Optical Transport Network Market by Technology (WDM, DWDM), by Components (Optical Switch, Optical Packet Platform), by Services (Network Design, Network Support), by End User, by Regions - Worldwide Market Forecast and Analysis (2014 - 2019)

[146 Pages Report] The global optical transport network market size was USD 11.35 billion in 2014 and is projected to reach USD 23.64 billion by 2019, growing at a Compound Annual Growth Rate (CAGR) of 15.8% during the forecast period.

The sudden surge in the internet home users and business users have unfolded a new level of bandwidth requirement over the network world. There has been a significant adoption among residential customers because of the increased use of online gaming, social media, video chatting, and many other real time streaming events. The fact that offers seamless data transmission and removes latency issues is a key reason for increased traction of optical transport network market. Based on the announcements by the services providers, enterprises and vendors the 100G system deployment is now gaining real traction with the higher bandwidth demand. The number of equipment sold in metros is increasing with 15% of annual growth every year.

Further, a huge increase in bandwidth requirement has also been seen in the business customers special in the financial companies, and government organizations. In addition, due to the increasing load on the current networks it has become difficult for the vendors to deploy and manage their advanced systems. Optical transport network overcomes the issues in the present Synchronous Optical Network (SONET)/ Synchronous Digital Hierarchy (SDH) networks such as latency, bandwidth limitation, robust management, transparent client signals, better scalability, and global acceptance as a standard. Thus it is rapidly replacing SDH/SONET globally.

The high initial investment is one of the challenges faced by the vendors and restraining its deployment. However, the vendors are rolling out globally; relying on the huge advantages of this technology. Optical transport network's inherent flexibility is enabled by its ability to extend transparency to the timing plane which is a very important differentiating factor of optical transport network from SONET/SDH. The next opportunity in the networking world is the advanced form i.e. Next Generation, which enables more efficient mapping of and support for data signals such as Ethernet and IP. This technology is expected to enhance the deployment and offer solution to the converged transparent transport of TDM, packet and IP-based services.

This report spans the overall structure of the optical transport network market and provides premium insights that can help software vendors, network operators, telecom service providers, equipment manufacturers, third-party providers, and managed service providers to identify the need of large and small organizations (end users) along with exhibiting the gaps for telecom services provider, and network operators. The report analyzes the growth rate and penetration across all the major regions.

The global optical transport network market research report is segmented on the basis of technology, components, services, type of users, and regions. The technologies are further categorized into Wavelength Division Multiplexer (WDM) and Dense Wavelength Division Multiplexer (DWDM) based on wavelengths [up to 10Gbps, 10Gbps, 40Gbps, 100Gbps, and more than 100Gbps]. On the basis of components the market is defined as optical switch market, optical transport market, and optical packet platform market. The services are segmented as network design and optimization, and network maintenance and support services. Further, the type of users is categorized into communication service providers and network operators, private enterprises, and government.

The global optical transport network market report analyzes global adoption trends, future growth potentials, key drivers, restraints, opportunities, and best practices in this market. The report also examines growth potential market sizes and revenue forecasts across different regions as well as user segments. The notable players in this market, who contributes to the major share, include ADTRAN, ADVA Optical Networking, Alcatel- Lucent, Aliathon Technoplogy, Ciena, Cisco, Fujitsu, Huawei, Infinera, and ZTE.

The report forecasts the optical transport network market sizes and trends in the following submarkets:

On the basis of technology:

- WDM (Metro market)

- up to 10Gbps

- 10Gbps

- 40Gbps

- 100Gbps

- More than 100Gbps

- DWDM (Long haul terrestrial market)

- up to 10Gbps

- 10Gbps

- 40Gbps

- 100Gbps

- More than 100Gbps]

On the basis of components:

- Optical switch market

- Optical transport market

- Optical packet platform market

On the basis of services:

- Network design and optimization

- network maintenance and support services

On the basis of types of users:

- Communication service providers and network operators

- Enterprises

- Government

On the basis of region:

- North America (NA)

- Europe

- Asia-Pacific (APAC)

- Middle East and Africa (MEA)

- Latin America (LA)

Changing user requirements, the rapid growth in IP and Ethernet services, and a dramatic increase in the capacity demanded are driving factors of the optical transport network market. The ecosystem architecture concept was originally developed by the ITU-T initially a decade ago, to build upon the Synchronous Digital Hierarchy (SDH) and Dense Wavelength-Division Multiplexing (DWDM) experience and provide bit rate efficiency, resiliency and management at high capacity. Optical transport network therefore looks a lot like Synchronous Optical Networking (SONET) / SDH in structure, with less overhead and more management features.

