Semiconductor Industry M&A Analysis and Future Trends � by Acquirer Type (IDM, Fabless, Foundry), Deal Value, End-User, and Region

Mergers and acquisitions in the semiconductor industry have picked up, both in terms of number of deals as well as deal size. The analysis of many Semiconductor M&A deals reveal that major semiconductor players are looking for companies that have lower operating expenses as compared to their growth potential. Major players target small to mid-sized companies that lack the scale to grow. The semiconductor industry saw record breaking mergers and acquisitions in the year 2015, with total value of the deals crossing USD 120 Billion. M&A’s play a very important role in the pursuit of growth for semiconductor companies. With the pool of M&A targets ever shrinking, the report will help semiconductor companies to maximize growth opportunities by taking the correct M&A decisions.

MarketsandMarkets analyzed the significant number of Semiconductor M&A deals in the semiconductor industry during 2014–2015 with the total value of deals to cross USD 120 Billion in 2015 itself. Semiconductor companies have found it necessary to increase their scale of operations to ensure they can provide their customers with the required products and services. The scale refers to both production capacity as well as human resources in the required areas. As the semiconductor manufacturing technology has advanced, the cost of manufacturing equipment has also increased significantly. Thus, the fixed costs associated with developing a chip have increased. These factors have led to an increase in the number of semiconductor M&A deals.

The report categorizes the Semiconductor M&A deals in semiconductor industry during 2014–2015 by deal value, acquirer type, end user, and region. In the current industry scenario, major players are looking to effectively use the big deal strategy to grow their market share in a competitive Semiconductor M&A environment. Growing organically by improving existing business portfolio and making only small selective acquisitions is a growth strategy that was preferred by players in the semiconductor M&A. However, the current market scenario makes this strategy less beneficial for medium-and large-sized semiconductor companies operating in the maturing industry segments. Some of the big ticket deals announced during 2014–2015 were: acquisition of Broadcom Corporation (U.S.) by Avago Technologies Ltd (U.S.), acquisition CSR plc (U.K.) by Qualcomm Inc. (U.S.), acquisition of Altera Corporation (U.S.) by Intel Corporation (U.S.), acquisition of Freescale Semiconductor Ltd (U.S.) by NXP Semiconductors NV (Netherlands), acquisition of Atmel Corporation (U.S.) by Dialog Semiconductor PLC (U.K.), and acquisition of SanDisk Corporation (U.S.) by Western Digital Corporation (U.S.), among others.

A key requirement for a successful Semiconductor M&A deal in semiconductor industry is identifying the acquisition target. The process of identifying acquisition targets should take place with a complete strategic review of the acquirer to identify key value drivers of the business and establishing a set of strategic goals. Semiconductor companies that serve maturing end user segments should target companies that can help them sustain the industry pricing pressures, improve profitability, and increase their market share.

North American companies, more specifically U.S. companies were highly active in the semiconductor M&A landscape. A majority of the acquirers and the acquirees were based in North America. In the APAC region, China bolstered its semiconductor acquisition with aggressive M&A activity.

One of major difficulties in merger and acquisition deals in semiconductor M&A is the post transaction process. It takes significant time and human resources to combine the resources of two companies to function as a single unit. This problem intensifies when the Semiconductor M&A involves two tier I companies. Issues such as tying the employee policies of the two companies to combining together the financial reporting systems of the two companies which may have different filling dates and use different systems can consume a lot of effort from the company management and hence hampers the overall company productivity.

The companies such as Intel Corporation (U.S.), Broadcom Corporation (U.S.), Qualcomm Incorporated (U.S.), Mediatek, Inc. (Taiwan), Avago Technologies Ltd (U.S.), SK Hynix, Inc. (South Korea), Micron Technology, Inc. (U.S.), Samsung Electronics Co., Ltd (South Korea), Taiwan Semiconductor Manufacturing Co., Ltd (Taiwan), and GLOBALFOUNDRIES Inc. (U.S.) have adopted various strategies such as partnerships, agreements, contracts, mergers and acquisitions, and new product developments to achieve business growth.

