Leather Chemicals Market by Type (Tanning & Dyeing Chemicals, Beamhouse Chemicals and Finishing Chemicals) and by Region - Trends & Forecasts to 2019

[121 Pages Report] The leather chemicals market is projected to reach $7,963 million by 2019, growing with a CAGR of 7.64% between 2014 and 2019. The leather production process involves several chemical reactions. The basic process is beamhouse process, which mainly includes beamhouse chemicals such as cleansing chemicals and degreasing agents. This is followed by leather tanning, which consumes tanning & dyeing chemicals such as synthetic tanning agents (syntans), fatliquors and dyes. The syntans (synthetic tanning agents) are considered as a substitute for vegetable tanning agents. Tanning operation ensures retaining the physical properties of leather and also helps in maintaining its softness and weather resistance.

The final stage of leather processing is leather finishing, which requires typical finishing chemicals to convert crust of leather into the final leather. The major purpose of using finishing chemicals is to bring certain properties to the leather such as water resistance, heat resistance.

The report covers the global leather chemicals market in major regions namely Asia-Pacific, North America, Europe, and the RoW for three major types, tanning & dyeing chemicals, beamhouse chemicals and finishing chemicals.

This report analyzes different marketing trends and identifies the most effective growth strategies in the market. It identifies market dynamics such as drivers, restraints, opportunities, and challenges. Major companies such as BASF SE (Germany), TFL Ledertechnik Gmbh & Co.KG (Germany), Stahl International BV (The Netherlands), Lanxess AG (Germany), Bayer AG (Germany) and Clariant International Ltd. (Switzerland) have also been profiled.

Segmentation:

By Type:

- Tanning & Dyeing Chemicals

- Beamhouse Chemicals

- Finishing Chemicals

By Region:

- Asia-Pacific

- North America

- Europe

- RoW

This report also includes the leading manufacturers� profiles such as BASF SE (Germany), TFL Ledertechnik Gmbh & Co.KG (Germany), Lanxess AG (Germany), Stahl International BV (The Netherlands), Bayer AG (Germany), Clariant International Ltd. (Switzerland), Schill & Seilacher Gmbh & Co.KG (Germany), DyStar Singapore Pte Ltd (Singapore) and Elementis plc (U.K.).

The leather chemicals market is projected to reach $7,963 million at a CAGR of 7.64% by 2019. Leather chemicals are used at different stages of leather production. The process starts with beamhouse operations, followed by tanning operations. The tanning process can be done by using two methods; vegetable tanning and chrome tanning. The vegetable tanned hides & skins are flexible and are mostly used in furniture.

Some chemicals used in the leather manufacturing process such as chromium, are considered as hazardous and banned in regions such as Europe. The regulatory policies set by REACH (Registration, Evaluation, Authorization and Restriction of Chemical substances), on the use of certain chemicals in tanneries has hampered the consumption of leather chemcials.

Countries like China, India, Brazil and Mexico have emerged as leading destinations, driving the demand for leather chemicals. The market in developing nations is dominated by tanning & dyeing chemicals. The market in China and India are one of the fastest-growing leather chemical market. Rapidly growing footwear, automotive leather apparel and leather goods industries are driving the growth of leather chemicals.

The finishing chemicals are specialty chemicals that are consumed at large scale in Europe. Italy is the major market for leather chemicals and is projected to grow with the highest CAGR between 2014 and 2019. The leather goods industry along with apparels industry is driving the growth in Italian leather chemicals market.

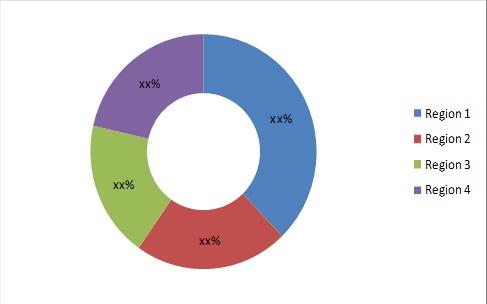

The global market for leather chemicals is witnessing high growth due to the growing demand for premium quality leather. The Asia-Pacific region dominated the market in 2013, globally. Asia-Pacific is projected to show the highest growth rate of 8.46% between 2014 and 2019, in terms of value for the market.

The major types in the market are tanning & dyeing chemicals, beamhouse chemicals and finishing chemicals. The market size in terms of volume was highest for tanning & dyeing chemicals in 2013 and is projected to continue the trend by 2019.

Leather Chemicals Market Share, By Region, 2013

Source: MarketsandMarkets Analysis

The major market players focus on expanding their regional presence while small players are mostly local in nature. The major players are also focusing on capturing market share by introducing new products in the market to enhance their product portfolio, technological knowledge, and regional presence.

