snapshot

Figure 38 RoW: Market Size, By Country, 2017 vs 2025 (Million Units)

Figure 39 Key Developments By Leading Players in the Market, 2015–2018

Figure 40 Market Ranking: 2017

Figure 41 Continental: Company Snapshot

Figure 42 SWOT Analysis: Continental

Figure 43 Bosch: Company Snapshot

Figure 44 SWOT Analysis: Bosch

Figure 45 Aptiv: Company Snapshot

Figure 46 SWOT Analysis: Aptiv

Figure 47 Denso Corporation: Company Snapshot

Figure 48 SWOT Analysis: Denso

Figure 49 Autoliv: Company Snapshot

Figure 50 SWOT Analysis: Autoliv

Figure 51 Company Snapshot: Mitsubishi Electric

Figure 52 Magneti Marelli: Company Snapshot

Figure 53 ZF: Company Snapshot

Figure 54 Hitachi: Company Snapshot

Figure 55 Lear: Company Snapshot

Growth opportunities and latent adjacency in Automotive ECU Market