Chronic Lymphocytic Leukemia Therapeutics Market in G8 Countries (2010 - 2020)

Chronic Lymphocytic Leukemia Therapeutics Market in G8 Countries (2010 - 2020)

Chronic lymphocytic leukemia is the second most common cancer in adult males and rarely occurs in children. The risk of chronic lymphocytic leukemia is closely associated with age. About 90% of chronic lymphocytic leukemia is diagnosed in middle age. Incidence rate of CLL is high in men and women over 50 years of age. The chronic lymphocytic leukemia market is segmented into two types; namely childhood chronic lymphocytic leukemia and adulthood lymphocytic leukemia. The market was dominated by Campath drug in 2010. However, in 2020, the market is expected to be equally dominated by GA101/RG7159 molecule and Arzerra drug.

This report studies the market from 2010 to 2020 covering seven major regimens and single drugs (off-patent and pipeline) for chronic lymphocytic leukemia treatment. At present, there are two regimens in the market; namely FC regimen and FCR regimen. Plus, there are four drugs in the market; such as Fludara (Fludarabine), Campath, Treanda, and Arzerra. Growing chronic lymphocytic leukemia population is an impetus for the growth of the market. This market is expected to grow at a CAGR of 13.43% from 2015 to 2020. North America was the major contributor to this market; accounting for 61.21% of the total sales of chronic lymphocytic leukemia drugs in 2010; whereas Campath was the major drug accounting for 42.32% of the total sales of chronic lymphocytic leukemia drugs in 2010. Fludara is highly effective in the treatment of CLL that captured the high market share of CLL market. Chronic lymphocytic leukemia is still an arena with high unmet need for early diagnosis and limited treatment options in this area.

The report studies six existing regimens and single drugs for chronic lymphocytic leukemia market. Currently, there is one major drug in pipeline for chronic lymphocytic leukemia; which is expecting a market launch by 2014; GA101/RG7159 will be launched in the market in 2014 by Genentech Inc (U.S.). The drug is expected to be priced at $409,586 for patients who take them annually.

Players are implementing various growth strategies in the market to gain a competitive edge. New product launches, product pipelines, agreements and collaborations, clinical trials, and acquisitions were the major strategies adopted by the players from January 2008 to September 2011.

Agreements and collaborations form the basic growth strategy in the chronic lymphocytic leukemia therapeutics market; accounting for 29% share in this market between January 2008 and September 2011, followed by NDA & BLA applications with a 25% share in the market and approvals with a 21% share.

Genzyme Corporation, Roche, GlaxoSmithKline Pharmaceuticals Limited, and Cephalon Inc rule the present market for chronic lymphocytic leukemia drugs; whereas Roche/Biogen Idec is expected to capture major share of the market by 2020.

Scope of the report

This chronic lymphocytic leukemia therapeutics market research report evaluates the leukemia therapeutics market with respect to the current and pipeline drugs and regimens. The report analyzes geography; forecasting revenue, and trends in each of the following submarkets:

- Chemotherapy regimens

- FC regimen

- FCR regimen

- Chemotherapy drugs

- Fludara

- Campath/MabCampath

- Treanda

- Arzerra

- Pipeline drugs

- GA101 / RG7159

The geographies covered under the report are

- North America

- U.S.

- Canada

- Europe

- U.K.

- Germany

- Italy

- France

- Spain

- Japan

Each section provides market data, market drivers, trends and opportunities, key players, and competitive outlook. This report also provides market tables for covering the sub-segments and micro-markets. Additionally, it makes ways for company profiles that cover all the sub-segments. The report has been made by keeping past trends, current happenings, and future forecasts in consideration.

B-cell chronic lymphocytic leukemia (B-CLL), also known as chronic lymphoid leukemia (CLL), is the most common type of leukemia. Chronic lymphocytic leukemia is also known as chronic lymphoid leukemia. It can be described as a slow increase in the number of white blood cells in the blood and the bone marrow. White blood cells guard the body from infections caused by bacteria. Chronic lymphocytic leukemia is divided by the type of lymphocyte involved; such as B-cell or T-cell. Chronic lymphocytic leukemia is divided mainly into three types, namely B-cell leukemia, T-cell leukemia, and NK-cell leukemia. Chronic leukemia can prove to be equally fatal as that of its counterparts.