To speak to our analyst for a discussion on the above findings, click Speak to Analyst

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Table of Contents

1 Introduction (Page No. - 13)

1.1 Objectives of the Study

1.2 Industry Definition

1.3 Study Scope

1.3.1 Segmentation of M&A Deals

1.3.2 Years Considered for the Study

1.4 Currency & Pricing

1.5 Limitations

1.6 Stakeholders

2 Research Methodology (Page No. - 17)

2.1 Research Data

2.1.1 Secondary Data

2.1.1.1 Key Data From Secondary Sources

2.1.2 Primary Data

2.1.2.1 Key Data From Primary Sources

2.1.2.2 Key Industry Insights

2.1.2.3 Breakdown of Primaries

2.1.3 Bottom-Up Approach

2.1.4 Top-Down Approach

2.2 Data Analysis & Triangulation

2.3 Research Assumptions

3 Executive Summary (Page No. - 26)

4 Premium Insights (Page No. - 31)

4.1 Significant Growth in Semiconductor M&A Activities in 2015

4.2 Semiconductor M&A – Deal Values

4.3 semiconductor M&A – Deal Volumes

4.4 Big Ticket Deals From 2011–2015

4.5 Strategy Roadmap

4.6 Analysis of Billion Dollar M&A Deals 2014–2015

5 Market Overview (Page No. - 35)

5.1 Introduction

5.2 Evolution

5.3 Semiconductor Industry M&A Deals Classification

5.3.1 Semiconductor M&A Deals, By Acquirer Type

5.3.2 Semiconductor M&A Deals, By Deal Value

5.3.3 Semiconductor M&A Deals, By End User

5.3.4 Semiconductor M&A Deals, By Geography

5.4 Market Dynamics

5.4.1 Drivers

5.4.1.1 Need to Increase Scale

5.4.1.2 Increasing Cost of Chip Manufacturing

5.4.1.3 Intense Industry Competition

5.4.1.4 Improving Technology, Product , and Services Portfolio

5.4.2 Restraints

5.4.2.1 Difficulty in Combining Resources and Integrating Them in A Single Company

5.4.2.2 Lengthy Regulatory Approval Cycles

5.4.3 Opportunities

5.4.3.1 Chip Demand Expected to Be Driven By Internet of Things (IoT)

5.4.3.2 Growth of Mobile Devices

5.4.4 Challenges

5.4.4.1 Decreasing Asp of Semiconductor Chips

5.4.5 Key Success Factor

5.4.5.1 Providing Comprehensive System Solutions

6 Industry Trends (Page No. - 47)

6.1 Introduction

6.2 Value Chain Analysis

6.3 Key Influencers

6.4 Porter’s Five Forces Analysis

6.4.1 Intensity of Rivalry

6.4.2 Threat of Substitutes

6.4.3 Bargaining Power of Buyers

6.4.4 Bargaining Power of Suppliers

6.4.5 Threat of New Entrants

6.5 Key Trends

6.5.1 Increasing Chip Complexity

6.5.2 Shift Towards Smart Devices and Connectivity

7 Review of Key Industry Segments (Page No. - 57)

7.1 Introduction

7.2 Semiconductor Component Market Review

7.3 Semiconductor Market-Geographic Review

7.4 Semiconductor M&A Market-End User Segment Review

7.4.1 Data Processing

7.4.2 Communications

7.4.3 Consumer Electronics

7.4.4 Automotive Electronics

7.4.5 Industrial Electronics

8 Mergers & Acquisitions (Page No. - 64)

8.1 Introduction

8.2 semiconductor M&A, By Deal Value

8.3 semiconductor M&A, By Acquirer Type

8.3.1 IDM

8.3.2 Fabless

8.3.3 Foundry

8.4 Semiconductor M&A, By Region

8.5 Semiconductor M&A, By End User

8.6 Review of Key Mergers and Acquisitions (2011–2015)

8.6.1 Avago Technologies Ltd Acquires Broadcom Corporation

8.6.2 Avago Technologies Ltd Acquires LSI Corporation

8.6.3 Qualcomm Inc. Acquires CSR PLC

8.6.4 Intel Corporation Acquires Altera Corporation

8.6.5 NXP Semiconductors Nv Acquires Freescale Semiconductor Ltd

8.6.6 Dialog Semiconductor PLC Acquires Atmel Corporation

8.6.7 Western Digital Corporation Acquires Sandisk Corporation

8.6.8 on Semiconductor Corp. Acquires Fairchild Semiconductor International Inc.