The leather chemicals market is projected to witness a high growth from developing regions. One of the major challenges to this market is to find an alternative to the hazardous chemicals used in leather processing.

The report analyzes the market based on major types and regions. It also covers the market behavior of leading producers, key developments, and strategies implemented to sustain and succeed in the market.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Table of Contents

1 Introduction (Slide No.- 12)

1.1 Objectives of the Study

1.2 Market Scope

1.2.1 Market Definition

1.2.2 Markets Covered

1.3 Stakeholders

2 Research Methodology (Slide No.- 14)

2.1 Market Size Estimation

2.2 Market Crackdown & Data Triangulation

2.2.1 Key Data From Secondary Sources

2.2.2 Key Data From Primary Sources

2.2.3 Assumptions

3 Executive Summary (Slide No.- 20)

4 Premium Insights (Slide No.- 23)

4.1 Attractive Market Opportunity for Leather Chemicals

5 Market Overview (Slide No.- 26)

5.1 Introduction

5.2 Leather Manufacturing Process

5.2.1 Beamhouse Operations

5.2.2 Tanning & Dyeing

5.2.3 Finishing (Wet Finishing)

5.3 Market Segmentation

5.3.1 Market Segmentation By Type

5.3.2 Market Segmentation, By Region

5.4 Market Dynamics

5.4.1 Drivers

5.4.1.1 Growing Demand for Premium Quality Leather

5.4.1.2 Abundance of Raw Materials

5.4.2 Restraints

5.4.2.1 Increasing Operational Costs

5.4.2.2 Stringent Environmental Regulatory Policies

5.4.3 Opportunities

5.4.3.1 Shift Toward Asia-Pacific

5.4.4 Challenges

5.4.4.1 Alternatives for Hazardous Chemicals

6 Industry Trends (Slide No.- 35)

6.1 Introduction

6.2 Supply Chain Analysis

6.3 Pricing & Cost Analysis

6.4 Porter�s Five forces Analysis

6.4.1 Bargaining Power of Suppliers

6.4.2 Bargaining Power of Buyers

6.4.3 Threat of New Entrants

6.4.4 Threat of New Substitutes

6.4.5 Intensity of Rivalry

7 Market, By Type (Slide No.- 39)

7.1 Introduction

7.2 Tanning & Dyeing Chemicals Market

7.3 Beamhouse Chemicals Market

7.4 Finishing Chemicals Market

8 Regional Analysis (Slide No.- 46)

8.1 Introduction

8.2 Asia-Pacific

8.2.1 China

8.2.2 India

8.2.3 South Korea

8.2.4 Thailand

8.2.5 Japan

8.2.6 Rest of Asia-Pacific

8.3 North America

8.3.1 U.S.

8.3.2 Canada

8.3.3 Mexico

8.4 Europe

8.4.1 Italy

8.4.2 Germany

8.4.3 Spain

8.4.4 France

8.4.5 U.K.

8.4.6 Rest of Europe

8.5 Rest of the World (ROW)

8.5.1 Brazil

8.5.2 Argentina

8.5.3 Ethiopia

8.5.4 Others

9 Competitive Landscape (Slide No.- 75)

9.1 Overview

9.1.1 Market Share Analysis for Leather Chemicals Market

9.1.2 Competitive Situation & Trends

9.1.3 New Product Launches & New Product Developments

9.1.4 Expansions & Investments

9.1.5 Mergers & Acquisitions

9.1.6 Agreement, Collaboration & Partnership

10 Company Profiles (Slide No.- 86)

(Overview, Financial*, Products & Services, Strategy, and Developments)

10.1 Introduction

10.2 BASF SE

10.3 Bayer AG

10.4 Lanxess AG

10.5 Elementis PLC

10.6 TFL Ledertechnik Gmbh

10.7 Clariant International Ltd

10.8 Dystar Singapore Pte Ltd.

10.9 Stahl Holdings B.V.

10.10 Schill+Seilacher Gmbh

10.11 Zschimmer & Schwarz & Co KG Chemische Fabriken

*Details Might Not Be Captured in Case of Unlisted Companies.