The risk of chronic lymphocytic leukemia is closely associated with age. About 90% chronic lymphocytic leukemia is diagnosed in adults. Incidence rate of chronic lymphocytic leukemia is high in men and women over 50 years with a ratio of approximately 1.7:1. Prevalence of chronic lymphocytic leukemia is very high in men and women between the 75 and 84 years of age.

Chronic lymphocytic leukemia is divided into different stages from 0 to IV. This staging system classified according to the patient has specific symptoms. Doctor can decide the kind of treatment suitable and help in the diagnosis. The patients who are in the earlier stage can have better long-term survival.

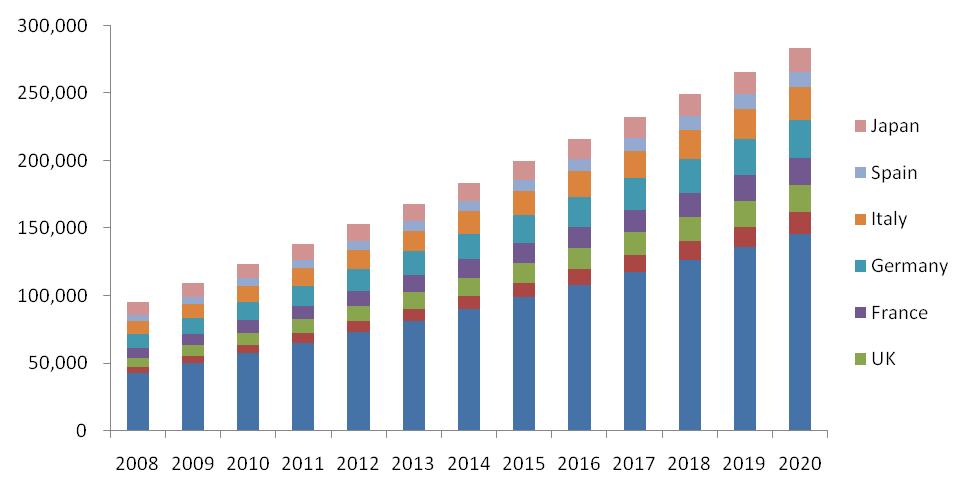

Chronic Lymphocytic Leukemia Diagnosed Population, 2008 - 2020, (Thousands)

Source: Globocan

According to WHO, chronic lymphocytic leukemia is expected to be more prominent in the developed world due to genetic factors. Exposure to certain chemicals is the primary cause of all the types of chronic lymphocytic leukemia. Global incidence of chronic lymphocytic leukemia was 94,960 in 2008 in the developing countries. Total 123,379 new cases were recorded in 2010 with 199,472 and 282,683 as the predicted new cases for 2015 and 2020.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 KEY TAKE-AWAYS