8.6.9 Lattice Semiconductor Corporation Acquires Silicon Image, Inc.

8.6.10 Cypress Semiconductor Corporation Acquires Spansion Inc.

9 Future Industry Roadmap (Page No. - 83)

9.1 Introduction

9.2 Semiconductor M&A Trends in the Semiconductor Industry

9.3 Key semiconductor M&A Strategies

9.3.1 Post-Merger Integration

9.3.2 Identification of Acquisition Targets

9.4 Potential Acquisition Targets

9.4.1 Xilinx, Inc.

9.4.2 Maxim Integrated Products, Inc.

9.4.3 Micron Technology, Inc.

9.4.4 Renesas Electronics Corporation

9.4.5 Cavium, Inc.

9.4.6 Lattice Semiconductor Corporation

9.4.7 Advanced Micro Devices, Inc. (AMD)

9.4.8 Skyworks Solutions, Inc.

9.4.9 Marvell Technology Group Ltd.

9.4.10 Nvidia Corporation

10 Competitive Landscape (Page No. - 97)

10.1 Overview

10.2 Market Rankings, semiconductor M&A

10.3 Competitive Situation and Trends

10.3.1 New Product Development/New Product Launch

10.3.2 Partnerships, Agreements, Alliances, and Collaborations

10.3.3 Acquisitions and Expansions

10.3.4 Other Developments

11 Company Profiles (Page No. - 105)

(Overview, Products and Services, Financials, Strategy & Development)*

11.1 Intel Corporation

11.2 Broadcom Corporation

11.3 Qualcomm Incorporated

11.4 Mediatek, Inc.

11.5 Avago Technologies Limited

11.6 SK Hynix, Inc.

11.7 Micron Technology, Inc.

11.8 Samsung Electronics Co., Ltd.

11.9 Taiwan Semiconductor Manufacturing Co., Ltd.

11.10 Globalfoundries Inc

*Details on Overview, Products and Sebrvices, Financials, Strategy & Development Might Not Be Captured in Case of Unlisted Companies.

12 Appendix (Page No. - 154)

12.1 Insights of Industry Experts

12.2 Discussion Guide

12.3 Introducing RT: Real-Time Market Intelligence

12.4 Available Customizations

12.5 Related Reports

List of Tables (11 Tables)

Table 1 Semiconductor Industry M&A Deals Classification: By Acquirer Type

Table 2 Increasing Cost of Chip Manufacturing Act as A Major Driver for Semiconductor M&A Deals

Table 3 Lengthy Regulatory Approval Cycle Restraining the Number of Semiconductor M&A Deals

Table 4 Internet of Things is an Exciting Growth Opportunity

Table 5 Decreasing Asp of Semiconductor Chips is A Major Challenge for Growth in the Semiconductor Market

Table 6 Semiconductor M&A : Key Player Ranking Analysis, 2014

Table 7 Semiconductor M&A: Market Rankings, By Key Player, 2014

Table 8 New Product Developments/New Product Launches, 2014–2015

Table 9 Partnerships, Agreements, Alliances, and Collaborations 2014–2015

Table 10 Acquisitions, 2014–2015

Table 11 Other Developments, 2014–2015

List of Figures (86 Figures)

Figure 1 Merger and Acquisition Deals Classification

Figure 2 Research Design

Figure 3 Research Flow

Figure 4 Bottom-Up Approach

Figure 5 Top-Down Approach

Figure 6 Data Triangulation

Figure 7 Semiconductor M&A to Grow at A Sluggish Pace Between 2015 and 2020

Figure 8 Automotive Electronics is Expected to Grow at the Highest Rate During the Forecast Period

Figure 9 Companies in the North America Were Most Active in M&A Activities

Figure 10 Consolidation in the Semiconductor M&A Driven By Increasing Chip Manufacturing Cost

Figure 11 Low Interest Rates Have Made M&A an Attractive Strategy in 2015

Figure 12 Average Value of Semiconductor M&A Deals Increased in 2015

Figure 13 Avago-Broadcomm is the Biggest Deal in Semiconductor M&A History

Figure 14 Strategy Roadmap of Companies Depended on the End User Verticals

Figure 15 The Communications End User Segment Was Impacted By the Highest Number of Billion Dollar Deals

Figure 16 Evolution of the semiconductor M&A

Figure 17 semiconductor M&A Deals Classification: By Deal Value

Figure 18 semiconductor M&A Deals Classification: By End User

Figure 19 semiconductor M&A Deals Classification: By Geography

Figure 20 Increasing Cost of Chip Manufacturing is Driving Semiconductor Companies to Grow Via Merger and Acquisition Deals