Next-Generation optical transport network offers a solution to the converged transparent transport of TDM, packet and IP-based services and goes beyond point-to-point wavelength services by implementing a more flexible architecture based on Optical Channel Data Units (ODU). This next generation of optical networking will develop the transmission layer from a static networking medium to become an intelligent dynamic transport network infrastructure supporting high-capacity multiplexed applications over multi-domains.

The rapid adoption of optical transport network technology components continues to gain momentum in the North America and APAC optical transport network market. This is attributable to the significant leap forward in optical network technology that optical transport network represents and the waning fortunes of SONET/SDH networking.

The optical transport network market research report outlines the key trends, and market sizing and forecasting for various emerging sub-segments. The report also emphasizes on key global adoption trends, future growth potential sub markets, key drivers, competitive outlook, restraints, and opportunities of optical network market ecosystem. It also provides insights into the current and future revenues of market from 2014 through 2019 and is aimed to provide the reader with an understanding of market drivers, current and upcoming players, and competitive landscape.

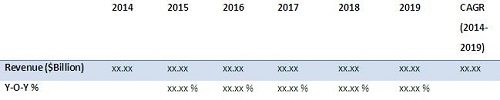

The market is further drilled down; by technology types; by components; by services; by end users; and by regions: North America (NA), Asia Pacific (APAC), Europe, Middle East and Africa (MEA) and Latin America (LA). The global optical transport network market is expected to grow from $11.35 billion in 2014 to $23.64 billion by 2019, at an estimated Compound Annual Growth Rate (CAGR) of 15.8% from 2014 to 2019.

Optical Transport Network Market size, 2014 � 2019 ($Billion, y-o-y %)

Source: Expert Views, Primary Interviews, and MarketsandMarkets Analysis

The figure given below highlights the market size and Y-O-Y growth pattern of the optical transport network market, for the forecast period from 2014 to 2019.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Table of Contents