11 Appendix (Slide No.- 116)

11.1 Discussion Guide

11.2 Introducing Rt: Real-Time Market Intelligence

11.3 Available Customizations

11.4 Related Reports

List of Tables (75 Tables)

Table 1 Global Leather Chemicals Market Size (KT) & ($Million), 2012 � 2019

Table 2 Rising Demand for Luxurious Leather is Driving the Growth of Market

Table 3 Increasing Prices of Raw Materials Coupled With Stringent Environmental Regulations Affecting the Growth of Market

Table 4 Shift of Production Facilities Toward Asia-Pacific is An Upcoming Opportunity

Table 5 Finding Replacement for Hazardous Chemicals is A Big Challenge

Table 6 Global: Leather Chemical Market Size, By Type, 2012�2019 ($Million)

Table 7 Global: Leather Chemicals Market Size, By Type, 2012�2019 (KT)

Table 8 Tanning & Dyeing Chemicals Market Size, By Region, 2012�2019 ($Million)

Table 9 Tanning & Dyeing Chemicals Market Size, By Region, 2012�2019 (KT)

Table 10 Beamhouse Chemicals Market Size, By Region, 2012�2019 ($Million)

Table 11 Beamhouse Chemicals Market Size, By Region, 2012�2019 (KT)

Table 12 Finishing Chemicals Market Size, By Region, 2012�2019 ($Million)

Table 13 Finishing Chemicals Market Size, By Region, 2012�2019 (KT)

Table 14 Global: Leather Chemicals Market Size, By Region, 2012�2019 ($Million)

Table 15 Global: Leather Chemical Market Size, By Region, 2012�2019 (KT)

Table 16 Global: Leather Chemicals Market Size, By Type, 2012�2019 ($Million)

Table 17 Global: Leather Chemical Market, By Type, 2012�2019 (KT)

Table 18 Asia-Pacific: Leather Chemicals: Market, By Type, 2012�2019 ($Million)

Table 19 Asia-Pacific: Market, By Type, 2012�2019 (KT)

Table 20 Asia-Pacific: Market Size, By Region, 2012�2019 ($Million)

Table 21 Asia-Pacific: Leather Chemicals Market Size, By Region, 2012�2019 (KT)

Table 22 China: Market Size, By Type, 2012�2019 ($Million)

Table 23 China: Market Size, By Type, 2012�2019 (KT)

Table 24 India: Market Size, By Type, 2012�2019 ($Million)

Table 25 India: Market Size, By Type, 2012�2019 (KT)

Table 26 South Korea: Leather Chemicals: Market Size, By Type, 2012�2019 ($Million)

Table 27 South Korea: Market Size, By Type, 2012�2019 (KT)

Table 28 Thailand: Market Size, By Type, 2012�2019 ($Million)

Table 29 Thailand: Market Size, By Type, 2012�2019 (KT)

Table 30 Japan: Market Size, By Type, 2012�2019 ($Million)

Table 31 Japan: Market Size, By Type, 2012�2019 (KT)

Table 32 Rest of Asia-Pacific: Leather Chemicals Market Size, By Type, 2012�2019 ($Million)

Table 33 Rest of Asia-Pacific: Market Size, By Type, 2012�2019 (KT)

Table 34 North America: Leather Chemicals: Market Size, By Type, 2012�2019 ($Million)

Table 35 North America: Market Size, By Type, 2012�2019 (KT)

Table 36 North America: Market Size, By Region, 2012�2019 (KT)

Table 37 North America: Leather Chemicals Market, By Region, 2012�2019 (KT)

Table 38 U.S.: Market Size, By Type, 2012�2019 ($Million)

Table 39 U.S.: Leather Chemicals: Market Size, By Type, 2012�2019 (KT)

Table 40 Canada: Market Size, By Type, 2012�2019 ($Million)

Table 41 Canada: Market Size, By Type, 2012�2019 (KT)

Table 42 Mexico: Market Size, By Type, 2012�2019 ($Million)

Table 43 Mexico: Market Size, By Type, 2012�2019 (KT)

Table 44 Europe: Market Size, By Type, 2012�2019 ($Million)

Table 45 Europe: Market Size, By Type, 2012�2019 (KT)

Table 46 Europe: Market Size, By Region, 2012�2019 (KT)

Table 47 Europe: Market Size, By Region, 2012�2019 (KT)

Table 48 Italy: Market Size, By Type, 2012�2019 ($Million)

Table 49 Italy: Market Size, By Type, 2012�2019 (KT)

Table 50 Germany: Leather Chemicals Market Size, By Type, 2012�2019 ($Million)

Table 51 Germany Market Size, By Type, 2012�2019 (KT)

Table 52 Spain Market Size, By Type, 2012�2019 ($Million)

Table 53 Spain: Market Size, By Type, 2012�2019 (KT)

Table 54 France Market Size, By Type, 2012�2019 ($Million)

Table 55 France Market Size, By Type, 2012�2019 (KT)

Table 56 U.K. Market Size, By Type, 2012�2019 ($Million)

Table 57 U.K. Market Size, By Type, 2012�2019 (KT)

Table 58 Rest of Europe Market Size, By Type, 2012�2019 ($Million)