1.2 REPORT DESCRIPTION

1.3 MARKETS COVERED

1.4 STAKEHOLDERS

1.5 RESEARCH METHODOLOGY

1.5.1 MARKET SIZE

1.5.2 KEY DATA POINTS FROM SECONDARY SOURCES

1.5.3 ASSUMPTIONS MADE FOR THIS REPORT

2 EXECUTIVE SUMMARY

2.1 OVERVIEW OF THE MARKET

3 MARKET OVERVIEW

3.1 DEFINING LEUKEMIA

3.2 DEFINING CHRONIC LYMPHOCYTIC LEUKEMIA (CLL)

3.2.1 TYPES OF CHRONIC LYMPHOCYTIC LEUKEMIA

3.2.1.1 B-cell CLL

3.2.1.1.1 Hairy cell leukemia

3.2.1.2 T-cell CLL

3.2.1.2.1 Large granular lymphocytic leukemia

3.2.1.3 NK cell CLL

3.3 STAGES/PHASES OF CHRONIC LYMPHOCYTIC LEUKEMIA

3.3.1 STAGE 0

3.3.2 STAGE I

3.3.3 STAGE II

3.3.4 STAGE III

3.3.5 STAGE IV

3.3.6 RAI STAGING SYSTEM (STAGE 0, I, II, III & IV)

3.3.7 RISK FACTORS

3.3.8 DIAGNOSIS

3.3.8.1 Biopsy and bone marrow aspiration

3.3.8.2 Complete blood count (CBC) and differential

3.3.8.3 Philadelphia chromosome�s presence

3.3.8.4 Spinal tap (lumbar puncture) and cerebrospinal fluid (CSF) analysis

3.3.8.5 Immunophenotyping or phenotyping by flow cytometry

3.3.9 CHRONIC LMYPHOCYTIC LEUKEMIA PREVALENCE

3.3.10 INCIDENCE & MORTALITY

3.4 MARKET STRUCTURE

3.4.1 KEY THERAPIES

3.4.1.1 Chemotherapy

3.4.1.2 Stem cell/bone marrow transplant

3.4.1.3 Radiation therapy

4 CHRONIC LYMPHOCYTIC LEUKEMIA MARKET DYNAMICS

4.1 MARKET OVERVIEW

4.2 BURNING ISSUES

4.3 WINNING IMPERATIVE

4.3.1 ROCHE STRATEGY FOCUSING ON ADDRESS UNMET MEDICAL NEEDS

4.4 MARKET DYNAMICS

4.4.1 DRIVERS

4.4.1.1 Innovative therapies to drive the market for leukemia

4.4.1.2 Oncology is the largest therapeutic market with high unmet needs

4.4.1.3 Off-label prescribing drives market growth

4.4.2 RESTRAINT

4.4.2.1 Low production capability for efficient drugs

4.4.3 OPPORTUNITIES

4.4.3.1 Limited players in the market

4.4.3.2 Growing older male population

4.4.3.3 High unmet needs offer potential for market growth

5 CHRONIC LYMPHOCYTIC LEUKEMIA PRODUCT MARKET

5.1 MARKET OVERVIEW

5.1.1 CAMPATH/MABCAMPATH

5.1.2 TREANDA

5.1.3 ARZERRA

5.1.4 FLUDARA

5.1.5 FCR REGIMEN

5.1.6 FC REGIMEN

6 CHRONIC LYMPHOCYTIC LEUKEMIA PIPELINE DRUG (PHASE III)

6.1 PIPELINE DRUG

6.1.1 GA101/RG7159

7 GEOGRAPHICAL ANALYSIS

7.1 U.S.

7.2 CANADA

7.3 U.K.

7.4 GERMANY

7.5 FRANCE

7.6 ITALY

7.7 SPAIN

7.8 JAPAN

8 COMPETITIVE LANDSCAPE

8.1 INTRODUCTION

9 COMPANY PROFILES

9.1 BIOGEN IDEC INC

9.1.1 OVERVIEW

9.1.2 FINANCIALS

9.1.3 PRODUCTS & SERVICES

9.1.4 STRATEGY

9.1.5 DEVELOPMENTS

9.2 CELGENE CORPORATION

9.2.1 OVERVIEW

9.2.2 FINANCIALS

9.2.3 PRODUCTS & SERVICES

9.2.4 STRATEGY

9.2.5 DEVELOPMENTS

9.3 CEPHALON INC

9.3.1 OVERVIEW

9.3.2 FINANCIALS

9.3.3 PRODUCTS & SERVICES

9.3.4 STRATEGY

9.3.5 DEVELOPMENTS

9.4 GENMAB A/S

9.4.1 OVERVIEW

9.4.2 FINANCIALS

9.4.3 PRODUCTS & SERVICES

9.4.4 STRATEGY

9.4.5 DEVELOPMENTS

9.5 GENZYME CORPORATION

9.5.1 OVERVIEW

9.5.2 FINANCIALS

9.5.3 PRODUCTS & SERVICES

9.5.4 STRATEGY

9.5.5 DEVELOPMENTS

9.6 GLAXOSMITHKLINE PLC

9.6.1 OVERVIEW

9.6.2 FINANCIALS

9.6.3 PRODUCTS & SERVICES

9.6.4 STRATEGY

9.6.5 DEVELOPMENTS

9.7 ROCHE HOLDING AG

9.7.1 OVERVIEW

9.7.2 FINANCIALS

9.7.3 PRODUCTS & SERVICES

9.7.4 STRATEGY

9.7.5 DEVELOPMENTS

LIST OF TABLES

TABLE 1 YEARLY COST OF DRUGS IN NORTH AMERICA & JAPAN, 2011 ($)

TABLE 2 YEARLY COST OF DRUGS IN EUROPEAN COUNTRIES, 2011 ($)

TABLE 3 DOSAGE PATTERN OF DRUGS

TABLE 4 CHRONIC LYMPHOCYTIC LEUKEMIA DRUGS MARKET REVENUE, BY DRUGS/REGIMENS, 2008 � 2020 ($MILLION)