1 Introduction (Page No. - 15)

1.1 Objectives of the Study

1.2 Market Definition

1.3 Market Scope

1.3.1 Markets Covered

1.3.2 Year

1.3.3 Currency

1.4 Stakeholders

1.5 Limitations

2 Research Methodology (Page No. - 18)

2.1 Introduction

2.2 Market Size Estimation

2.3 Market Breakdown and Data Triangulation

2.4 Market Share Estimation

2.4.1 Key Data From Secondary Sources

2.4.2 Key Data From Primary Sources

2.4.2.1 Key Industry Insights

2.4.3 Assumptions

3 Executive Summary (Page No. - 25)

4 Premium Insights (Page No. - 28)

4.1 Attractive Market Opportunities in the Optical Transport Network Market

4.2 Market: Top Components

4.3 Europe Market: By Components and End Users

4.4 Life Cycle Analysis, By Region, (2014)

5 Market Overview (Page No. - 32)

5.1 Introduction

5.2 Evolution

5.3 Market Segmentation

5.4 Market Dynamics

5.4.1 Drivers

5.4.1.1 Rapid Increase in the Bandwidth and Capacity Demand

5.4.1.2 Increasing Internet Use By Residential Customers

5.4.1.3 Resolves the SONET/SDH Networks Issues

5.4.2 Restraints

5.4.2.1 High Initial Investment

5.4.2.2 Failure of Early P-Ots Installation

5.4.3 Opportunities

5.4.3.1 Next-Generation Optical Transport Network

5.4.3.2 Introduction of New Technologies

5.4.4 Challenges

5.4.4.1 Tolerance to Chromatic Dispersion and Osnr

5.4.4.2 Up-Gradation of Legacy Systems

6 Industry Trends (Page No. - 42)

6.1 Value Chain Analysis

6.2 Porter�s Five Forces Analysis

6.2.1 Bargaining Power of Suppliers

6.2.2 Bargaining Power of Buyers

6.2.3 Threat From New Entrants

6.2.4 Threat From Substitutes

6.2.5 Intensity of Rivalry

7 Optical Transport Network Market Analysis, By Technology (Page No. - 47)

7.1 Introduction

7.2 Wavelength Division Multiplexer (WDM)

7.3 WDM (Metro Market)

7.4 DWDM (Long-Haul Terrestrial Market)

8 Market Analysis, By Component (Page No. - 58)

8.1 Introduction

8.2 Optical Switch Market

8.3 Optical Transport Market

8.4 Optical Packet Platform Market

9 Market Analysis, By Services (Page No. - 65)

9.1 Introduction

9.2 Network Design and Optimization Services

9.3 Network Maintenance and Support Services

10 Optical Transport Network Market Analysis, By Type of User (Page No. - 69)

10.1 Introduction

10.2 Communication Service Providers and Network Operators

10.3 Enterprises

10.4 Government

11 Geographic Analysis (Page No. - 74)

11.1 Introduction

11.2 North America

11.3 Europe

11.4 Asia-Pacific

11.5 Middle East and Africa

11.6 Latin America

12 Competitive Landscape (Page No. - 96)

12.1 Overview

12.2 Market Share Analysis

12.3 Competitive Situations and Trends

12.3.1 Global Optical Transport Network Market, 2014

12.4 New Product/Technology Launches

12.5 Agreement, Partnerships, Collaborations, and Joint Ventures

12.6 Mergers & Acquisitions (M&A), 2012-2014

13 Company Profiles (Page No. - 111)

13.1 Introduction

13.2 Alcatel-Lucent

13.2.1 Business Overview

13.2.2 Product Portfolio

13.2.3 Key Strategies

13.2.4 Recent Developments

13.2.5 SWOT Analysis

13.2.6 MNM View

13.3 Ciena Corporation

13.3.1 Business Overview

13.3.2 Products and Services

13.3.3 Key Strategies

13.3.4 Recent Developments

13.3.5 SWOT Analysis

13.3.6 MNM View

13.4 CISCO Systems, Inc.

13.4.1 Business Overview

13.4.2 Products & Services

13.4.3 Key Strategy

13.4.4 Recent Developments

13.4.5 SWOT Analysis

13.4.6 MNM View

13.5 Huawei Technologies

13.5.1 Business Overview

13.5.2 Product & Services

13.5.3 Key Strategy

13.5.4 Recent Developments

13.5.5 SWOT Analysis

13.5.6 MNM View

13.6 ZTE Corporation

13.6.1 Business Overview

13.6.2 Product Portfolio

13.6.3 Key Strategies

13.6.4 Recent Developments

13.6.5 SWOT Analysis

13.6.6 MNM View

13.7 Adtran, Inc.

13.7.1 Business Overview

13.7.2 Products Portfolio

13.7.3 Key Strategies

13.7.4 Recent Developments

13.7.5 MNM View

13.8 ADVA Optical Networking SE

13.8.1 Business Overview

13.8.2 Products and Services

13.8.3 Key Strategies

13.8.4 Recent Developments

13.8.5 MNM View

13.9 Aliathon Technology Ltd

13.9.1 Business Overview

13.9.2 Products and Services

13.9.3 Key Strategy

13.9.4 Recent Developments

13.9.5 MNM View

13.10 Fujitsu Ltd

13.10.1 Business Overview

13.10.2 Product Portfolio

13.10.3 Key Strategies

13.10.4 Recent Developments

13.10.5 MNM View

13.11 Infinera Corporation

13.11.1 Business Overview

13.11.2 Products Portfolio

13.11.3 Key Strategies

13.11.4 Recent Developments

13.11.5 MNM View

14 Appendix (Page No. - 140)

14.1 Discussion Guide

14.2 Introducing RT: Real-Time Market Intelligence

14.3 Available Customizations

14.4 Related Reports

List of Tables (79 Tables)

Table 1 Market, By Type, 2012�2019 ($Million)

Table 2 Optical Transport Network Resolves the Various Flaws of SONET/SDH

Table 3 High Initial Investment Restraining the Adoption

Table 4 Next-Generation Optical Transport Network A Huge Opportunity for Market

Table 5 Up-Gradation of Legacy Systems is A Major Challenge for This Market

Table 6 WDM Market, By Type, 2012�2019 ($Million)

Table 7 Optical Transport Network Market Size, By Region, 2012�2019 ($Million)

Table 8 WDM - Metro Market, By Region, 2012�2019 ($Million)

Table 9 WDM - Metro Market, By Bandwidth Technology, 2014�2019 ($Million)

Table 10 WDM Bandwidth Technology (Up to 10 GBPS Wavelengths), By Region, 2012�2019 ($Million)

Table 11 WDM Bandwidth Technology (10 GBPS Wavelengths), By Region, 2012�2019 ($Million)

Table 12 WDM Bandwidth Technology (40 GBPS Wavelengths), By Region, 2012�2019 ($Million)

Table 13 WDM Bandwidth Technology (100 GBPS Wavelengths), By Region, 2012�2019 ($Million)

Table 14 WDM Bandwidth Technology (More Than100 GBPS Wavelengths), By Region, 2012�2019 ($Million)