Figure 21 Value Chain Analysis: Major Value Added During the R&D and Manufacturing Phase

Figure 22 Porter’s Five Forces Analysis, 2014

Figure 23 Porter’s Five Forces Analysis,2014

Figure 24 M&A in Semiconductor Industry and Future Industry Roadmap: Intensity of Rivalry

Figure 25 Semiconductor M&A and Future Industry Roadmap: Threat of Substitutes

Figure 26 Semiconductor M&A and Future Industry Roadway: Bargaining Power of Buyers

Figure 27 Semiconductor M&A and Future Industry Roadmap: Bargaining Power of Suppliers

Figure 28 M&A in Semiconductor Industry and Future Industry Roadmap: Threat of New Entrants

Figure 29 Semiconductor Market Expected to Experience A Steady Growth

Figure 30 Logic Segment to Dominate the Semiconductor Component Market

Figure 31 Sensors and Actuators Segment to Grow at the Highest Rate Between 2015 and 2020

Figure 32 China Held the Largest Market for the semiconductor M&A in 2014

Figure 33 China’s Semiconductor Consumption Growth has Outpaced Every Region

Figure 34 Data Processing Segment to Dominate the Semiconductor Market

Figure 35 Number of Big Ticket Deals Increased in 2014–2015

Figure 36 IDM and Fabless Semiconductor Companies Accounted for Majority of the M&A Deals During 2014 and 2015

Figure 37 Companies in North America Have Undergone Highest Number of Semiconductor M&A Deals Between 2014 and 2015

Figure 38 The Communications End User Segment Was Majorly Impacted By Semiconductor M&A Deals During 2014 and 2015

Figure 39 Avago’s Product Portfolio Expected to Significantly Increase Post Broadcom Acquisition

Figure 40 Avago’s Market Share to Grow in the Communications IC Market

Figure 41 LSI ’S Product Portfolio Before Avago Acquisition

Figure 42 Industry Solutions Offered By CSR PLC

Figure 43 Altera Corporation Product Portfolio

Figure 44 NXP-Freescale Combination Makes A Strong Company in the semiconductor M&A

Figure 45 NXP-Freescale Combination to Hold the Largest Share in the Automotive semiconductor M&A Based on 2014 Segment Revenues

Figure 46 Atmel Acquisition Expected to Help Dialog Diversify Its Customer Base

Figure 47 Atmel Acquisition Expected to Help Dialog Build A Comprehensive IoT Platform

Figure 48 Sandisk Acquisition Would Help Western Digital to Reduce Its Dependence on HDD Sales

Figure 49 Sandisk Acquisition to Help Western Digital to Get A Strong Foothold in the Ssd Market

Figure 50 Fairchild Semiconductor Product Portfolio Encompasses A Wide Range of Semiconductor Products

Figure 51 Acquiring Silicon Image Would Help Lattice Semiconductor to Expand Its Presence in Consumer, Communications, and Industrial Segments

Figure 52 Spansion Inc. Product Portfolio

Figure 53 Number of Deals Worth 500 Million Each Or Less Dominated the Semiconductor Industry Landscape Between 2000 and 2010

Figure 54 Breakdown of Deals Worth Below 500 Million Category Between 2000 and 2010

Figure 55 Xilinx, Inc.: Company Snapshot

Figure 56 Maxim Integrated Products, Inc.: Company Snapshot

Figure 57 Micron Technology, Inc.: Company Snapshot

Figure 58 Renesas Electronics Corporation: Company Snapshot

Figure 59 Cavium, Inc.: Company Snapshot

Figure 60 Lattice Semiconductor Corporation: Company Snapshot

Figure 61 Advanced Micro Devices, Inc.: Company Snapshot

Figure 62 Skyworks Solutions, Inc.: Company Snapshot

Figure 63 Marvell Technology Group Ltd.: Company Snapshot

Figure 64 Nvidia Corporation: Company Snapshot

Figure 65 Acquisitions and New Product Developments Were Key Growth Strategies During 2011–2015

Figure 66 Qualcomm Grew at the Highest Growth Rate Between 2010 and 2014

Figure 67 Battle for Market Share: New Product Launches/New Product Developments Drive Competitive Trends