TABLE 5 RAI STAGING SYSTEM

TABLE 6 CHRONIC LYMPHOCYTIC LEUKEMIA DRUGS � PATENT STATUS

TABLE 7 CHRONIC LYMPHOCYTIC LEUKEMIA DRUGS MARKET REVENUE, BY TYPES, 2008 � 2020 ($MILLION)

TABLE 8 AGED MALE POPULATION GROWTH, 2010 � 2025 (THOUSAND)

TABLE 9 CHRONIC LYMPHOCYTIC LEUKEMIA DRUGS/REGIMENS MARKET REVENUE, 2008 � 2020 ($MILLION)

TABLE 10 CHRONIC LYMPHOCYTIC LEUKEMIA CAMPATH DRUG MARKET REVENUE, BY COUNTRY, 2008 � 2020 ($MILLION)

TABLE 11 CHRONIC LYMPHOCYTIC LEUKEMIA TREANDA DRUG MARKET REVENUE, BY COUNTRY, 2008 � 2020 ($MILLION)

TABLE 12 CHRONIC LYMPHOCYTIC LEUKEMIA ARZERRA DRUG MARKET REVENUE, BY COUNTRY, 2008 � 2020 ($MILLION)

TABLE 13 CHRONIC LYMPHOCYTIC LEUKEMIA FLUDARA DRUG MARKET REVENUE, BY COUNTRY, 2008 � 2020 ($MILLION)

TABLE 14 CHRONIC LYMPHOCYTIC LEUKEMIA FCR REGIMEN MARKET REVENUE, BY COUNTRY, 2008 � 2020 ($MILLION)

TABLE 15 CHRONIC LYMPHOCYTIC LEUKEMIA FC REGIMEN MARKET REVENUE, BY COUNTRY, 2008 � 2020 ($MILLION)

TABLE 16 CHRONIC LYMPHOCYTIC LEUKEMIA PIPELINE DRUG MARKET, 2014

TABLE 17 CHRONIC LYMPHOCYTIC LEUKEMIA PIPELINE DRUG (GA101/RG7159) MARKET REVENUE, BY COUNTRY, 2015 � 2020 ($MILLION)

TABLE 18 U.S: SEER STATISTICS FOR CHRONIC LYMPHOCYTIC LEUKEMIA (ESTIMATED), 2011

TABLE 19 U.S: CHRONIC LYMPHOCYTIC LEUKEMIA THERAPEUTICS MARKET REVENUE, BY DRUGS/REGIMENS, 2008 � 2020 ($MILLION)

TABLE 20 U.S: CHRONIC LYMPHOCYTIC LEUKEMIA PIPELINE DRUGS MARKET REVENUE, BY DRUG, 2015 � 2020 ($MILLION)

TABLE 21 CANADA: CHRONIC LYMPHOCYTIC LEUKEMIA THERAPEUTICS MARKET REVENUE, BY DRUGS/REGIMENS, 2008 � 2020 ($MILLION)

TABLE 22 CANADA: CHRONIC LYMPHOCYTIC LEUKEMIA PIPELINE DRUGS MARKET REVENUE, BY DRUG, 2015 � 2020 ($MILLION)

TABLE 23 U.K: INCIDENCE OF CHRONIC LYMPHOCYTIC LEUKEMIA, BY GENDER, 2010

TABLE 24 U.K: CHRONIC LYMPHOCYTIC LEUKEMIA THERAPEUTICS MARKET REVENUE, BY DRUGS/REGIMENS, 2008 � 2020 ($MILLION)

TABLE 25 U.K: CHRONIC LYMPHOCYTIC LEUKEMIA PIPELINE DRUGS MARKET REVENUE, BY DRUG, 2015 � 2020 ($MILLION)

TABLE 26 GERMANY: CHRONIC LYMPHOCYTIC LEUKEMIA THERAPEUTICS MARKET REVENUE, BY DRUGS/REGIMENS, 2008 � 2020 ($MILLION)

TABLE 27 GERMANY: CHRONIC LYMPHOCYTIC LEUKEMIA PIPELINE DRUGS MARKET REVENUE, BY DRUG, 2015 � 2020 ($MILLION)

TABLE 28 FRANCE: CHRONIC LYMPHOCYTIC LEUKEMIA THERAPEUTICS MARKET REVENUE, BY DRUGS/REGIMENS, 2008 � 2020 ($MILLION)

TABLE 29 FRANCE: CHRONIC LYMPHOCYTIC LEUKEMIA PIPELINE DRUGS MARKET REVENUE, BY DRUG, 2015 � 2020 ($MILLION)