Table 15 DWDM-Long-Haul Terrestrial Market, By Region, 2012�2019 ($Million)

Table 16 DWDM-Long-Haul Terrestrial Market, By Bandwidth Technology, 2012�2019 ($Million)

Table 17 DWDM Bandwidth Technology (Up to 10 GBPS Wavelengths), By Region, 2012�2019 ($Million)

Table 18 DWDM Bandwidth Technology (10 GBPS Wavelengths), By Region, 2012�2019 ($Million)

Table 19 DWDM Bandwidth Technology (40 GBPS Wavelengths), By Region, 2012�2019 ($Million)

Table 20 DWDM Bandwidth Technology (100 GBPS Wavelengths), By Region, 2012�2019 ($Million)

Table 21 DWDM Bandwidth Technology (More Than100 GBPS Wavelengths), By Region, 2012�2019 ($Million)

Table 22 Optical Transport Network Market Size, By Component, 2012�2019 ($Million)

Table 23 Optical Switch Market, By Region, 2012�2019 ($Million)

Table 24 Optical Transport Market, By Region, 2012�2019 ($Million)

Table 25 Optical Packet Platform Market, By Region, 2012�2019 ($Million)

Table 26 Optical Packet Platform Market, By Type, 2012�2019 ($Million)

Table 27 Optical Packet Platform- Transport Market, By Region, 2012�2019 ($Million)

Table 28 Optical Packet Platform- Switch Market, By Region, 2012�2019 ($Million)

Table 29 Optical Transport Network Market Size, By Services, 2012�2019 ($Million)

Table 30 Network Design and Optimization Services Market Size, By Region, 2012�2019 ($Million)

Table 31 Network Maintenance and Support Services Market Size, By Region, 2012�2019 ($Million)

Table 32 Market Size, By Type of User, 2012�2019 ($Million)

Table 33 Communication Service Provider and Network Operators Market Size, By Region, 2012�2019 ($Million)

Table 34 Enterprises Market Size, By Region, 2012�2019 ($Million)

Table 35 Government Market Size, By Region, 2012�2019 ($Million)

Table 36 Optical Transport Network Market Size, By Region, 2012�2019 ($Million)

Table 37 NA: Market Size, By Types, 2012�2019 ($Million)

Table 38 NA: WDM Market Size, By Type, 2012-2019 ($Million)

Table 39 NA: WDM-Metro Market Size, By Bandwidth Technology, 2012�2019 ($Million)

Table 40 NA: DWDM-Long-Haul Terrestrial Market Size, By Bandwidth Technology, 2012�2019 ($Million)

Table 41 NA: Market Size, By Components, 2012�2019 ($Million)

Table 42 NA: Optical Packet Platform Market Size, By Types, 2012�2019 ($Million)

Table 43 NA: Market Size, By Services, 2012�2019 ($Million)

Table 44 NA: Market Size, By Type of User, 2012�2019 ($Million)

Table 45 Europe: Market Size, By Types, 2012�2019 ($Million)

Table 46 Europe: WDM Market Size, By Type, 2012-2019 ($Million)

Table 47 Europe: WDM-Metro Market Size, By Bandwidth Technology, 2012�2019 ($Million)

Table 48 Europe: DWDM-Long-Haul Terrestrial Market Size, By Bandwidth Technology, 2012�2019 ($Million)

Table 49 Europe: Market Size, By Components, 2012�2019 ($Million)

Table 50 Europe: Optical Packet Platform Market Size, By Types, 2012�2019 ($Million)

Table 51 Europe: Optical Transport Network Market Size, By Services, 2012�2019 ($Million)

Table 52 Europe: Market Size, By Type of User, 2012�2019 ($Million)

Table 53 APAC: Market Size, By Types, 2012�2019 ($Million)

Table 54 APAC: WDM Market Size, By Type, 2012-2019 ($Million)

Table 55 APAC: WDM-Metro Market Size, By Bandwidth Technology, 2012�2019 ($Million)

Table 56 APAC: DWDM-Long-Haul Terrestrial Market Size, By Bandwidth Technology, 2012�2019 ($Million)

Table 57 APAC: Market Size, By Component, 2012�2019 ($Million)

Table 58 APAC: Optical Packet Platform Market Size, By Types, 2012�2019 ($Million)

Table 59 APAC: Market Size, By Services, 2012�2019 ($Million)

Table 60 APAC: Market Size, By Type of User, 2012�2019 ($Million)

Table 61 MEA: Market Size, By Types, 2012�2019 ($Million)

Table 62 MEA: WDM Market Size, By Type, 2012-2019 ($Million)