Figure 68 Intel Corporation.: Company Snapshot

Figure 69 Intel Corporation: SWOT Analysis

Figure 70 Broadcom Corporation: Company Snapshot

Figure 71 Broadcom Corporation: SWOT Analysis

Figure 72 Qualcomm Incorporated.: Company Snapshot

Figure 73 Qualcomm Incorporated: SWOT Analysis

Figure 74 Mediatek,Inc.: Company Snapshot

Figure 75 Mediatek, Inc.: SWOT Analysis

Figure 76 Avago Technologies Limited: Company Snapshot

Figure 77 Avago Technologies Limited: SWOT Analysis

Figure 78 SK Hynix, Inc.: Company Snapshot

Figure 79 SK Hynix, Inc.: SWOT Analysis

Figure 80 Micron Technology, Inc.: Company Snapshot

Figure 81 Micron Technology, Inc.: SWOT Analysis

Figure 82 Samsung Electronics Co., Ltd.: Company Snapshot

Figure 83 Samsung Electronics Co., Ltd.: SWOT Analysis

Figure 84 Taiwan Semiconductor Manufacturing Co., Ltd.: Company Snapshot

Figure 85 Taiwan Semiconductor Manufacturing Co., Ltd.: SWOT Analysis

Figure 86 Global Foundries Inc: SWOT Analysis

The research methodology used to estimate and forecast the global semiconductor market begins with capturing data on key vendor revenues through secondary research. The vendor offerings are also taken into consideration to determine the market segmentation. The bottom-up procedure was employed to arrive at the overall market size of the global semiconductor market from the revenue of the key players in the market. After arriving at the overall market size, the total market was split into several segments and sub-segments which are then verified through primary research by conducting extensive interviews with key industry people - CEOs, VPs, Directors and executives. This data triangulation and market breakdown procedures were employed to complete the overall market engineering process and arrive at the exact statistics for all segments and sub-segments. The analysis of the Semiconductor M&A deals in semiconductor industry includes extensive primary research to gather information and verify and validate the critical conclusions arrived at after an extensive secondary research.

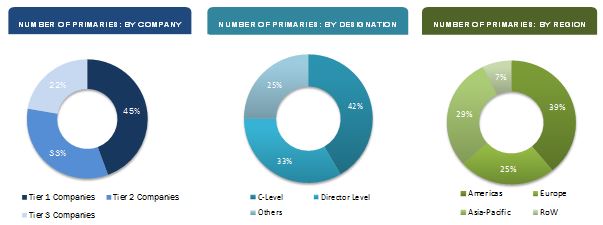

The breakdown of profiles of primary is depicted in the below figure:

To know about the assumptions considered for the study, download the pdf brochure

The top players in the semiconductor industry among integrated device manufacturers (IDMs), fabless semiconductor companies, and semiconductor foundries covered in this report include Intel Corporation (U.S.), Broadcom Corporation (U.S.), Qualcomm Incorporated (U.S.), Mediatek, Inc. (Taiwan), Avago Technologies Ltd (U.S.), SK Hynix, Inc. (South Korea), Micron Technology, Inc. (U.S.), Samsung Electronics Co., Ltd (South Korea), Taiwan Semiconductor Manufacturing Co., Ltd (Taiwan), and GLOBALFOUNDRIES Inc. (U.S.) have been profiled in the study.

Key Target Audience

- IDMs, fabless semiconductor companies, semiconductor foundries

- Distributors and retailers

- Technology investors

- Commercial banks

- Government and financial institutions

- Research organizations and consulting companies

- Semiconductor industry related associations, organizations, forums,and alliances

Scope of the Report

The research report segments merger and acquisition deals in the semiconductor market during the period 2014-2015 in to following categories:

By Deal Value:

- Less than USD 100 million

- USD 100 million to USD 500 million

- More than USD 500 million

- Others

By Acquirer Type:

- IDM

- Fabless

- Foundry

By End User:

- Automotive Electronics

- Communications

- Consumer Electronics

- Industrial Electronics

- Data Processing

By Region:

- North America

- Europe

- Asia-Pacific (APAC)

- Rest of the World (RoW)

Available Customizations

With the given market data, MarketsandMarkets offers customizations as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

- Product matrix which gives a detailed comparison of product portfolio of top companies

Custom M&A Analysis

- Analysis of Semiconductor M&A deals not covered in the study orexpected to happen in the near future

Company Information

- Detailed analysis and profiling of additional market players (Up to 5)

Growth opportunities and latent adjacency in Semiconductor Industry M&A Analysis and Future Trends