TABLE 30 ITALY: CHRONIC LYMPHOCYTIC LEUKEMIA THERAPEUTICS MARKET REVENUE, BY DRUGS/REGIMENS, 2008 � 2020 ($MILLION)

TABLE 31 ITALY: CHRONIC LYMPHOCYTIC LEUKEMIA PIPELINE DRUGS MARKET REVENUE, BY DRUG, 2015 � 2020 ($MILLION)

TABLE 32 SPAIN: CHRONIC LYMPHOCYTIC LEUKEMIA DRUGS MARKET REVENUE, BY DRUGS/REGIMENS, 2008 � 2020 ($MILLION)

TABLE 33 SPAIN: CHRONIC LYMPHOCYTIC LEUKEMIA THERAPEUTICS PIPELINE DRUGS MARKET REVENUE, BY DRUG, 2008 � 2020 ($MILLION)

TABLE 34 JAPAN: CHRONIC LYMPHOCYTIC LEUKEMIA THERAPEUTICS MARKET REVENUE, BY DRUGS/REGIMENS, 2008 � 2020 ($MILLION)

TABLE 35 JAPAN: CHRONIC LUMPHOCYTIC LEUKEMIA PIPELINE DRUGS MARKET REVENUE, BY DRUG, 2008 � 2020 ($MILLION)

TABLE 36 COLLABORATIONS/PARTNERSHIPS/AGREEMENTS/JOINT VENTURES, 2008 � 2011

TABLE 37 NEW PRODUCTS LAUNCH, 2008 � 2010

TABLE 38 EXPANSIONS/NEW FACILITY/INVESTMENTS, 2011

TABLE 39 FDA APPROVALS, 2008 � 2010

TABLE 40 PHASE III CLINICAL TRIALS, 2008 � 2010

TABLE 41 NDA, BLA & MARKETING APPLICATIONS, 2008 � 2010

TABLE 42 BIOGEN IDEC INC: TOTAL REVENUE & R&D EXPENSES, 2008 � 2010 ($MILLION)

TABLE 43 BIOGEN IDEC INC: EXISTING PRODUCT & PIPELINE PRODUCT PORTFOLIO

TABLE 44 CELGENE CORPORATION: TOTAL REVENUE & R&D EXPENSES, 2008 � 2010 ($MILLION)

TABLE 45 CELGENE CORPORATION: PRODUCT PIPELINE

TABLE 46 CEPHALON INC: TOTAL REVENUE & R&D EXPENSES, 2008 � 2010 ($MILLION)

TABLE 47 CEPHALON INC: PRODUCT PORTFOLIO

TABLE 48 GENMAB A/S: TOTAL REVENUE & R&D EXPENSES, 2008 � 2010 ($MILLION)

TABLE 49 GENMAB A/S: EXISTING PRODUCT &PIPELINE PRODUCT PORTFOLIO

TABLE 50 GENZYME CORPORATION: TOTAL REVENUE AND R&D EXPENSES, 2008 � 2010 ($MILLION)

TABLE 51 GENZYME CORPORATION: PRODUCT PORTFOLIO

TABLE 52 GLAXOSMITHKLINE PLC: TOTAL REVENUE AND R&D EXPENSES, 2008 � 2010 ($MILLION)

TABLE 53 GLAXOSMITHKLINE PLC: PRODUCT PORTFOLIO

TABLE 54 ROCHE HOLDING: TOTAL REVENUE AND R&D EXPENSES, 2008 � 2010 ($MILLION)

TABLE 55 ROCHE HOLDINGS: MARKET REVENUE, BY BUSINESS SEGMENTS, 2008 � 2010 ($MILLION)

TABLE 56 ROCHE HOLDINGS: EXISTING & PIPELINE PRODUCT PORTFOLIO

LIST OF FIGURES

FIGURE 1 TOTAL CHRONIC LYMPHOCYTIC LEUKEMIA MARKET REVENUE, 2008 � 2020 ($MILLION)

FIGURE 2 CHRONIC LYMPHOCYTIC LEUKEMIA MARKET REVENUE, BY DRUGS/REGIMENS, 2008 � 2020 ($MILLION)