Table 63 MEA: WDM-Metro Market Size, By Bandwidth Technology, 2012�2019 ($Million)

Table 64 MEA: DWDM-Long-Haul Terrestrial Market Size, By Bandwidth Technology, 2012�2019 ($Million)

Table 65 MEA: Market Size, By Components, 2012�2019 ($Million)

Table 66 MEA: Optical Packet Platform Market Size, By Types, 2012�2019 ($Million)

Table 67 MEA: Market Size, By Services, 2012�2019 ($Million)

Table 68 MEA: Market Size, By Type of User, 2012�2019 ($Million)

Table 69 LA: Optical Transport Network Market Size, By Types, 2012�2019 ($Million)

Table 70 LA: WDM Market Size, By Type, 2012-2019 ($Million)

Table 71 LA: WDM-Metro Market Size, By Bandwidth Technology, 2012�2019 ($Million)

Table 72 LA: DWDM-Long-Haul Terrestrial Market Size, By Bandwidth Technology, 2012�2019 ($Million)

Table 73 LA: DWDM-Long-Haul Terrestrial Market Size, By Bandwidth Technology, 2012�2019 ($Million)

Table 74 LA: Optical Packet Platform Market Size, By Types, 2012�2019 ($Million)

Table 75 LA: Market Size, By Services, 2012�2019 ($Million)

Table 76 NA: Market Size, By Type of User, 2012�2019 ($Million)

Table 77 New Product Launches, 2012�2014

Table 78 Agreements, Partnerships, Collaborations, and Joint Ventures, 2012�2014

Table 79 Mergers & Acquisitions

List of Figures (45 Figures)

Figure 1 Global Optical Transport Network Market: Research Methodology

Figure 2 Market Size Estimation Methodology: Bottom-Up Approach

Figure 3 Market Size Estimation Methodology: Top-Down Approach

Figure 4 Global Optical Transport Network Market: Assumptions

Figure 5 Market Snapshot (2014 vs. 2019)

Figure 6 Global Market Snapshot, 2014

Figure 7 Increasing Bandwidth Demand Pushing the Market

Figure 8 Optical Transport Market Segment Contributes to the Biggest Market Share Among the Components

Figure 9 CSPS and Network Operators Accounts for the Highest Share in Europe Region

Figure 10 APAC and MEA Markets Experiencing Fastest Growth Due to Increasing Bandwidth Demand in Developing Countries Such as Japan and China

Figure 11 Evolution of Market

Figure 12 Market Segmentation: By Technology

Figure 13 Market Segmentation: By Component

Figure 14 Optical Transport Network Market: By Services

Figure 15 Increasing Internet Use By Residential Customers Will Fuel the Demand

Figure 16 Value Chain Analysis

Figure 17 Porter�s Five Forces Analysis

Figure 18 Market Technologies

Figure 19 DWDM- Long-Haul Terrestrial Market Growing With the Higher CAGR

Figure 20 Components Market

Figure 21 Optical Transport Network Market Size, By Components, 2014�2019 ($Million)

Figure 22 Market Size, By Services, 2014�2019 ($Million)

Figure 23 Market Size, By End User, 2014�2019 ($Million)

Figure 24 Geographic Snapshot (2014): APAC Showing the Highest Growth Rate

Figure 25 APAC Growing Fastest With the CAGR of 19.3%

Figure 26 NA Market Evaluation

Figure 27 Companies Adopted Partnerships and Collaborations as the Key Growth Strategy

Figure 28 Global Market, 2014

Figure 29 Market Evaluation Framework- Significant Partnerships Has Fuled the Growth of Optical Transport Network Market

Figure 30 Geographic Revenue Mix of Top 5 Market Players: Reference

Figure 31 Alcatel-Lucent, Inc: Business Overview

Figure 32 SWOT Analysis

Figure 33 Ciena Corporation: Business Overview

Figure 34 SWOT Analysis

Figure 35 CISCO Systems, Inc.: Business Overview

Figure 36 SWOT Analysis

Figure 37 Huawei Technologies: Business Overview

Figure 38 SWOT Analysis

Figure 39 ZTE Corporation : Business Overview

Figure 40 SWOT Analysis

Figure 41 Adtran, Inc.: Business Overview

Figure 42 ADVA Optical Networking SE: Business Overview

Figure 43 Aliathon Technology Ltd: Business Overview

Figure 44 Fujitsu Ltd: Business Overview

Figure 45 Infinera Corporation: Business Overview

Growth opportunities and latent adjacency in Optical Transport Network Market