Table 59 Rest of Europe Leather Chemicals Market Size, By Type, 2012�2019 (KT)

Table 60 ROW Market Size, By Type, 2012�2019 ($Million)

Table 61 ROW Market Size, By Type, 2012�2019 (KT)

Table 62 ROW Market Size, By Region, 2012�2019 ($Million)

Table 63 ROW Leather Chemicals Market Size, By Region, 2012�2019 (KT)

Table 64 Brazil Market Size, By Type, 2012�2019 ($Million)

Table 65 Brazil Market Size, By Type, 2012�2019 (KT)

Table 66 Argentina Market Size, By Type, 2012�2019 ($Million)

Table 67 Argentina Market Size, By Type, 2012�2019 (KT)

Table 68 Ethiopia Leather Chemicals: Market Size, By Type, 2012�2019 ($Million)

Table 69 Ethiopia Market Size, By Type, 2012�2019 (KT)

Table 70 Others Market Size, By Type, 2012�2019 ($Million)

Table 71 Others Leather Chemicals: Market Size, By Type, 2012�2019 (KT)

Table 72 New Product Launches & New Product Developments, 2010�2014

Table 73 Expansions and Investments, 2010�2014

Table 74 Mergers & Acquisitions, 2010-2014

Table 75 Agreement, Collaboration, & Partnerships, 2010�2014

List of Figures (48 Figures)

Figure 1 Research Methodology

Figure 2 Growth Rate (%) of Leather Chemicals, By Type, 2014�2019

Figure 3 Leather Chemicals Market Size Estimation Methodology: Bottom-Up Approach

Figure 4 Leather Chemical Market Size Estimation Methodology: Top-Down Approach

Figure 5 Break Down of Primary Interviews: By Company Type, Designation & Region

Figure 6 Global Leather Chemicals: Market Size ($Million), By Type

Figure 7 Regional Market Share and Cagr of Leather Chemicals: Market, By Value

Figure 8 Global Leather Chemicals: Market, By Value

Figure 9 Fastest Growing Product Types and Regions

Figure 10 Most of the Asia-Pacific Countries Register High-Growth Rates

Figure 11 Tanning & Dyeing is the Fastest-Growing Product Type Followed, By Beamhouse Chemicals

Figure 12 Leather Chemicals: Market Size, By Country, 2013 Vs. 2019 ($Million)

Figure 13 Leather Manufacturing Process

Figure 14 Market Segmentation, By Type

Figure 15 Market Segmentation, By Region

Figure 16 Abundance of Raw Materials & Growing Demand for Premium-Quality Leather Drive the Leather Chemicals Market

Figure 17 Supply Chain Analysis

Figure 18 Pricing Trend (2014�2019):

Figure 19 Porter�s Five forces Analysis

Figure 20 Tanning & Dyeing and Finishing Chemicals to Witness Significant Market Shares, 2013 Vs 2019

Figure 21 Market � Key Growth Drivers

Figure 22 Key Elements Driving the Leather Chemicals: Market

Figure 23 Key Drivers of the Leather Chemicals: Market

Figure 24 Regional Snapshot (2013)�Rapidly Growing Markets Are Emerging As the New Hot Spots

Figure 25 China�An Attractive Destination for Leather Chemicals

Figure 26 Italy is the Major Market for Three Product Categories in the European Leather Chemicals Market (2013)

Figure 27 Finishing Chemicals to Boost the Italian Leather Chemicals Market

Figure 28 Companies Adopted New Product Launches As the Key Growth Strategy Over the Last Three Years

Figure 29 Bayer AG Grew At the Fastest Rate Between 2010-2013

Figure 30 Battle for Market Share: New Product Launches Between 2010-2014 Was the Key Strategy

Figure 31 Regional Revenue Mix of Top Five Market Players

Figure 32 BASF SE: Business Overview

Figure 33 SWOT Analysis

Figure 34 Bayer AG: Business Overview

Figure 35 SWOT Analysis

Figure 36 Lanxess AG: Business Overview

Figure 37 SWOT Analysis

Figure 38 Elementis PLC: Business Overview

Figure 39 SWOT Analysis

Figure 40 TFL Ledertechnik Gmbh: Business Overview

Figure 41 SWOT Analysis

Figure 42 Clariant International Ltd.: Business Overview

Figure 43 SWOT Analysis

Figure 44 Dystar Singapore Pte Ltd: Business Overview

Figure 45 SWOT Analysis

Figure 46 Stahl Holdings B.V.: Business Overview

Figure 47 Schill+Seilacher Gmbh: Business Overview

Figure 48 Zschimmer & Schwarz & Co KG Chemische Fabriken: Business Overvie

Growth opportunities and latent adjacency in Leather Chemicals Market