FIGURE 3 LEUKEMIA POPULATION, BY COUNTRY, 2008 � 2020

FIGURE 4 CHRONIC LYMPHOCYTIC LEUKEMIA DEVELOPMENT & PROGRESSION RATE, BY AGE

FIGURE 5 TYPES OF CHRONIC LYMPHCYTIC LEUKEMIA

FIGURE 6 CHRONIC LYMPHOCYTIC LEUKEMIA POPULATION, BY COUNTRY, 2008 � 2020

FIGURE 7 CHRONIC LYMPHOCYTIC LEUKEMIA: MARKET SEGMENTATION, BY DRUGS/REGIMENS

FIGURE 8 CHRONIC LYMPHOCYTIC LEUKEMIA: EXISTING & PIPELINE DRUGS/REGIMENS MARKET SHARE, 2010 VS 2020

FIGURE 9 CHRONIC LYMPHOCYTIC LEUKEMIA MARKET SHARE, BY DRUGS/REGIMENS, 2010 VS 2020

FIGURE 10 CHRONIC LYMPHOCYTIC LEUKEMIA THERAPEUTICS PIPELINE DRUGS MARKET REVENUE, BY DRUG, 2015 VS 2020 ($MILLION)

FIGURE 11 U.S: CHRONIC LYMPHOCYTIC LEUKEMIA THERAPEUTICS MARKET SHARE, BY DRUGS/REGIMENS, 2010 VS 2020 ($MILLION)

FIGURE 12 U.S: CHRONIC LYMPHOCYTIC LEUKEMIA PIPELINE DRUGS MARKET REVENUE, BY DRUG, 2015 VS 2020 ($MILLION)

FIGURE 13 CANADA: CHRONIC LYMPHOCYTIC LEUKEMIA THERAPEUTICS MARKET SHARE, BY DRUGS/REGIMENS, 2010 VS 2020

FIGURE 14 CANADA: CHRONIC LYMPHOCYTIC LEUKEMIA PIPELINE DRUGS MARKET REVENUE, BY DRUG, 2015 VS 2020 ($MILLION)

FIGURE 15 U.K: CHRONIC LYMPHOCYTIC LEUKEMIA THERAPEUTICS MARKET SHARE, BY DRUGS/REGIMENS, 2010 VS 2020

FIGURE 16 U.K: CHRONIC LYMPHOCYTIC LEUKEMIA PIPELINE DRUGS REVENUE, BY DRUG, 2015 VS 2020 ($MILLION)

FIGURE 17 GERMANY: CHRONIC LYMPHOCYTIC LEUKEMIA THERAPEUTICS MARKET SHARE, BY DRUGS/REGIMENS, 2010 VS 2020

FIGURE 18 GERMANY: PIPELINE REGIMENS/DRUGS MARKET SHARE, BY DRUG, 2015 VS 2020 ($MILLION)

FIGURE 19 FRANCE: CHRONIC LYMPHOCYTIC LEUKEEMIA THERAPEUTICS MARKET SHARE, BY DRUGS/REGIMENS, 2010 VS 2020

FIGURE 20 FRANCE: CHRONIC LYMPHOCYTIC LEUKEMIA PIPELINE DRUG MARKET REVENUE, BY DRUG, 2015 VS 2020 ($MILLION)

FIGURE 21 ITALY: CHRONIC LYMPHOCYTIC LEUKEMIA THERAPEUTICS MARKET SHARE, BY DRUGS/REGIMENS, 2010 VS 2020

FIGURE 22 ITALY: CHRONIC LYMPHOCYTIC LEUKEMIA PIPELINE DRUGS MARKET REVENUE, BY DRUG, 2015 VS 2020 ($MILLION)

FIGURE 23 SPAIN: CHRONIC LYMPHOCYTIC LEUKEMIA MARKET SHARE, BY DRUGS/REGIMENS, 2010 VS 2020

FIGURE 24 SPAIN: CHRONIC LYMPHOCYTIC LEUKEMIA PIPELINE DRUGS MARKET REVENUE, BY DRUG, 2015 � 2020 ($MILLION)

FIGURE 25 JAPAN: CHRONIC LYMPHOCYTIC THERAPEUTICS MARKET SHARE, BY DRUGS/REGIMENS, 2010 VS 2020

FIGURE 26 JAPAN: CHRONIC LYMPHOCYTIC LEUKEMIA PIPELINE DRUGS MARKET REVENUE, BY DRUG, 2015 VS 2020 ($MILLION)

FIGURE 27 KEY GROWTH STRATEGIES, JANUARY 2008 � SEPTEMBER 2011

Generating Response ...

Generating Response ...

Growth opportunities and latent adjacency in Chronic Lymphocytic Leukemia Therapeutics Market